You might also like

- Irrigation in U.S. AgricultureDocument34 pagesIrrigation in U.S. AgriculturePiney MartinNo ratings yet

- Tahal ResentationDocument32 pagesTahal ResentationIon IonescuNo ratings yet

- 1362318507pivot Irriagri EngDocument15 pages1362318507pivot Irriagri EngIon IonescuNo ratings yet

- 215 Toderasc Petru ADocument4 pages215 Toderasc Petru AIon IonescuNo ratings yet

- App 5 Agrinatura Crop TimingsDocument2 pagesApp 5 Agrinatura Crop TimingsIon IonescuNo ratings yet

- Pipes & FittingsDocument3 pagesPipes & FittingsIon IonescuNo ratings yet

- Adina Mriescu, Measure 125Document9 pagesAdina Mriescu, Measure 125Ion IonescuNo ratings yet

- Climate-Smart Agriculture Key to Food Security in AfricaDocument218 pagesClimate-Smart Agriculture Key to Food Security in AfricaIon IonescuNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- 25 Simple ETF PortfoliosDocument10 pages25 Simple ETF PortfoliosdabuttiNo ratings yet

- Stock Valuation TechniquesDocument11 pagesStock Valuation TechniquesSeid KassawNo ratings yet

- Quantifeed White Paper - 13mar17 (002) DC PDFDocument6 pagesQuantifeed White Paper - 13mar17 (002) DC PDFJohanna LaajarinneNo ratings yet

- Introduction To Financial EconometricsDocument191 pagesIntroduction To Financial EconometricsArvinder KaurNo ratings yet

- Sid RgessDocument36 pagesSid Rgessu4rishiNo ratings yet

- Index Investing & Financial Independence For Expats: Getting Started GuideDocument54 pagesIndex Investing & Financial Independence For Expats: Getting Started GuideAmr Mustafa ToradNo ratings yet

- Awp Examination Guide For Exams From 1 May 2016 Up To 30 April 2017Document22 pagesAwp Examination Guide For Exams From 1 May 2016 Up To 30 April 2017Piere Christofer Salas HerreraNo ratings yet

- Example Case 1 - Investment Fund - Chapter 3Document13 pagesExample Case 1 - Investment Fund - Chapter 3JJJNo ratings yet

- Resilience 2021-Market PulseDocument45 pagesResilience 2021-Market PulseNishit GolchhaNo ratings yet

- USD TO INR FORECAST 2020, 2021, 2022, 2023, 2024 - Long ForecastDocument7 pagesUSD TO INR FORECAST 2020, 2021, 2022, 2023, 2024 - Long ForecastShanMugamNo ratings yet

- Msci-Acwi-Islamic-Index (USD)Document3 pagesMsci-Acwi-Islamic-Index (USD)Aristo Elyan TambuwunNo ratings yet

- Stock Index Futures or Options ContractDocument7 pagesStock Index Futures or Options ContractarmailgmNo ratings yet

- Chap 1 - 3 International Certificate in Wealth Management Ed4Document51 pagesChap 1 - 3 International Certificate in Wealth Management Ed4farzycimaNo ratings yet

- CFA Society Boston Level III 2021 Practice Exam Morning SessionDocument53 pagesCFA Society Boston Level III 2021 Practice Exam Morning SessionSteph ONo ratings yet

- Application of The Value Averaging Investment Method On The Us Stock MarketDocument10 pagesApplication of The Value Averaging Investment Method On The Us Stock MarketN C NAGESH PRASAD KOTINo ratings yet

- Memoria Gamesa INGDocument104 pagesMemoria Gamesa INGPrince SMNo ratings yet

- QFR 03-March 2022 LDocument70 pagesQFR 03-March 2022 LNapolean DynamiteNo ratings yet

- Ind Nifty MetalDocument2 pagesInd Nifty MetalShah HiNo ratings yet

- Dow Jones - 100 Year Historical Chart - MacroTrendsDocument1 pageDow Jones - 100 Year Historical Chart - MacroTrendsameliNo ratings yet

- Mutual Fund Concept and Working: Advantages of Mutual FundsDocument60 pagesMutual Fund Concept and Working: Advantages of Mutual FundsSonal ChaurasiaNo ratings yet

- Available Managed FundsDocument18 pagesAvailable Managed Fundsalman888No ratings yet

- Monthly Portfolio Nov 23Document628 pagesMonthly Portfolio Nov 23Chandrasekar ChandramohanNo ratings yet

- Financial Plan Assignments 7apr05Document23 pagesFinancial Plan Assignments 7apr05Pavan Kumar MylavaramNo ratings yet

- ICICI Prudential Value Discovery Fund - Direct Plan Rating: Below Average Risk, Average ReturnDocument4 pagesICICI Prudential Value Discovery Fund - Direct Plan Rating: Below Average Risk, Average ReturnHemant DujariNo ratings yet

- WM - Group (C23-C32) - Structured ProductsDocument30 pagesWM - Group (C23-C32) - Structured ProductsPrince JoshiNo ratings yet

- Binomial Model and Arrow SecuritiesDocument8 pagesBinomial Model and Arrow SecuritiesAlbert WangNo ratings yet

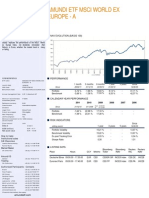

- Amundi ETF Tracks World ex Europe StocksDocument2 pagesAmundi ETF Tracks World ex Europe Stockshp24714303No ratings yet

- Ind Nifty Financial Services PDFDocument2 pagesInd Nifty Financial Services PDFArvind AceNo ratings yet

- Investment Analysis and Portfolio ManagementDocument26 pagesInvestment Analysis and Portfolio Managementkumar sahityaNo ratings yet

- 1900-1935 - Nakamura - Monetario - Banking and Finance in Argentina in The Period 1900-35Document48 pages1900-1935 - Nakamura - Monetario - Banking and Finance in Argentina in The Period 1900-35juan-peronNo ratings yet