You might also like

- 209 THEME Yield ManagementDocument3 pages209 THEME Yield ManagementRavi ThakurNo ratings yet

- ACCA F2 Course NotesDocument494 pagesACCA F2 Course NotesТурал Мансумов100% (4)

- An Introduction to SDN Intent Based NetworkingFrom EverandAn Introduction to SDN Intent Based NetworkingRating: 5 out of 5 stars5/5 (1)

- PBA Vs CADocument11 pagesPBA Vs CANorma WabanNo ratings yet

- The Industry Handbook - The Telecommunications Industry: Back To Industry ListDocument5 pagesThe Industry Handbook - The Telecommunications Industry: Back To Industry ListAnkush ThoratNo ratings yet

- Outreach Networks Case Study SolutionDocument2 pagesOutreach Networks Case Study SolutionEaston Griffin0% (1)

- Third ExamDocument16 pagesThird ExamShine0% (1)

- Future Telco 2014 enDocument324 pagesFuture Telco 2014 enVladimir PodshivalovNo ratings yet

- Neutral Host DAS White Paper WP 108555Document6 pagesNeutral Host DAS White Paper WP 108555Pedro PrietoNo ratings yet

- Definition and Nature of Management ControlDocument4 pagesDefinition and Nature of Management ControlAlma Calvelo Musni100% (2)

- Study On Home LoansDocument52 pagesStudy On Home LoansbrijeshcocoNo ratings yet

- TDD SynchronisationDocument25 pagesTDD SynchronisationfarrukhmohammedNo ratings yet

- Radio DOTDocument36 pagesRadio DOTNgờuyênnguyênngãNguyễn TờiêntiênsắcTiến SờangsangsắcSáng NguyễntiếnSángNo ratings yet

- Modernize Customer Service with a Cloud-Based Contact CenterDocument11 pagesModernize Customer Service with a Cloud-Based Contact CenterMishNo ratings yet

- ManagedServices WhitePaper PDFDocument13 pagesManagedServices WhitePaper PDFaghorbanzadehNo ratings yet

- Genband - The Intelligent SBCDocument10 pagesGenband - The Intelligent SBCAshim SolaimanNo ratings yet

- Ea White Paper 25052011Document16 pagesEa White Paper 25052011vvladimovNo ratings yet

- Jamcracker Case Study AnalysisDocument2 pagesJamcracker Case Study AnalysisAshutosh Jha100% (1)

- Over-the-Top Services: John SladekDocument9 pagesOver-the-Top Services: John SladekNurani MasyitaNo ratings yet

- Essential Reading 5Document20 pagesEssential Reading 5Rahul AwtansNo ratings yet

- Technology: by Ross TisnovskyDocument3 pagesTechnology: by Ross TisnovskyPhattharabophit Pat NanongkhaNo ratings yet

- 2005 Mobihoc Taxi PDFDocument11 pages2005 Mobihoc Taxi PDFالطيبحمودهNo ratings yet

- Accelerating Small Cell DeploymentDocument4 pagesAccelerating Small Cell DeploymentJesus Emmanuel Martinez JimenezNo ratings yet

- Cellwize Award Write-UpDocument10 pagesCellwize Award Write-UpChristopher ChangNo ratings yet

- Big Data in Communications White Paper BAE PDFDocument4 pagesBig Data in Communications White Paper BAE PDFPrash Prak TestAcctNo ratings yet

- Will Cloud Rain On Resellers' Parade?Document3 pagesWill Cloud Rain On Resellers' Parade?quocircaNo ratings yet

- Risk Management in BPODocument4 pagesRisk Management in BPOadeelNo ratings yet

- BCG Service Factory of The Future Aug 2020Document8 pagesBCG Service Factory of The Future Aug 2020meghraj gurjarNo ratings yet

- Your Next IT StrategyDocument10 pagesYour Next IT Strategyxheti21778No ratings yet

- Scsr1213 Section 04 Network Communications: TaskDocument14 pagesScsr1213 Section 04 Network Communications: Tasksooyong123No ratings yet

- Convergence Without Complexity: Insights and Lessons Learned From The TrenchesDocument8 pagesConvergence Without Complexity: Insights and Lessons Learned From The TrenchesJohn C. YoungNo ratings yet

- India 2009 11Document2 pagesIndia 2009 11Kashif AliNo ratings yet

- Outsourcing: A Discussion of The Pros and Cons: Number 37, Winter 2003Document4 pagesOutsourcing: A Discussion of The Pros and Cons: Number 37, Winter 2003Karthikeya SaiNo ratings yet

- Risk Management Notes (Revised)Document13 pagesRisk Management Notes (Revised)Imtiaz KaziNo ratings yet

- Network Planning ProblemDocument11 pagesNetwork Planning ProblemXavier EduardoNo ratings yet

- Module 6 Reading - 7 Technology Trends That Will Impact Equipment Dealers by The Year 2020Document22 pagesModule 6 Reading - 7 Technology Trends That Will Impact Equipment Dealers by The Year 2020Sergio VelardeNo ratings yet

- Modern Business Strategies and Process Support (2001)Document7 pagesModern Business Strategies and Process Support (2001)Hany SalahNo ratings yet

- WP Next Generation Platform Innovation in m2m En-XgDocument14 pagesWP Next Generation Platform Innovation in m2m En-XgRaj BhadoriyaNo ratings yet

- What Are The Outsourcing Options For An SME?Document4 pagesWhat Are The Outsourcing Options For An SME?quocircaNo ratings yet

- EMS in The Cloud - FinalDocument5 pagesEMS in The Cloud - FinaltabbforumNo ratings yet

- PDF Chapter 18Document3 pagesPDF Chapter 18jaberalislamNo ratings yet

- White Paper A "Perfect Storm" For Managed UC Service ProvidersDocument12 pagesWhite Paper A "Perfect Storm" For Managed UC Service ProviderseriquewNo ratings yet

- Telecom Business Intelligence - The Five Forces of A Highly Competitive Industry by John Myers - BeyeNETWORKDocument3 pagesTelecom Business Intelligence - The Five Forces of A Highly Competitive Industry by John Myers - BeyeNETWORKnaviprasadthebond9532No ratings yet

- Force10 Networks: Rising To The Challenges of Cloud Computing NetworksDocument6 pagesForce10 Networks: Rising To The Challenges of Cloud Computing NetworksalpvistaNo ratings yet

- 4D Tip ReportDocument16 pages4D Tip ReportGeorge GuNo ratings yet

- Analysis and Design of Next-Generation Software Architectures: 5G, IoT, Blockchain, and Quantum ComputingFrom EverandAnalysis and Design of Next-Generation Software Architectures: 5G, IoT, Blockchain, and Quantum ComputingNo ratings yet

- Motorola Exploding The Myth WPDocument4 pagesMotorola Exploding The Myth WPjcy1978No ratings yet

- Strategies For Evolving Into A Multi Sided BusinessDocument16 pagesStrategies For Evolving Into A Multi Sided Businessj_rageNo ratings yet

- Ciscos Technology AlliancesDocument3 pagesCiscos Technology Alliancesapi-252385328No ratings yet

- Sme Cloud Based Services Overseas Successes and Ustralian Opportunities ReportDocument26 pagesSme Cloud Based Services Overseas Successes and Ustralian Opportunities ReportDaniel SherwoodNo ratings yet

- Don't Forget The NetworkDocument3 pagesDon't Forget The NetworkquocircaNo ratings yet

- Optimizing Your Network On A Budget: Expert Reference Series of White PapersDocument16 pagesOptimizing Your Network On A Budget: Expert Reference Series of White PapersgynxNo ratings yet

- 16 QuestionsDocument1 page16 QuestionsBushra KhanNo ratings yet

- Cloud Clarity The Key Tpo SuccessDocument3 pagesCloud Clarity The Key Tpo SuccessquocircaNo ratings yet

- WP Parting The Clouds Demystifying Cloud Computing Options en XGDocument7 pagesWP Parting The Clouds Demystifying Cloud Computing Options en XGcjende1No ratings yet

- Revenue Assurance For Third Party ServicesDocument8 pagesRevenue Assurance For Third Party Servicesmail2liyakhatNo ratings yet

- Sharing Data in The Construction IndustryDocument2 pagesSharing Data in The Construction IndustryrajuanthatiNo ratings yet

- XumaDocument3 pagesXumaPallavi BorkarNo ratings yet

- EB Nabled: RansformationDocument7 pagesEB Nabled: RansformationSylvia GraceNo ratings yet

- X (BSS OSS) White - Paper - How To Transform Business Support Systems To Become A Service Provider of Everything 282791Document9 pagesX (BSS OSS) White - Paper - How To Transform Business Support Systems To Become A Service Provider of Everything 282791zulhelmy photoNo ratings yet

- Know when to outsource VPN services for costs and staffingDocument21 pagesKnow when to outsource VPN services for costs and staffingseenubhaiNo ratings yet

- Busting Myths of On-Demand: Why Multi-Tenancy Matters (Nov. 2007)Document6 pagesBusting Myths of On-Demand: Why Multi-Tenancy Matters (Nov. 2007)Astri NapitupuluNo ratings yet

- Case 3 Rent A CarDocument11 pagesCase 3 Rent A Carmkadawi770100% (1)

- Trends, Opportunities and Use Cases For Mobile Data Monetization in Mature MarketsDocument12 pagesTrends, Opportunities and Use Cases For Mobile Data Monetization in Mature MarketspragsyNo ratings yet

- Chapter 3 Building Cloud NetworkDocument7 pagesChapter 3 Building Cloud Networkali abbas100% (1)

- Name Netid Group Number: Website Link: Tutorial Details Time Spent On AssignmentDocument11 pagesName Netid Group Number: Website Link: Tutorial Details Time Spent On AssignmentDaniel BradleyNo ratings yet

- Project Work 2.0Document18 pagesProject Work 2.0PurviNo ratings yet

- Bandwidth For StreamingDocument6 pagesBandwidth For StreamingfarrukhmohammedNo ratings yet

- MIMODocument4 pagesMIMOfarrukhmohammedNo ratings yet

- Testing of Wireless EquipmentDocument10 pagesTesting of Wireless EquipmentfarrukhmohammedNo ratings yet

- UMTS HandoverDocument2 pagesUMTS HandoverRanjan KumarNo ratings yet

- The Myths and Facts of 5GDocument3 pagesThe Myths and Facts of 5GfarrukhmohammedNo ratings yet

- Testing of Wireless Radio EquipmentDocument12 pagesTesting of Wireless Radio EquipmentfarrukhmohammedNo ratings yet

- Future NetworksDocument3 pagesFuture NetworksfarrukhmohammedNo ratings yet

- HetNet Solution Helps Telcos Improve User Experience & RevenueDocument60 pagesHetNet Solution Helps Telcos Improve User Experience & RevenuefarrukhmohammedNo ratings yet

- Survey Report FemtocellDocument44 pagesSurvey Report FemtocellfarrukhmohammedNo ratings yet

- LTE FDD V LTE TDDDocument3 pagesLTE FDD V LTE TDDfarrukhmohammedNo ratings yet

- Multiple Input Multiple OutputDocument2 pagesMultiple Input Multiple OutputfarrukhmohammedNo ratings yet

- Mesh NetworksDocument7 pagesMesh NetworksfarrukhmohammedNo ratings yet

- MPLS TechnologiesDocument1 pageMPLS TechnologiesfarrukhmohammedNo ratings yet

- Trans in Tendering ProcessDocument11 pagesTrans in Tendering ProcessfarrukhmohammedNo ratings yet

- PIM Brings A New Perspective To DAS InstallationsDocument4 pagesPIM Brings A New Perspective To DAS InstallationsfarrukhmohammedNo ratings yet

- A New Approach To Enterprise LTEDocument3 pagesA New Approach To Enterprise LTEfarrukhmohammedNo ratings yet

- Circulation of The Awf-9 QuestionnairesDocument2 pagesCirculation of The Awf-9 QuestionnairesfarrukhmohammedNo ratings yet

- Connecting DAS To CRANDocument3 pagesConnecting DAS To CRANfarrukhmohammedNo ratings yet

- Dos and Don'Ts of WLAN and DASDocument4 pagesDos and Don'Ts of WLAN and DASfarrukhmohammedNo ratings yet

- Coping With Wi-Fi's Biggest Problem InterferenceDocument6 pagesCoping With Wi-Fi's Biggest Problem InterferencefarrukhmohammedNo ratings yet

- Compatibility StudyDocument61 pagesCompatibility StudyfarrukhmohammedNo ratings yet

- Making The Most of Wi-Fi CallingDocument6 pagesMaking The Most of Wi-Fi CallingfarrukhmohammedNo ratings yet

- In-Building RF Planning Tools For Small CellsDocument4 pagesIn-Building RF Planning Tools For Small CellsfarrukhmohammedNo ratings yet

- Calculating and Understanding Optical Power BudgetsDocument3 pagesCalculating and Understanding Optical Power BudgetsfarrukhmohammedNo ratings yet

- DL - UL Acceleration TechnologiesDocument7 pagesDL - UL Acceleration TechnologiesfarrukhmohammedNo ratings yet

- 5ghz Vs 2.4ghz Wireless LanDocument3 pages5ghz Vs 2.4ghz Wireless LanfarrukhmohammedNo ratings yet

- Compatibility StudyDocument61 pagesCompatibility StudyfarrukhmohammedNo ratings yet

- Technical Specification For FAPDocument6 pagesTechnical Specification For FAPfarrukhmohammedNo ratings yet

- Compatibility Study For Umts Operating Within The GSM 900 and GSM 1800 Frequency Bands Roskilde, May 2006Document61 pagesCompatibility Study For Umts Operating Within The GSM 900 and GSM 1800 Frequency Bands Roskilde, May 2006farrukhmohammedNo ratings yet

- Budgeting and Programming Master PlanDocument14 pagesBudgeting and Programming Master PlanJim YauNo ratings yet

- Additional QuestionsDocument57 pagesAdditional QuestionsNadil NinduwaraNo ratings yet

- Commissioner of Internal Revenue vs. ST Luke's Medical CenterDocument1 pageCommissioner of Internal Revenue vs. ST Luke's Medical CenterTJ Dasalla GallardoNo ratings yet

- This Is A System Generated Payslip and Does Not Require SignatureDocument1 pageThis Is A System Generated Payslip and Does Not Require Signaturemamatha mamtaNo ratings yet

- (Kotak) Zee Entertainment Enterprises, May 30, 2022Document11 pages(Kotak) Zee Entertainment Enterprises, May 30, 2022darshanmaldeNo ratings yet

- Cost-Volume-Profit Analysis: © 2009 Pearson Prentice Hall. All Rights ReservedDocument19 pagesCost-Volume-Profit Analysis: © 2009 Pearson Prentice Hall. All Rights ReservedLea WigiartiNo ratings yet

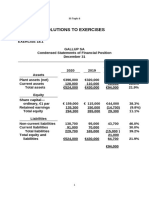

- Chapter 9: Cash Flow Statement: Solutions To Problems and Cases Try It YourselfDocument7 pagesChapter 9: Cash Flow Statement: Solutions To Problems and Cases Try It YourselfSaurabh KhuranaNo ratings yet

- SS Topic 6Document8 pagesSS Topic 6ibrahimkingpubg7No ratings yet

- Absolute returns in any marketDocument20 pagesAbsolute returns in any marketLudwig CaluweNo ratings yet

- Financial ReportingDocument22 pagesFinancial Reportingmhel cabigonNo ratings yet

- Square: Prepared & Submitted by Group: 8Document18 pagesSquare: Prepared & Submitted by Group: 8Niloy Rahman0% (1)

- Company Stock Analysis and Recommendation Report TemplateDocument3 pagesCompany Stock Analysis and Recommendation Report TemplateMary Angeline Lopez100% (1)

- Decision Tree To Evaluate Capacity AlternativesDocument2 pagesDecision Tree To Evaluate Capacity AlternativesShashank TewariNo ratings yet

- Responsibility Accounting and Transfer PricingDocument2 pagesResponsibility Accounting and Transfer PricingLaraNo ratings yet

- Inkp - Icmd 2009 (B06)Document4 pagesInkp - Icmd 2009 (B06)IshidaUryuuNo ratings yet

- 1936 (CTH) Does Not Define The Term Resides', Therefore Its Ordinary Meaning FromDocument8 pages1936 (CTH) Does Not Define The Term Resides', Therefore Its Ordinary Meaning FromDessiree ChenNo ratings yet

- David Ahl v. Fairholme Capital Management LawsuitDocument23 pagesDavid Ahl v. Fairholme Capital Management LawsuitMatthew Seth SarelsonNo ratings yet

- 9.ratio Proportion Variation CAT 2010 Sample QuestionsDocument10 pages9.ratio Proportion Variation CAT 2010 Sample QuestionskeerthanasubramaniNo ratings yet

- Actual Costing enDocument8 pagesActual Costing enRajanNo ratings yet

- Berger Paints India Limited: Public AnnouncementDocument16 pagesBerger Paints India Limited: Public Announcement563vasuNo ratings yet

- Assessing A FirmDocument4 pagesAssessing A Firm蔡朝泉No ratings yet

- When You Dismiss Your Tax Representative, Please Submit "Notification of Dismissal of Tax Representative For Income Tax/consumption Tax". 70Document1 pageWhen You Dismiss Your Tax Representative, Please Submit "Notification of Dismissal of Tax Representative For Income Tax/consumption Tax". 70renatoNo ratings yet

- HCL TECHNOLOGIES EQUITY ANALYSIS TARGET PRICE RS. 1324 GROWTH 26.0Document14 pagesHCL TECHNOLOGIES EQUITY ANALYSIS TARGET PRICE RS. 1324 GROWTH 26.0ROHIT JAISWALNo ratings yet

- Brand Book in Pran JuiceDocument17 pagesBrand Book in Pran JuiceChowdhury Farsad AurangzebNo ratings yet