You might also like

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- Ms Archana. Wali MBA II Semester Exam No. MBA0702009Document78 pagesMs Archana. Wali MBA II Semester Exam No. MBA0702009vijayakooliNo ratings yet

- Introduction To Public and Private Sector BanksDocument21 pagesIntroduction To Public and Private Sector Bankspriyanka shedge100% (1)

- State Bank of IndiaDocument25 pagesState Bank of IndiabsragaNo ratings yet

- Indian Overseas Bank FinalDocument39 pagesIndian Overseas Bank FinalDeepak Singh PundirNo ratings yet

- SBI (State Bank of India)Document2 pagesSBI (State Bank of India)dashgreevlankeshNo ratings yet

- Sravanya MTDocument60 pagesSravanya MTPUTTU GURU PRASAD SENGUNTHA MUDALIAR100% (8)

- A Comparative Study On SBI and HDFC in Ambala City Ijariie5997Document11 pagesA Comparative Study On SBI and HDFC in Ambala City Ijariie5997vinayNo ratings yet

- "Adaptability of E-Banking - A Case Study of Jalandhar": A Final Research Report OnDocument44 pages"Adaptability of E-Banking - A Case Study of Jalandhar": A Final Research Report OnRavinder KaurNo ratings yet

- Non-Performing AssestDocument56 pagesNon-Performing AssestKhalid HussainNo ratings yet

- Retail Banking An Introduction Research Methodology: Title of Project Statement of The Problem Objective of The StudyDocument9 pagesRetail Banking An Introduction Research Methodology: Title of Project Statement of The Problem Objective of The StudySandeep KumarNo ratings yet

- Case Study of SbiDocument6 pagesCase Study of Sbiसंजय साहNo ratings yet

- Final Project of YES BANKDocument68 pagesFinal Project of YES BANKashok sathale100% (1)

- Growth in Banking SectorDocument30 pagesGrowth in Banking SectorHarish Rawal Harish RawalNo ratings yet

- Financial Statement Analysis Soubhagya PDFDocument79 pagesFinancial Statement Analysis Soubhagya PDFDaniel JacksonNo ratings yet

- Co Operative BankDocument52 pagesCo Operative BankDevendra SawantNo ratings yet

- Project Report On Ratio Analysis of HDFC BankDocument15 pagesProject Report On Ratio Analysis of HDFC BankRajat GuptaNo ratings yet

- Analysis of Financial Performance of SbiDocument5 pagesAnalysis of Financial Performance of SbiMAYANK GOYALNo ratings yet

- Project On Rural Banking in IndiaDocument57 pagesProject On Rural Banking in IndiaMunawara 2481No ratings yet

- 80 Pages ProjectDocument80 pages80 Pages ProjectR AdenwalaNo ratings yet

- Introduction of IDBI BankDocument58 pagesIntroduction of IDBI BankHarshada Patil67% (3)

- Best Practices 2 Sindhu Durg DCCB PDFDocument13 pagesBest Practices 2 Sindhu Durg DCCB PDFPRALHADNo ratings yet

- Customer Satisfaction Towards HDFC BANKS AND SBI PDFDocument90 pagesCustomer Satisfaction Towards HDFC BANKS AND SBI PDFKrishma RatheeNo ratings yet

- Blackbook ProjectDocument19 pagesBlackbook ProjectDhruv Rocksta100% (1)

- Credit SaraswatDocument76 pagesCredit Saraswatsahil1508100% (1)

- Comparative Study Between Private Sector Banks and Public Sector BanksDocument60 pagesComparative Study Between Private Sector Banks and Public Sector BanksAsħîŞĥLøÝå100% (1)

- Pooja Patel 70Document93 pagesPooja Patel 70Mohd Saad HamidaniNo ratings yet

- Comparative Study of The Public Sector Amp Private Sector BankDocument68 pagesComparative Study of The Public Sector Amp Private Sector Bankankurp68No ratings yet

- A Project Report On History of SbiDocument57 pagesA Project Report On History of SbiMitali AmagdavNo ratings yet

- Comparative Study On E-Banking of Icici and HDFC BankDocument63 pagesComparative Study On E-Banking of Icici and HDFC BankAbhi KengaleNo ratings yet

- Comparative Study of HDFC and SbiDocument53 pagesComparative Study of HDFC and SbiABHISHEK RAWATNo ratings yet

- A Study On Financial Performance of HDFC BankDocument53 pagesA Study On Financial Performance of HDFC BankFelix BadigerNo ratings yet

- Union Bank of IndiaDocument33 pagesUnion Bank of Indiaraghavan swaminathanNo ratings yet

- "Financial Services of Icici Bank": Project Report OnDocument106 pages"Financial Services of Icici Bank": Project Report OnRajat BansalNo ratings yet

- Innovation in Banking SectorDocument21 pagesInnovation in Banking Sectoruma2k10No ratings yet

- Icici Bank Summer Internship ReportDocument56 pagesIcici Bank Summer Internship ReportAbhishek jain100% (1)

- Axis Bank ProjectDocument78 pagesAxis Bank Projectzizz23No ratings yet

- Merchant Banking Hebu Kapadia 100 Marks Project Jai Hind CollegeDocument59 pagesMerchant Banking Hebu Kapadia 100 Marks Project Jai Hind CollegeShraddha MalandkarNo ratings yet

- Sbi Persoal LoanDocument7 pagesSbi Persoal Loananon_832837899No ratings yet

- Saraswat BankDocument22 pagesSaraswat Banksamy7541No ratings yet

- Retail Banking of Allahabad BankDocument50 pagesRetail Banking of Allahabad Bankaru161112No ratings yet

- Comparision of Publick Sector Bank and Private Sector BankDocument37 pagesComparision of Publick Sector Bank and Private Sector Bankjaypatel2201No ratings yet

- Canara BankDocument35 pagesCanara BankSambathkumar Madanagopal0% (1)

- Organisational Setup and Management of The State Bank of IndiaDocument6 pagesOrganisational Setup and Management of The State Bank of IndiapandisivaNo ratings yet

- ReportDocument120 pagesReportAman Prakash100% (2)

- Cooperative Bank Internship ProjectDocument64 pagesCooperative Bank Internship ProjectJagadish KumarNo ratings yet

- Icici Bank PPT 5584a31de5658Document13 pagesIcici Bank PPT 5584a31de5658dinesh mehlawatNo ratings yet

- Credit Risk Management at State Bank of India Project Report Mba FinanceDocument104 pagesCredit Risk Management at State Bank of India Project Report Mba FinanceNilam Pawar67% (3)

- Indusind Bank LTDDocument77 pagesIndusind Bank LTDbhupsaaaNo ratings yet

- Comparison of Sbi Internet Banking Facilities With Icici BankDocument7 pagesComparison of Sbi Internet Banking Facilities With Icici BankEkta KhoslaNo ratings yet

- OB Union BankDocument6 pagesOB Union BankArka Goswami100% (1)

- Study On Retail Banking in IndiaDocument12 pagesStudy On Retail Banking in IndiashwethaNo ratings yet

- Project Mcom PDFDocument45 pagesProject Mcom PDFPriyanka SatamNo ratings yet

- A Study On Performance of Private Sector Banks in IndiaDocument13 pagesA Study On Performance of Private Sector Banks in IndiaPARAMASIVAN CHELLIAHNo ratings yet

- Chapter-1: Statement of The Problem Objectives Scope Limitations Presentation of The ReportDocument51 pagesChapter-1: Statement of The Problem Objectives Scope Limitations Presentation of The Reportbiji1010No ratings yet

- Introduction of Banking IndustryDocument15 pagesIntroduction of Banking IndustryArchana Mishra100% (1)

- Saraswat BanK ORIGINALDocument57 pagesSaraswat BanK ORIGINALSudama EppiliNo ratings yet

- MBA Project ReportDocument71 pagesMBA Project ReportHimali ChandwaniNo ratings yet

- Contemporary Issue Report ON: "A Critical Case Study of Icici Bank Before and After Merger of Bank of RajasthanDocument68 pagesContemporary Issue Report ON: "A Critical Case Study of Icici Bank Before and After Merger of Bank of RajasthanParesh DuaNo ratings yet

- About The Co-Operative Society: Karnataka University DharwadDocument62 pagesAbout The Co-Operative Society: Karnataka University DharwadArun SavukarNo ratings yet

- OIl Mill BijapurDocument36 pagesOIl Mill BijapurArun SavukarNo ratings yet

- ChetanDocument48 pagesChetanArun SavukarNo ratings yet

- MOHAMMEDDocument83 pagesMOHAMMEDArun SavukarNo ratings yet

- Credit Assessment On Agricultural LoansDocument84 pagesCredit Assessment On Agricultural LoansArun SavukarNo ratings yet

- Tata 1Document79 pagesTata 1Arun SavukarNo ratings yet

- Study of Housing Loan and Awareness of Top Up LoansDocument343 pagesStudy of Housing Loan and Awareness of Top Up LoansArun SavukarNo ratings yet

- Study of Non Performing Assets in Bank of Maharashtra.Document74 pagesStudy of Non Performing Assets in Bank of Maharashtra.Arun Savukar60% (10)

- RNS MotorsDocument59 pagesRNS MotorsArun SavukarNo ratings yet

- Project Title: Octorich Dairy Products Executive SummaryDocument46 pagesProject Title: Octorich Dairy Products Executive SummaryArun SavukarNo ratings yet

- TC and ConductorsDocument37 pagesTC and ConductorsArun SavukarNo ratings yet

- Factors Influences The Purchase Decision To Buy Mahindra Tractor by The FarmerDocument51 pagesFactors Influences The Purchase Decision To Buy Mahindra Tractor by The FarmerArun SavukarNo ratings yet

- Final Report of Apex Bank (Ram)Document85 pagesFinal Report of Apex Bank (Ram)Arun SavukarNo ratings yet

- Axis Bank NPADocument101 pagesAxis Bank NPAArun SavukarNo ratings yet

- ING Banking AnalysisDocument65 pagesING Banking AnalysisArun SavukarNo ratings yet

- Bank of MaharashtraDocument91 pagesBank of MaharashtraArun Savukar67% (3)

- Stolle Terms & Conditions 9 22 16Document3 pagesStolle Terms & Conditions 9 22 16Jhonny Berrios VacaNo ratings yet

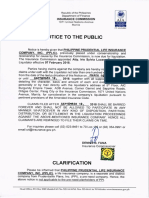

- Notice To The Public PPLIC Placed Under Liquidation Effective 07 Feb 2018Document1 pageNotice To The Public PPLIC Placed Under Liquidation Effective 07 Feb 2018Jerry MisterinoNo ratings yet

- DTC Agreement Between Egypt and ItalyDocument16 pagesDTC Agreement Between Egypt and ItalyOECD: Organisation for Economic Co-operation and DevelopmentNo ratings yet

- FAR - Post-Employement Employee BenefitsDocument5 pagesFAR - Post-Employement Employee BenefitsJohn Mahatma Agripa100% (1)

- Report Writing On Effective Business Letters BY PAKI.Document9 pagesReport Writing On Effective Business Letters BY PAKI.OHWAHWAHNo ratings yet

- Office Space LeaseDocument5 pagesOffice Space LeaseRocketLawyerNo ratings yet

- 071 Edillon vs. Manila Bankers Life Insurance Corp.Document2 pages071 Edillon vs. Manila Bankers Life Insurance Corp.Jovelan V. EscañoNo ratings yet

- RAs For Nursing NLE ReviewDocument1 pageRAs For Nursing NLE Reviewcarlmatt100% (1)

- ICICI Pru Saral Jeevan BimaDocument9 pagesICICI Pru Saral Jeevan BimaThampy ATNo ratings yet

- An Assessment of The Performance of Nile Insurance Company S.C PDFDocument75 pagesAn Assessment of The Performance of Nile Insurance Company S.C PDFnigus100% (2)

- Striking The Right Balance - Pricing in InsuranceDocument102 pagesStriking The Right Balance - Pricing in InsuranceShantanuNo ratings yet

- 3 GratuityDocument17 pages3 GratuityDeepakNo ratings yet

- Best Procurement PracticesDocument13 pagesBest Procurement PracticesSolomon AppiahNo ratings yet

- NCR Frontliners 2017 TaxDocument12 pagesNCR Frontliners 2017 Taxjsus22No ratings yet

- 03.1 Insular Life V NLRCDocument2 pages03.1 Insular Life V NLRCElaineMarcillaNo ratings yet

- Home Mortgage Calculator: Payment ScheduleDocument13 pagesHome Mortgage Calculator: Payment ScheduleAlexander BuitronNo ratings yet

- Eng Construction ContractsDocument50 pagesEng Construction Contractsghadish100% (1)

- Boice Mellon Beach House TransferDocument5 pagesBoice Mellon Beach House TransferGlen HellmanNo ratings yet

- Ong Guan Can and The Bank of The Philippine ISLANDS, Plaintiffs-Appellees, vs. THE CENTURY INSURANCE CO., LTD., Defendant-AppellantDocument37 pagesOng Guan Can and The Bank of The Philippine ISLANDS, Plaintiffs-Appellees, vs. THE CENTURY INSURANCE CO., LTD., Defendant-AppellantMonica MoranteNo ratings yet

- White Gold Marine Vs Pioneer Insurance GR 154514Document5 pagesWhite Gold Marine Vs Pioneer Insurance GR 154514VieNo ratings yet

- TAS 200 Insurance Dec 2016Document10 pagesTAS 200 Insurance Dec 2016tanziam66No ratings yet

- Suretyship: Baldivia Xyra INSURANCE (SAT 1030-1230 AM)Document4 pagesSuretyship: Baldivia Xyra INSURANCE (SAT 1030-1230 AM)Xyra BaldiviaNo ratings yet

- BST Project Aids To TradeDocument19 pagesBST Project Aids To TradeYesh AgarwalNo ratings yet

- Notes Business Studies Lesson 4 XI ComDocument4 pagesNotes Business Studies Lesson 4 XI Comadarshchoudhary2796No ratings yet

- Service Schedule (NPS1.0) PDFDocument1 pageService Schedule (NPS1.0) PDFMarinFeraruNo ratings yet

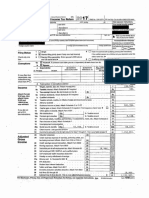

- Sanders IRS Filing 2017Document21 pagesSanders IRS Filing 2017Stephanie Dube DwilsonNo ratings yet

- Am Sure Bonus BuilderDocument4 pagesAm Sure Bonus BuildersuganthiaravindNo ratings yet

- HOME INSURANCE COMPANY, Plaintiff-Appellee, vs. AMERICAN STEAMSHIP AGENCIES, INC. and LUZON STEVEDORING CORPORATION, AMERICAN STEAMSHIP AGENCIES, INC.Document2 pagesHOME INSURANCE COMPANY, Plaintiff-Appellee, vs. AMERICAN STEAMSHIP AGENCIES, INC. and LUZON STEVEDORING CORPORATION, AMERICAN STEAMSHIP AGENCIES, INC.michelle_calzada_1No ratings yet

- Institute and Faculty of Actuaries: Subject ST8 - General Insurance: Pricing Specialist TechnicalDocument25 pagesInstitute and Faculty of Actuaries: Subject ST8 - General Insurance: Pricing Specialist Technicaldickson phiriNo ratings yet

- Insurance Testing AppLabsDocument2 pagesInsurance Testing AppLabsAnant JohriNo ratings yet

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthFrom EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthRating: 4 out of 5 stars4/5 (20)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetFrom EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetRating: 5 out of 5 stars5/5 (2)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Private Equity and Venture Capital in Europe: Markets, Techniques, and DealsFrom EverandPrivate Equity and Venture Capital in Europe: Markets, Techniques, and DealsRating: 5 out of 5 stars5/5 (1)

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Creating Shareholder Value: A Guide For Managers And InvestorsFrom EverandCreating Shareholder Value: A Guide For Managers And InvestorsRating: 4.5 out of 5 stars4.5/5 (8)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (34)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)