You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Phone Pbone: (Eastern IimejDocument6 pagesPhone Pbone: (Eastern IimejlegalmattersNo ratings yet

- Associação Americana de Psicologia - Orientação HomossexualDocument6 pagesAssociação Americana de Psicologia - Orientação HomossexualLorena FonsecaNo ratings yet

- Pentagon Comprehensive Review of Don't Ask, Don't Tell PolicyDocument267 pagesPentagon Comprehensive Review of Don't Ask, Don't Tell PolicyShane Vander HartNo ratings yet

- San Bruno Fire: NTSB Preliminary ReportDocument3 pagesSan Bruno Fire: NTSB Preliminary Reportlegalmatters100% (2)

- Starting With 029:03: Trial DB - v2 Trial DB - v2Document6 pagesStarting With 029:03: Trial DB - v2 Trial DB - v2legalmattersNo ratings yet

- PX2337Document31 pagesPX2337legalmattersNo ratings yet

- PX1319Document36 pagesPX1319legalmattersNo ratings yet

- PX1763Document2 pagesPX1763legalmattersNo ratings yet

- Federal Estate Tax Disadvantages For Same-Sex Couples: July 2009Document27 pagesFederal Estate Tax Disadvantages For Same-Sex Couples: July 2009legalmattersNo ratings yet

- P P E ? T I S - S M C ' B: Utting A Rice On Quality HE Mpact of AME EX Arriage On Alifornia S UdgetDocument37 pagesP P E ? T I S - S M C ' B: Utting A Rice On Quality HE Mpact of AME EX Arriage On Alifornia S UdgetlegalmattersNo ratings yet

- T C D P L: W I M F Y A Y F: HE Alifornia Omestic Artnership AW HAT T Eans OR OU ND OUR AmilyDocument19 pagesT C D P L: W I M F Y A Y F: HE Alifornia Omestic Artnership AW HAT T Eans OR OU ND OUR AmilylegalmattersNo ratings yet

- PX1011Document13 pagesPX1011legalmattersNo ratings yet

- The Impact of Extending Marriage To Same-Sex Couples On The California BudgetDocument16 pagesThe Impact of Extending Marriage To Same-Sex Couples On The California BudgetlegalmattersNo ratings yet

- First Marriage Dissolution, Divorce, and Remarriage: United StatesDocument20 pagesFirst Marriage Dissolution, Divorce, and Remarriage: United StateslegalmattersNo ratings yet

- The Williams Institute: Unequal Taxes On Equal Benefits: The Taxation of Domestic Partner BenefitsDocument27 pagesThe Williams Institute: Unequal Taxes On Equal Benefits: The Taxation of Domestic Partner BenefitslegalmattersNo ratings yet

- PX0943Document23 pagesPX0943legalmattersNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Tax System in FranceDocument8 pagesThe Tax System in FranceMariana MunteanuNo ratings yet

- RPT Case DigestsDocument71 pagesRPT Case Digestscarlota ann lafuenteNo ratings yet

- 074 - Quezon City v. Bayan TelecommunicationsDocument3 pages074 - Quezon City v. Bayan TelecommunicationsMarlowe UyNo ratings yet

- The Lakeville Journal 1-7-16 PDFDocument18 pagesThe Lakeville Journal 1-7-16 PDFLakeville Journal0% (1)

- MIAA V City of Lapu-LapuDocument3 pagesMIAA V City of Lapu-LapuMigs GayaresNo ratings yet

- Ferrer V Bautista DigestsDocument3 pagesFerrer V Bautista Digestspinkblush717100% (1)

- Affidavit of Hipkiss vs. ShinDocument26 pagesAffidavit of Hipkiss vs. ShinP-R HipkissNo ratings yet

- Gross Income (Tax)Document52 pagesGross Income (Tax)HOOPE JISONNo ratings yet

- Mahncke Park - Historic District FlyerDocument3 pagesMahncke Park - Historic District Flyermahncke_justiceNo ratings yet

- Meralco vs. BarlisDocument3 pagesMeralco vs. BarlisMari Erika Joi BancualNo ratings yet

- Principles of TaxDocument46 pagesPrinciples of TaxPASCUA, ROWENA V.No ratings yet

- Urban Water Pricing-ReportDocument53 pagesUrban Water Pricing-Reportshree_rs81No ratings yet

- Reviewer (Book) Chapter 1-3Document41 pagesReviewer (Book) Chapter 1-3Noeme Lansang50% (2)

- Bar Examination 2006 - TaxationlawDocument7 pagesBar Examination 2006 - TaxationlawLyraNo ratings yet

- 2B Property Casebook PDFDocument370 pages2B Property Casebook PDFJireh AgustinNo ratings yet

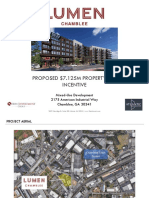

- Chamblee DDADocument99 pagesChamblee DDAZachary HansenNo ratings yet

- Income Tax 02 Taxes, Tax Laws and AdministrationDocument11 pagesIncome Tax 02 Taxes, Tax Laws and AdministrationJade Ivy GarciaNo ratings yet

- June 12, 2015Document16 pagesJune 12, 2015Anonymous KMKk9Msn5No ratings yet

- 012 Kerala Stamp (Undervaluation) Rules 1968Document15 pages012 Kerala Stamp (Undervaluation) Rules 1968shiyas.vkNo ratings yet

- 64.-Angeles University Foundation v. City of Angeles, G.R No. 189999Document12 pages64.-Angeles University Foundation v. City of Angeles, G.R No. 189999Christine Rose Bonilla LikiganNo ratings yet

- Property Tax CADocument42 pagesProperty Tax CAElnur5No ratings yet

- WFH#4 OnegoDocument3 pagesWFH#4 OnegoJoselito OñegoNo ratings yet

- CD - 20. RCPI v. Provincial AssessorDocument1 pageCD - 20. RCPI v. Provincial AssessorAlyssa Alee Angeles JacintoNo ratings yet

- The Punjab Urban Immovable Property Tax Rules 1958Document11 pagesThe Punjab Urban Immovable Property Tax Rules 1958Muhammad Aamir50% (2)

- Seq. To and Inclusive of Article 534, Recapitulating The ThingsDocument44 pagesSeq. To and Inclusive of Article 534, Recapitulating The ThingsChristine ErnoNo ratings yet

- Case StudyDocument2 pagesCase Studybthanks376No ratings yet

- City of Lapu Lapu V PEZADocument3 pagesCity of Lapu Lapu V PEZAjuan aldabaNo ratings yet

- Appraisal Methods Real EstateDocument32 pagesAppraisal Methods Real Estateanujpundir2006100% (3)

- Mah. Act 3 of 2007 The Maha. Fire Prevention & LSM Act-2006Document63 pagesMah. Act 3 of 2007 The Maha. Fire Prevention & LSM Act-2006Priya Vishvanathan AjayNo ratings yet

- Pratt & Whitney Economic Development AgreementDocument23 pagesPratt & Whitney Economic Development AgreementChristian SmithNo ratings yet