You might also like

- PWC Clarifying The RulesDocument196 pagesPWC Clarifying The RulesCA Sagar WaghNo ratings yet

- Designing and Implementing A TransferDocument18 pagesDesigning and Implementing A TransferManser KhalidNo ratings yet

- OECD Methods ALICE AND TITUS PDFDocument37 pagesOECD Methods ALICE AND TITUS PDFdjagoenk100% (1)

- PWC Clarifying The Rules PDFDocument196 pagesPWC Clarifying The Rules PDFCristian Nasser Orellana QuispeNo ratings yet

- Five Transfer Pricing Methods With ExamplesDocument15 pagesFive Transfer Pricing Methods With ExamplesErique Miguel MachariaNo ratings yet

- Coordinated Issue Paper - Sec. 482 CSA Buy-In AdjustmentsDocument18 pagesCoordinated Issue Paper - Sec. 482 CSA Buy-In AdjustmentsSgt2No ratings yet

- 2018 Interim Disclosure ChecklistDocument24 pages2018 Interim Disclosure ChecklistWedi TassewNo ratings yet

- Risk Management and Basel II: Bank Alfalah LimitedDocument72 pagesRisk Management and Basel II: Bank Alfalah LimitedtanhaitanhaNo ratings yet

- GRNDocument74 pagesGRNAvinashNo ratings yet

- Ifrs9 For Corporates PDFDocument64 pagesIfrs9 For Corporates PDFeunice chungNo ratings yet

- Share-Based Compensation: Learning ObjectivesDocument48 pagesShare-Based Compensation: Learning ObjectivesMark S MadsenNo ratings yet

- AccountingTools - Questions & Answers PDFDocument4 pagesAccountingTools - Questions & Answers PDFTsvetomira Ivanova100% (1)

- Risk Analysis in Brand ValuationDocument21 pagesRisk Analysis in Brand Valuationvasilev50% (2)

- IFRS Compared To US GAAP 2012 KPMGDocument0 pagesIFRS Compared To US GAAP 2012 KPMGFabi FabianeNo ratings yet

- Analisis Pengaruh Pajak Dan Mekanisme Bonus Terhadap Keputusan Transfer Pricing (3 Files Merged)Document63 pagesAnalisis Pengaruh Pajak Dan Mekanisme Bonus Terhadap Keputusan Transfer Pricing (3 Files Merged)Elsa Kisari PutriNo ratings yet

- Profit PlanningDocument5 pagesProfit PlanningChaudhry Umair YounisNo ratings yet

- Transfer Pricing and Intangibles: Oddleif TorvikDocument877 pagesTransfer Pricing and Intangibles: Oddleif TorvikingjuanesNo ratings yet

- IDEA v9 Case StudyDocument48 pagesIDEA v9 Case StudyTec BrNo ratings yet

- Report On A Forensic Audit and Review of Guyana Forestry CommissionDocument70 pagesReport On A Forensic Audit and Review of Guyana Forestry CommissionGenevieve BelmakerNo ratings yet

- Chapter 20 Issuing Securities To The PublicDocument34 pagesChapter 20 Issuing Securities To The PublicPravin KumarNo ratings yet

- Fair Value Accounting PDFDocument8 pagesFair Value Accounting PDFbgq2296No ratings yet

- Applying IFRS Revenue From Contracts With CustomersDocument76 pagesApplying IFRS Revenue From Contracts With CustomersDhe SagalaNo ratings yet

- Permanent Establishment and Transfer PricingDocument27 pagesPermanent Establishment and Transfer PricingTimothy Jevon LieanderNo ratings yet

- Itp 2015 2016 Final PDFDocument1,162 pagesItp 2015 2016 Final PDFht1234222No ratings yet

- Nestle Strategic Plan Final Project 4M1 Group. (Major - Marekting)Document50 pagesNestle Strategic Plan Final Project 4M1 Group. (Major - Marekting)mohaNo ratings yet

- Chapter 8: Global Accounting and Auditing StandardsDocument32 pagesChapter 8: Global Accounting and Auditing Standardsapi-241660930No ratings yet

- IPSAS in Your Pocket - January 2021Document61 pagesIPSAS in Your Pocket - January 2021Megha AgarwalNo ratings yet

- GAAP and Accounting Concepts ExplainedDocument25 pagesGAAP and Accounting Concepts ExplainedVibhat Chabra 225013No ratings yet

- Understand Interest Rates and Bonds for Accounting, Finance CareersDocument7 pagesUnderstand Interest Rates and Bonds for Accounting, Finance CareersMarlon A. RodriguezNo ratings yet

- Walking Through The Key Challenges' and Practical Insights' of "Financial Instruments"Document70 pagesWalking Through The Key Challenges' and Practical Insights' of "Financial Instruments"Tamirat Eshetu WoldeNo ratings yet

- The Role of The Insurance Industry Association: Brad Smith and Diana KeeganDocument30 pagesThe Role of The Insurance Industry Association: Brad Smith and Diana Keeganrajesh_natarajan_4No ratings yet

- 4 Comparative Accounting America and AsiaDocument17 pages4 Comparative Accounting America and AsiaNIARAMLINo ratings yet

- Chapter 9: International Financial Statement AnalysisDocument31 pagesChapter 9: International Financial Statement Analysisapi-241660930No ratings yet

- International TP Handbook 2011Document0 pagesInternational TP Handbook 2011Kolawole AkinmojiNo ratings yet

- Complete Revision Notes Auditing 1Document90 pagesComplete Revision Notes Auditing 1Marwin AceNo ratings yet

- Accounting For Derivatives and Hedging ActivitiesDocument35 pagesAccounting For Derivatives and Hedging Activitiesevie veronicaNo ratings yet

- Understanding Accounting Standards and IFRSDocument22 pagesUnderstanding Accounting Standards and IFRSdodiyavijay25691No ratings yet

- Best PDFDocument569 pagesBest PDFnidamahNo ratings yet

- Travel Agency ManagementDocument5 pagesTravel Agency ManagementHimani ChaudharyNo ratings yet

- Summary Chapter 6 Accounting For Managers - Paul M. CollierDocument4 pagesSummary Chapter 6 Accounting For Managers - Paul M. CollierMarina_1995No ratings yet

- PWC Ifrs and Luxembourg GaapDocument148 pagesPWC Ifrs and Luxembourg Gaapronitraje100% (2)

- Roche International TaxationDocument59 pagesRoche International Taxationpshu44835No ratings yet

- IFRS 17 in South AfricaDocument12 pagesIFRS 17 in South AfricaDanielNo ratings yet

- Generally Accepted Accounting Principles (GAAP)Document7 pagesGenerally Accepted Accounting Principles (GAAP)Laxmi GurungNo ratings yet

- Ifrs 16 LeasesDocument25 pagesIfrs 16 LeasesOsamaHussainNo ratings yet

- Law of Persons: Legal Subjects and Legal ObjectsDocument4 pagesLaw of Persons: Legal Subjects and Legal ObjectsKelli FinleyNo ratings yet

- PF CMA NotesDocument19 pagesPF CMA NotesvigneshanantharajanNo ratings yet

- Ey Worldwide Transfer Pricing Reference Guide 2018 19Document588 pagesEy Worldwide Transfer Pricing Reference Guide 2018 19Kelvin RodriguezNo ratings yet

- On IFRS, US GAAP and Indian GAAPDocument64 pagesOn IFRS, US GAAP and Indian GAAPrishipath100% (1)

- Lie Dharma Putra-Audit EngagementDocument3 pagesLie Dharma Putra-Audit EngagementDarma SparrowNo ratings yet

- Enterprise Risk Management Plan A Complete Guide - 2021 EditionFrom EverandEnterprise Risk Management Plan A Complete Guide - 2021 EditionNo ratings yet

- Accounting for Professionals: The Business Professionalism Series, #1From EverandAccounting for Professionals: The Business Professionalism Series, #1No ratings yet

- Guide to Contract Pricing: Cost and Price Analysis for Contractors, Subcontractors, and Government AgenciesFrom EverandGuide to Contract Pricing: Cost and Price Analysis for Contractors, Subcontractors, and Government AgenciesNo ratings yet

- Schön in Building Global International Tax Law (2022) 243Document18 pagesSchön in Building Global International Tax Law (2022) 243Selcen CenikogluNo ratings yet

- Max PlanckDocument5 pagesMax Planckflordeliz12No ratings yet

- Apostila Verbo JuridicoDocument6 pagesApostila Verbo Juridicoflordeliz12No ratings yet

- Ensuring Tax Compliance in A Globalized World The International Automatic Exchange of Tax Information PDFDocument374 pagesEnsuring Tax Compliance in A Globalized World The International Automatic Exchange of Tax Information PDFflordeliz12100% (1)

- Bentley. Taxpayer RightsDocument493 pagesBentley. Taxpayer Rightsflordeliz12No ratings yet

- Tax Treaties and Developing CountriesDocument13 pagesTax Treaties and Developing Countriesflordeliz12No ratings yet

- Bort - c03. The Concept of Beneficial Owner in CanadaDocument6 pagesBort - c03. The Concept of Beneficial Owner in Canadaflordeliz12No ratings yet

- Taxation Today Feb09Document7 pagesTaxation Today Feb09flordeliz12No ratings yet

- Almeida PELAYO. MEDIAÇAODocument2 pagesAlmeida PELAYO. MEDIAÇAOflordeliz12No ratings yet

- Analysis of International Tax Law in The Changing State-Society InteractionDocument17 pagesAnalysis of International Tax Law in The Changing State-Society Interactionflordeliz12No ratings yet

- National Interest in The International Tax Game - Tsilly DaganDocument54 pagesNational Interest in The International Tax Game - Tsilly Daganflordeliz12No ratings yet

- International Allocation of Cross-Border Business Profits. Arm's Length PrincipleDocument12 pagesInternational Allocation of Cross-Border Business Profits. Arm's Length Principleflordeliz12No ratings yet

- Source Versus Residence. The Potential of Multilateral Tax TreatiesDocument12 pagesSource Versus Residence. The Potential of Multilateral Tax Treatiesflordeliz12No ratings yet

- Klaus VogelDocument4 pagesKlaus Vogelflordeliz120% (1)

- The Influence of Public Instutions of The Shadow EconomyDocument12 pagesThe Influence of Public Instutions of The Shadow Economyflordeliz12No ratings yet

- Treaty ShoppingDocument12 pagesTreaty Shoppingflordeliz12No ratings yet

- Treaty Shopping and Avoidance of AbuseDocument16 pagesTreaty Shopping and Avoidance of Abuseflordeliz12No ratings yet

- Tax Coordination Between EuDocument26 pagesTax Coordination Between Euflordeliz12No ratings yet

- Responses To Treaty ShoppingDocument16 pagesResponses To Treaty Shoppingflordeliz12No ratings yet

- Credit Versus ExemptionDocument22 pagesCredit Versus Exemptionflordeliz12No ratings yet

- Martin Zagler. Capital Taxation and Economic PerformanceDocument14 pagesMartin Zagler. Capital Taxation and Economic Performanceflordeliz12No ratings yet

- Horizontal Tax CoordinationDocument1 pageHorizontal Tax Coordinationflordeliz12No ratings yet

- In BrazilDocument14 pagesIn Brazilflordeliz12No ratings yet

- DaganDocument45 pagesDaganflordeliz12No ratings yet

- HeinOnline Virginia Tax Review 1998-1999Document54 pagesHeinOnline Virginia Tax Review 1998-1999flordeliz12No ratings yet

- Alberto VegaDocument1 pageAlberto Vegaflordeliz12No ratings yet

- Horizontal Tax CoordinationDocument1 pageHorizontal Tax Coordinationflordeliz12No ratings yet

- GAARDocument80 pagesGAARflordeliz12No ratings yet

- International Tax AvoidanceDocument27 pagesInternational Tax Avoidanceflordeliz12No ratings yet

- Beyond Legal BindingsDocument17 pagesBeyond Legal Bindingsflordeliz12No ratings yet

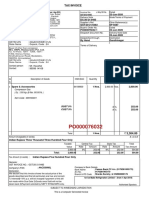

- Tax Invoice: Ice Make Refrigeration Limited - (From 1-Apr-2019)Document1 pageTax Invoice: Ice Make Refrigeration Limited - (From 1-Apr-2019)Sunil PatelNo ratings yet

- Corinthians V Spouses TanjangcoDocument3 pagesCorinthians V Spouses TanjangcoDiane VirtucioNo ratings yet

- Barangay Palao Special Session ResolutionDocument2 pagesBarangay Palao Special Session ResolutionMa Ann Jubay Limbaga-BasaloNo ratings yet

- Law of Criminal Revisions: S.S. UpadhyayDocument60 pagesLaw of Criminal Revisions: S.S. UpadhyayChaitanya KumarNo ratings yet

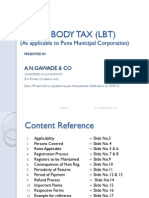

- Local Body Tax in Pune Municipal Corporation (LBT in PMC) - 0Document20 pagesLocal Body Tax in Pune Municipal Corporation (LBT in PMC) - 0nikhilpasariNo ratings yet

- Adp Pay Stub TemplateDocument1 pageAdp Pay Stub TemplateJordan McKenna0% (1)

- Chua v. PeopleDocument17 pagesChua v. PeopleRe doNo ratings yet

- Navarro Vs EscobidoDocument2 pagesNavarro Vs EscobidocarinokatrinaNo ratings yet

- Reaction Paper - Pelican Brief - Japhet Grace Moleta - JD 1-BDocument1 pageReaction Paper - Pelican Brief - Japhet Grace Moleta - JD 1-BJaphet Grace MoletaNo ratings yet

- Joining TimeDocument7 pagesJoining TimeVangara HarshuNo ratings yet

- Nacpil VS. International Broadcasting CorpDocument2 pagesNacpil VS. International Broadcasting CorpAllenNo ratings yet

- Capacity To CONTRACTDocument13 pagesCapacity To CONTRACTpriyaNo ratings yet

- Lawyers On Trial: Human Rights WatchDocument62 pagesLawyers On Trial: Human Rights WatchbaabdullahNo ratings yet

- DOJ Department Circular No. 41Document4 pagesDOJ Department Circular No. 41Nica GasapoNo ratings yet

- Letter To Assemblywoman Lupardo Regarding OPWDD TransitionDocument2 pagesLetter To Assemblywoman Lupardo Regarding OPWDD TransitionDonna LupardoNo ratings yet

- LNS 2003 1 241 Ag02Document64 pagesLNS 2003 1 241 Ag02kish7385No ratings yet

- Harry Keeler Electric Co. v. Rodriguez, G.R. No. L-19001, November 11, 1922 - DUENASDocument2 pagesHarry Keeler Electric Co. v. Rodriguez, G.R. No. L-19001, November 11, 1922 - DUENASJong PerrarenNo ratings yet

- Benguet Electric Cooperative vs NLRC (1992Document4 pagesBenguet Electric Cooperative vs NLRC (1992Naia Gonzales100% (1)

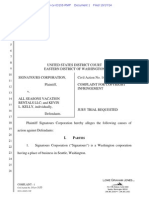

- 2.01 Signatours Corporation V All Seasons Vacation Rentals LLC ComplaintDocument6 pages2.01 Signatours Corporation V All Seasons Vacation Rentals LLC ComplaintCopyright Anti-Bullying Act (CABA Law)No ratings yet

- Petition For NaturalizationDocument4 pagesPetition For NaturalizationbertspamintuanNo ratings yet

- Roshell V. Gasing-Bs Criminology 1st Year - Cri 121-1090Document2 pagesRoshell V. Gasing-Bs Criminology 1st Year - Cri 121-1090roshell GasingNo ratings yet

- History of The Indian Penal CodeDocument7 pagesHistory of The Indian Penal CodeBhushan BariNo ratings yet

- Ielts Scholarship Application Form 2014Document6 pagesIelts Scholarship Application Form 2014Zahid NajuwaNo ratings yet

- Liquidated CaseDocument4 pagesLiquidated CaseJam CastilloNo ratings yet

- Alavado v. City Government of TaclobanDocument1 pageAlavado v. City Government of TaclobanJAMNo ratings yet

- PRD-22 Change of Status With or Without Change in Registered Name Due To MarriageDocument2 pagesPRD-22 Change of Status With or Without Change in Registered Name Due To MarriageClarissa CachoNo ratings yet

- Income Tax Ruling Explains Salary and WagesDocument11 pagesIncome Tax Ruling Explains Salary and WagesAbedNo ratings yet

- National Infrastructure Protection Plan IntroductionDocument8 pagesNational Infrastructure Protection Plan IntroductionSpit Fire100% (6)

- Age Discrimination 2Document2 pagesAge Discrimination 2Raphael Seke OkokoNo ratings yet

- Hancock v. Watson Full TextDocument5 pagesHancock v. Watson Full TextJennilyn TugelidaNo ratings yet