You might also like

- Mark-To-Actual Revision of Lower Provision, But Headwind Trend RemainsDocument11 pagesMark-To-Actual Revision of Lower Provision, But Headwind Trend RemainsbodaiNo ratings yet

- Sawasdee SET: S-T Retracement, Opportunity To BuyDocument14 pagesSawasdee SET: S-T Retracement, Opportunity To BuybodaiNo ratings yet

- Features: Tracking TechnicalDocument3 pagesFeatures: Tracking TechnicalbodaiNo ratings yet

- TH Property Sector Update 20180509Document5 pagesTH Property Sector Update 20180509bodaiNo ratings yet

- TH Consumer and Hospitality Sector Update 20180509 RHBDocument14 pagesTH Consumer and Hospitality Sector Update 20180509 RHBbodaiNo ratings yet

- Energy & Power 1Q19 PDFDocument25 pagesEnergy & Power 1Q19 PDFbodaiNo ratings yet

- Morning Brief - E - 2018103918368Document18 pagesMorning Brief - E - 2018103918368bodaiNo ratings yet

- Company Report - IMPACT - E - 20180219081453Document8 pagesCompany Report - IMPACT - E - 20180219081453bodaiNo ratings yet

- ImagesDocument6 pagesImagesbodaiNo ratings yet

- Morning Brief - E - 20170726093031Document25 pagesMorning Brief - E - 20170726093031bodaiNo ratings yet

- TH Property Sector Update 20180509Document5 pagesTH Property Sector Update 20180509bodaiNo ratings yet

- ImagesDocument9 pagesImagesbodaiNo ratings yet

- Morning Brief - E - 20170721100634Document24 pagesMorning Brief - E - 20170721100634bodaiNo ratings yet

- Morning Breif - E - 20170801095547Document22 pagesMorning Breif - E - 20170801095547bodaiNo ratings yet

- SET to bounce on US inflation missDocument10 pagesSET to bounce on US inflation missbodaiNo ratings yet

- Big PursuitDocument8 pagesBig PursuitbodaiNo ratings yet

- SET to bounce on US inflation missDocument10 pagesSET to bounce on US inflation missbodaiNo ratings yet

- ImagesDocument11 pagesImagesbodaiNo ratings yet

- ImagesDocument8 pagesImagesbodaiNo ratings yet

- ImagesDocument11 pagesImagesbodaiNo ratings yet

- Sci FinestDocument8 pagesSci FinestbodaiNo ratings yet

- 20161223175636Document26 pages20161223175636bodaiNo ratings yet

- Morning Brief - E - 20170222092647Document27 pagesMorning Brief - E - 20170222092647bodaiNo ratings yet

- Bangkok Chain Hospital: A New Lease of LifeDocument11 pagesBangkok Chain Hospital: A New Lease of LifebodaiNo ratings yet

- Fish or Cut BaitDocument10 pagesFish or Cut BaitbodaiNo ratings yet

- Time Will PassDocument43 pagesTime Will PassbodaiNo ratings yet

- The Erawan Group: Book Now, Good Price GuaranteedDocument10 pagesThe Erawan Group: Book Now, Good Price GuaranteedbodaiNo ratings yet

- 20161223092340Document3 pages20161223092340bodaiNo ratings yet

- Thai markets move narrowly, foreign funds net sellDocument10 pagesThai markets move narrowly, foreign funds net sellbodaiNo ratings yet

- Aps Lit@tb 110615 93817Document2 pagesAps Lit@tb 110615 93817bodaiNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Meadow DanceDocument22 pagesThe Meadow DancemarutishNo ratings yet

- 2Document3 pages2Ruth TenajerosNo ratings yet

- SEC Accredited Asset Valuer As of February 29 2016Document1 pageSEC Accredited Asset Valuer As of February 29 2016Gean Pearl IcaoNo ratings yet

- Mahusay Acc227 Module 4Document4 pagesMahusay Acc227 Module 4Jeth MahusayNo ratings yet

- Fashion ShoeDocument5 pagesFashion ShoeManal ElkhoshkhanyNo ratings yet

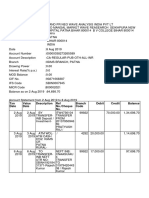

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument3 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceNishi GuptaNo ratings yet

- BENEFITS ILLUSTRATIONDocument2 pagesBENEFITS ILLUSTRATIONRon CatalanNo ratings yet

- Construction and Projects in Indonesia OverviewDocument31 pagesConstruction and Projects in Indonesia OverviewDaniel LubisNo ratings yet

- New Form No 15GDocument4 pagesNew Form No 15GDevang PatelNo ratings yet

- Nature and Importance of Financial SystemsDocument11 pagesNature and Importance of Financial SystemsAuie Eugene Frae SalameraNo ratings yet

- Treasury & Capital MarketsDocument5 pagesTreasury & Capital MarketsHIMANSHI MADANNo ratings yet

- 1-LLIVAN - Alliance Lite 2-MDocument15 pages1-LLIVAN - Alliance Lite 2-Mveldanez100% (6)

- Error Correction (Part 2) - Suspense Accounts (Including RQS)Document6 pagesError Correction (Part 2) - Suspense Accounts (Including RQS)King JulianNo ratings yet

- The Concepts and Practice of Mathematical Finance: Second EditionDocument8 pagesThe Concepts and Practice of Mathematical Finance: Second EditionChâu GiangNo ratings yet

- Sub Order LabelsDocument2 pagesSub Order LabelsZeeshan naseemNo ratings yet

- Tax Sheltered SchemesDocument13 pagesTax Sheltered SchemesVivek DwivediNo ratings yet

- 8 - 8 - 31 - 2023 12 - 00 - 00 Am - 2023Document2 pages8 - 8 - 31 - 2023 12 - 00 - 00 Am - 2023Larry GatlinNo ratings yet

- Revision Question Topic 3,4Document4 pagesRevision Question Topic 3,4Nur Wahida100% (1)

- India Warehousing Report - Knight Frank PDFDocument59 pagesIndia Warehousing Report - Knight Frank PDFdeepakmukhiNo ratings yet

- 23 RD Jan 17 Synergies Dooray AutomativeDocument6 pages23 RD Jan 17 Synergies Dooray AutomativeTarun ParasharNo ratings yet

- Excel Academy of CommerceDocument2 pagesExcel Academy of CommerceHassan Jameel SheikhNo ratings yet

- Credit Dispute FormDocument2 pagesCredit Dispute FormcorvidspamNo ratings yet

- Research ProposalDocument11 pagesResearch ProposalQaiser Khalil100% (1)

- This Is A Complete, Comprehensive and Single Document Promulgated by IASB Establishing The Concepts That Underlie Financial ReportingDocument9 pagesThis Is A Complete, Comprehensive and Single Document Promulgated by IASB Establishing The Concepts That Underlie Financial ReportingFelsie Jane PenasoNo ratings yet

- Ad 5933Document2 pagesAd 5933Kaustuv MishraNo ratings yet

- Fairstone Terms and Conditions PDFDocument10 pagesFairstone Terms and Conditions PDFGarrett GilesNo ratings yet

- Cash Flow and Ratio AnalysisDocument7 pagesCash Flow and Ratio AnalysisShalal Bin YousufNo ratings yet

- Top Trading LessonsDocument19 pagesTop Trading LessonsDheeraj DhingraNo ratings yet

- NPC Guidelines 2019Document119 pagesNPC Guidelines 2019nihajnoorNo ratings yet

- Summary-AHM 510 PDFDocument70 pagesSummary-AHM 510 PDFSiddhartha KalasikamNo ratings yet