You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

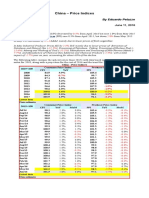

- China - Price IndicesDocument1 pageChina - Price IndicesEduardo PetazzeNo ratings yet

- South Africa - 2015 GDP OutlookDocument1 pageSouth Africa - 2015 GDP OutlookEduardo PetazzeNo ratings yet

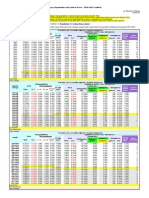

- India - Index of Industrial ProductionDocument1 pageIndia - Index of Industrial ProductionEduardo PetazzeNo ratings yet

- Turkey - Gross Domestic Product, Outlook 2016-2017Document1 pageTurkey - Gross Domestic Product, Outlook 2016-2017Eduardo PetazzeNo ratings yet

- México, PBI 2015Document1 pageMéxico, PBI 2015Eduardo PetazzeNo ratings yet

- Commitment of Traders - Futures Only Contracts - NYMEX (American)Document1 pageCommitment of Traders - Futures Only Contracts - NYMEX (American)Eduardo PetazzeNo ratings yet

- Analysis and Estimation of The US Oil ProductionDocument1 pageAnalysis and Estimation of The US Oil ProductionEduardo PetazzeNo ratings yet

- Germany - Renewable Energies ActDocument1 pageGermany - Renewable Energies ActEduardo PetazzeNo ratings yet

- Highlights, Wednesday June 8, 2016Document1 pageHighlights, Wednesday June 8, 2016Eduardo PetazzeNo ratings yet

- U.S. Employment Situation - 2015 / 2017 OutlookDocument1 pageU.S. Employment Situation - 2015 / 2017 OutlookEduardo PetazzeNo ratings yet

- China - Demand For Petroleum, Energy Efficiency and Consumption Per CapitaDocument1 pageChina - Demand For Petroleum, Energy Efficiency and Consumption Per CapitaEduardo PetazzeNo ratings yet

- US Mining Production IndexDocument1 pageUS Mining Production IndexEduardo PetazzeNo ratings yet

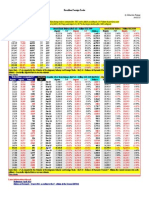

- WTI Spot PriceDocument4 pagesWTI Spot PriceEduardo Petazze100% (1)

- Reflections On The Greek Crisis and The Level of EmploymentDocument1 pageReflections On The Greek Crisis and The Level of EmploymentEduardo PetazzeNo ratings yet

- India 2015 GDPDocument1 pageIndia 2015 GDPEduardo PetazzeNo ratings yet

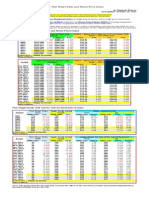

- U.S. New Home Sales and House Price IndexDocument1 pageU.S. New Home Sales and House Price IndexEduardo PetazzeNo ratings yet

- European Commission, Spring 2015 Economic Forecast, Employment SituationDocument1 pageEuropean Commission, Spring 2015 Economic Forecast, Employment SituationEduardo PetazzeNo ratings yet

- China - Power GenerationDocument1 pageChina - Power GenerationEduardo PetazzeNo ratings yet

- USA - Oil and Gas Extraction - Estimated Impact by Low Prices On Economic AggregatesDocument1 pageUSA - Oil and Gas Extraction - Estimated Impact by Low Prices On Economic AggregatesEduardo PetazzeNo ratings yet

- Chile, Monthly Index of Economic Activity, IMACECDocument2 pagesChile, Monthly Index of Economic Activity, IMACECEduardo PetazzeNo ratings yet

- Singapore - 2015 GDP OutlookDocument1 pageSingapore - 2015 GDP OutlookEduardo PetazzeNo ratings yet

- Mainland China - Interest Rates and InflationDocument1 pageMainland China - Interest Rates and InflationEduardo PetazzeNo ratings yet

- Highlights in Scribd, Updated in April 2015Document1 pageHighlights in Scribd, Updated in April 2015Eduardo PetazzeNo ratings yet

- Brazilian Foreign TradeDocument1 pageBrazilian Foreign TradeEduardo PetazzeNo ratings yet

- Japan, Population and Labour Force - 2015-2017 OutlookDocument1 pageJapan, Population and Labour Force - 2015-2017 OutlookEduardo PetazzeNo ratings yet

- US - Personal Income and Outlays - 2015-2016 OutlookDocument1 pageUS - Personal Income and Outlays - 2015-2016 OutlookEduardo PetazzeNo ratings yet

- South Korea, Monthly Industrial StatisticsDocument1 pageSouth Korea, Monthly Industrial StatisticsEduardo PetazzeNo ratings yet

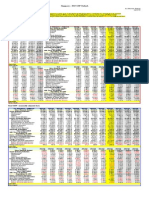

- United States - Gross Domestic Product by IndustryDocument1 pageUnited States - Gross Domestic Product by IndustryEduardo PetazzeNo ratings yet

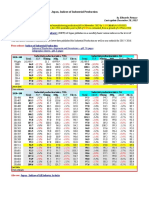

- Japan, Indices of Industrial ProductionDocument1 pageJapan, Indices of Industrial ProductionEduardo PetazzeNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Institutional Framework For Small Business DevelopmentDocument59 pagesInstitutional Framework For Small Business DevelopmentNishantpiyooshNo ratings yet

- Orange Book 2nd Edition 2011 AddendumDocument4 pagesOrange Book 2nd Edition 2011 AddendumAlex JeavonsNo ratings yet

- Introduction to India's Oil and Gas IndustryDocument15 pagesIntroduction to India's Oil and Gas IndustryMeena HarryNo ratings yet

- Summary of Newell'S Corporate AdvantageDocument3 pagesSummary of Newell'S Corporate AdvantageMay Angeline CurbiNo ratings yet

- Benefits of MYOB Accounting SoftwareDocument13 pagesBenefits of MYOB Accounting SoftwareTuba MirzaNo ratings yet

- Questionnaire On Influence of Role of Packaging On ConsumerDocument5 pagesQuestionnaire On Influence of Role of Packaging On ConsumerMicheal Jones85% (13)

- Lkas 27Document15 pagesLkas 27nithyNo ratings yet

- Chapter 3 & 4 Banking An Operations 2Document15 pagesChapter 3 & 4 Banking An Operations 2ManavAgarwalNo ratings yet

- Flexible Budgets, Direct-Cost Variances, and Management ControlDocument21 pagesFlexible Budgets, Direct-Cost Variances, and Management Control2mrbunbunsNo ratings yet

- Going: ForwrdDocument340 pagesGoing: ForwrdAngel MaNo ratings yet

- Report On Non Performing Assets of BankDocument53 pagesReport On Non Performing Assets of Bankhemali chovatiya75% (4)

- Investment and Portfolio AnalysisDocument6 pagesInvestment and Portfolio AnalysisMuhammad HaiderNo ratings yet

- ISM - PrimarkDocument17 pagesISM - PrimarkRatri Ika PratiwiNo ratings yet

- Team 6 - Pricing Assignment 2 - Cambridge Software Corporation V 1.0Document7 pagesTeam 6 - Pricing Assignment 2 - Cambridge Software Corporation V 1.0SJ100% (1)

- S.N. Arts, D.J. Malpani Commerce and B.N. Sarda Science College, Sangamner T.Y. B. Com. Notes: Advanced AccountingDocument34 pagesS.N. Arts, D.J. Malpani Commerce and B.N. Sarda Science College, Sangamner T.Y. B. Com. Notes: Advanced AccountingAnant DivekarNo ratings yet

- ALTHURUPADU BID DOCUMENT Judicial Preview (7 - 11-2019)Document125 pagesALTHURUPADU BID DOCUMENT Judicial Preview (7 - 11-2019)Habeeb ShaikNo ratings yet

- Financial Services CICDocument19 pagesFinancial Services CICAashan Paul100% (1)

- Assignment 1: Marketing ManagementDocument37 pagesAssignment 1: Marketing ManagementHimanshu Verma100% (2)

- Owners EquityDocument8 pagesOwners Equityumer sheikhNo ratings yet

- ScotiaBank AUG 09 Daily FX UpdateDocument3 pagesScotiaBank AUG 09 Daily FX UpdateMiir ViirNo ratings yet

- Accenture Service Design Tale Two Coffee Shops TranscriptDocument2 pagesAccenture Service Design Tale Two Coffee Shops TranscriptAmilcar Alvarez de LeonNo ratings yet

- 20 Important Uses of PLR Rights Material PDFDocument21 pages20 Important Uses of PLR Rights Material PDFRavitNo ratings yet

- Bio Pharma Case StudyDocument2 pagesBio Pharma Case StudyAshish Shadija100% (2)

- The Trap Sir James Goldsmith PDFDocument189 pagesThe Trap Sir James Goldsmith PDFBob L100% (1)

- HR Practices in Automobile IndustryDocument13 pagesHR Practices in Automobile IndustryNEENDI AKSHAY THILAKNo ratings yet

- SunstarDocument189 pagesSunstarSarvesh Chandra SaxenaNo ratings yet

- Taxation Reviewer - SAN BEDADocument128 pagesTaxation Reviewer - SAN BEDAMark Lawrence Guzman93% (28)

- Case Study On Citizens' Band RadioDocument7 pagesCase Study On Citizens' Band RadioরাসেলআহমেদNo ratings yet

- Number of Months Number of Brownouts Per Month: Correct!Document6 pagesNumber of Months Number of Brownouts Per Month: Correct!Hey BeshywapNo ratings yet

- Brand Management Assignment (Project)Document9 pagesBrand Management Assignment (Project)Haider AliNo ratings yet