You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Audit of CashDocument9 pagesAudit of CashEmma Mariz Garcia25% (8)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Neil Garfield - Expert or Bozo?Document44 pagesNeil Garfield - Expert or Bozo?Bob Hurt50% (2)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Letter of Release From NCDSSDocument2 pagesLetter of Release From NCDSSepowellwcncNo ratings yet

- Letters Written For CannonDocument8 pagesLetters Written For CannonepowellwcncNo ratings yet

- Statement - Bree Newsome.6.29.15Document5 pagesStatement - Bree Newsome.6.29.15epowellwcncNo ratings yet

- Letters Written For Patrick CannonDocument2 pagesLetters Written For Patrick CannonepowellwcncNo ratings yet

- Letters Written For Patrick CannonDocument41 pagesLetters Written For Patrick CannonepowellwcncNo ratings yet

- Letter Sent To Belmont ResidentsDocument3 pagesLetter Sent To Belmont ResidentsepowellwcncNo ratings yet

- 01.23.2015 WCNC Media Request (Classroom Data)Document25 pages01.23.2015 WCNC Media Request (Classroom Data)epowellwcncNo ratings yet

- Letter To Charlotte City CouncilDocument12 pagesLetter To Charlotte City CouncilepowellwcncNo ratings yet

- 2015-3-30 Coddle Acreek - Letter To ParentsDocument1 page2015-3-30 Coddle Acreek - Letter To ParentsepowellwcncNo ratings yet

- H554 Exotic 2015Document5 pagesH554 Exotic 2015epowellwcncNo ratings yet

- McAlpine Ave. LetterDocument2 pagesMcAlpine Ave. LetterepowellwcncNo ratings yet

- Parsons' Indictment ChargesDocument33 pagesParsons' Indictment Chargesepowellwcnc100% (1)

- State Child Fatality ReviewDocument10 pagesState Child Fatality ReviewepowellwcncNo ratings yet

- Bianca Tanner AutopsyDocument6 pagesBianca Tanner AutopsyepowellwcncNo ratings yet

- Morganton Triple Homicide WarrantDocument5 pagesMorganton Triple Homicide WarrantepowellwcncNo ratings yet

- Integrated Review Ceu PDFDocument28 pagesIntegrated Review Ceu PDFHello Kitty100% (1)

- Nomura Quant JD PDFDocument2 pagesNomura Quant JD PDFLakhan SaitejaNo ratings yet

- 1910dsycp 11600Document2 pages1910dsycp 11600brandiwinde41No ratings yet

- British Lyceum ChallanDocument1 pageBritish Lyceum ChallanKamran JalilNo ratings yet

- Statement of AccountDocument7 pagesStatement of AccountHamza CollectionNo ratings yet

- Money LaunderingDocument38 pagesMoney LaunderingMuhammad Saiful IslamNo ratings yet

- HINCOL - EMULSION - Chennai (16 10 2022)Document1 pageHINCOL - EMULSION - Chennai (16 10 2022)praveen kumar sainiNo ratings yet

- In The Partial Fulfillment of The Requirement For The Award of Degree inDocument17 pagesIn The Partial Fulfillment of The Requirement For The Award of Degree inMohmmedKhayyumNo ratings yet

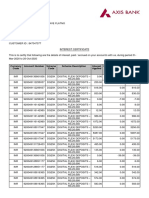

- Interest CertificateDocument2 pagesInterest CertificatesumitNo ratings yet

- LJK UkkDocument55 pagesLJK UkkSaepul RohmanNo ratings yet

- Percukaian (Taxation) 2022Document15 pagesPercukaian (Taxation) 2022Faiz IskandarNo ratings yet

- Engineering EconomyDocument19 pagesEngineering EconomyGreg Calibo LidasanNo ratings yet

- Ratio Analysis at Amararaja Batteries Limited (Arbl) A Project ReportDocument79 pagesRatio Analysis at Amararaja Batteries Limited (Arbl) A Project Reportfahim zamanNo ratings yet

- Tutorial (Merchandising With Answers)Document16 pagesTutorial (Merchandising With Answers)Luize Nathaniele Santos0% (1)

- Lecture 5Document1 pageLecture 5JohnNo ratings yet

- Fundamentals of Auditing and Assurance Services OverviewDocument8 pagesFundamentals of Auditing and Assurance Services OverviewSkye LeeNo ratings yet

- PBCom V CA, G.R. No. 118552, February 5, 1996Document6 pagesPBCom V CA, G.R. No. 118552, February 5, 1996ademarNo ratings yet

- BCG Growth-Share MatrixDocument3 pagesBCG Growth-Share Matrixabhishek kunalNo ratings yet

- Pending Home SalesDocument2 pagesPending Home SalesAmber TaufenNo ratings yet

- Chapter 18Document27 pagesChapter 18jimmy_chou1314100% (1)

- Jurnal 2 - Alaeto Henry Emeka (2020) - Determinants - of - Dividend - Polic - NigeriaDocument31 pagesJurnal 2 - Alaeto Henry Emeka (2020) - Determinants - of - Dividend - Polic - NigeriaGilang KotawaNo ratings yet

- Page 226 236 - Lyka Mae AdluzDocument9 pagesPage 226 236 - Lyka Mae AdluzWendell Maverick MasuhayNo ratings yet

- Assignment No. 1Document3 pagesAssignment No. 1ENo ratings yet

- Lesson 1 ExtendDocument6 pagesLesson 1 ExtendRoel Cababao50% (2)

- Ashoka BuildconDocument11 pagesAshoka Buildconpritish070No ratings yet

- Case 7: Kate Myers: Case Studies in Finance Basic Concepts: The Time Value of MoneyDocument12 pagesCase 7: Kate Myers: Case Studies in Finance Basic Concepts: The Time Value of MoneyluqmanforuNo ratings yet

- ESG Syllabus V3 16062021finalDocument13 pagesESG Syllabus V3 16062021finalsaabiraNo ratings yet

- Business Studies - Exam Paper 1Document12 pagesBusiness Studies - Exam Paper 1Azar100% (1)