You might also like

- AWS D1.1 Structural Welding Code - SteelDocument8 pagesAWS D1.1 Structural Welding Code - SteelMalcolm DiamondNo ratings yet

- The Sales PitchDocument7 pagesThe Sales PitchYasir KhokharNo ratings yet

- Lsat Logical ReasoningDocument1 pageLsat Logical ReasoningAlexa Bulayungan Fontanilla0% (1)

- Limitless Fitness Course BrochureDocument16 pagesLimitless Fitness Course BrochureLimitless Fitness100% (1)

- Case CoachDocument10 pagesCase CoachAnsab Khan100% (1)

- Visa StatementsDocument1 pageVisa Statementsdchristensen5No ratings yet

- 0000 Example Using The SCAMPERDocument23 pages0000 Example Using The SCAMPERAnonymous i3HHYO8No ratings yet

- Student Handouts - Fraud CaseDocument30 pagesStudent Handouts - Fraud Casedchristensen5No ratings yet

- DGCA CPL Conversion Flow ChartDocument3 pagesDGCA CPL Conversion Flow ChartCyril Mathew Roy100% (2)

- Info 4 Coursework IdeasDocument6 pagesInfo 4 Coursework Ideasafiwhhioa100% (1)

- Major Parts of A Research PaperDocument5 pagesMajor Parts of A Research Paperefdkhd4e100% (1)

- Reporting Results ThesisDocument6 pagesReporting Results Thesisclaudiashaharlington100% (2)

- Steps of Preparing Research PaperDocument7 pagesSteps of Preparing Research Paperpib0b1nisyj2100% (1)

- Advanced Corporate Finance: (Preliminary & Subject To Change. Updated On January 12, 2015)Document5 pagesAdvanced Corporate Finance: (Preliminary & Subject To Change. Updated On January 12, 2015)Abhishek KamdarNo ratings yet

- Dissertation First ClassDocument4 pagesDissertation First ClassWhereCanIFindSomeoneToWriteMyPaperUK100% (1)

- UT Dallas Syllabus For Aim6344.002.09f Taught by Umit Gurun (Ugg041000)Document6 pagesUT Dallas Syllabus For Aim6344.002.09f Taught by Umit Gurun (Ugg041000)UT Dallas Provost's Technology GroupNo ratings yet

- Dissertation How Long To WriteDocument8 pagesDissertation How Long To WriteHelpWithPaperWritingAlbuquerque100% (1)

- Caucasus School of BusinessDocument6 pagesCaucasus School of BusinessDavid ChikhladzeNo ratings yet

- Research Paper Chapter 1 ComponentsDocument6 pagesResearch Paper Chapter 1 Componentsgz98szx1100% (1)

- Dissertation Step by Step GuideDocument5 pagesDissertation Step by Step GuideWebsiteThatWillWriteAPaperForYouSingapore100% (1)

- Updated FIN812 Capital Budgeting - 2015 - SpringDocument6 pagesUpdated FIN812 Capital Budgeting - 2015 - Springnguyen_tridung2No ratings yet

- Thesis OutlineDocument4 pagesThesis Outlinew2nrsj5512No ratings yet

- Thesis Statement ObjectivesDocument7 pagesThesis Statement Objectivesewdgbnief100% (2)

- Examples of Good and Bad Thesis StatementsDocument4 pagesExamples of Good and Bad Thesis Statementsbeacbpxff100% (2)

- Syllabus BoothDocument6 pagesSyllabus BoothAshish MakraniNo ratings yet

- ACCT 6260 Syllabus Fall 2010Document6 pagesACCT 6260 Syllabus Fall 2010Nishant VermaNo ratings yet

- What Is A Thesis Driven Research PaperDocument4 pagesWhat Is A Thesis Driven Research Paperfbzgmpm3100% (2)

- Research Paper Discussion and AnalysisDocument7 pagesResearch Paper Discussion and Analysisaflefvsva100% (1)

- Master Thesis Chapter OneDocument4 pagesMaster Thesis Chapter Onerqopqlvcf100% (2)

- Writing Reports and EvaluationsDocument13 pagesWriting Reports and EvaluationsUTS1234No ratings yet

- Thesis Evaluation TechniquesDocument4 pagesThesis Evaluation Techniquesafcnahwvk100% (1)

- Thesis Writing GuidanceDocument8 pagesThesis Writing Guidanceafknvhdlr100% (2)

- Chapter 1 Research Paper PartsDocument6 pagesChapter 1 Research Paper Partsqrcudowgf100% (1)

- Case Coach (HBS)Document19 pagesCase Coach (HBS)amdatabase100% (2)

- Importance of Results and Discussion in A Research PaperDocument6 pagesImportance of Results and Discussion in A Research Paperfvg2xg5rNo ratings yet

- Thesis Chapter One ContentsDocument8 pagesThesis Chapter One Contentszeh0silun0z2100% (1)

- How To Write Results and Discussion For Research PaperDocument7 pagesHow To Write Results and Discussion For Research Paperpukjkzplg100% (1)

- Dissertation Proposal Chapter 1Document4 pagesDissertation Proposal Chapter 1OrderAPaperOnlineUK100% (1)

- Chapter 3 Thesis ComponentsDocument7 pagesChapter 3 Thesis Componentsafkojbvmz100% (2)

- Thesis Vs TopicDocument8 pagesThesis Vs TopicKatie Robinson100% (2)

- First Class Dissertation ConclusionDocument6 pagesFirst Class Dissertation ConclusionCustomHandwritingPaperManchester100% (1)

- Thesis All ChaptersDocument8 pagesThesis All Chapterskathymillerminneapolis100% (2)

- Term Paper Vs ReportDocument6 pagesTerm Paper Vs Reportea8142xb100% (1)

- Thesis Evaluation ReportDocument4 pagesThesis Evaluation Reportdwf6nx2z100% (2)

- Results and Discussion Thesis SampleDocument7 pagesResults and Discussion Thesis Samplefc29jv0c100% (2)

- Course Guidelines - MarketingDocument5 pagesCourse Guidelines - MarketingAgbor AyukNo ratings yet

- Research Paper Chapter 5 ExampleDocument5 pagesResearch Paper Chapter 5 Examplerfxlaerif100% (1)

- Sample Thesis AssessmentDocument4 pagesSample Thesis AssessmentCheapCustomPapersPaterson100% (2)

- How To Write A Good Discussion For A Research PaperDocument5 pagesHow To Write A Good Discussion For A Research PaperlzpyreqhfNo ratings yet

- Background of The Study Sample Thesis ProposalDocument6 pagesBackground of The Study Sample Thesis Proposalafcmnnwss100% (1)

- DoingAppliedResearch AdvertDocument5 pagesDoingAppliedResearch AdvertSynthia SantanaNo ratings yet

- Dissertation Discussion and ConclusionDocument6 pagesDissertation Discussion and ConclusionPayForPaperCanada100% (1)

- How To Write Discussion Research PaperDocument6 pagesHow To Write Discussion Research Paperrfxlaerif100% (1)

- How To Write A Good Thesis IntroductionDocument7 pagesHow To Write A Good Thesis Introductionbsqkr4kn100% (2)

- UT Dallas Syllabus For hmgt6324.001.09s Taught by Laurie Ziegler (Ziegler)Document16 pagesUT Dallas Syllabus For hmgt6324.001.09s Taught by Laurie Ziegler (Ziegler)UT Dallas Provost's Technology GroupNo ratings yet

- Writing Dissertation FastDocument7 pagesWriting Dissertation FastPayToWriteMyPaperUK100% (1)

- Thesis of Writing SkillDocument7 pagesThesis of Writing SkillDawn Cook100% (3)

- Parts of Thesis Chapter 1-3Document7 pagesParts of Thesis Chapter 1-3ppxohvhkd100% (2)

- How To Write Thesis Examination ReportDocument7 pagesHow To Write Thesis Examination Reportruthuithovensiouxfalls100% (2)

- Advanced Coursework MeaningDocument7 pagesAdvanced Coursework Meaningafjzdonobiowee100% (2)

- How To Write A Dissertation DiscussionDocument6 pagesHow To Write A Dissertation DiscussionWriteMyPaperForMeFastCanada100% (1)

- Survey ReportDocument18 pagesSurvey ReportANJILLY IBRAHIMNo ratings yet

- Thesis Specific Objective SampleDocument5 pagesThesis Specific Objective Sampletishanoelfrisco100% (2)

- How To Write A Good Discussion Section in Research PaperDocument8 pagesHow To Write A Good Discussion Section in Research PaperafmchxxyoNo ratings yet

- We Will Write Your ThesisDocument4 pagesWe Will Write Your Thesisfjncb9rp100% (2)

- Examples of A Thesis Statement For A Response PaperDocument4 pagesExamples of A Thesis Statement For A Response Paperveronicagarciaalbuquerque100% (1)

- Statement of The Problem Thesis SampleDocument4 pagesStatement of The Problem Thesis SampleWhitney Anderson100% (2)

- Arya Glover SunderDocument6 pagesArya Glover Sunderdchristensen5No ratings yet

- Tax Policy Presentation QuidelinesDocument3 pagesTax Policy Presentation Quidelinesdchristensen5No ratings yet

- AuditingDocument35 pagesAuditingbabaabbyNo ratings yet

- ACCT 816 Syllabus Summer 2015Document1 pageACCT 816 Syllabus Summer 2015dchristensen5No ratings yet

- Six Flags 2012 Annual Report FinalDocument150 pagesSix Flags 2012 Annual Report Finaldchristensen5No ratings yet

- Tax Reform Act of 2014 DraftDocument1,184 pagesTax Reform Act of 2014 Draftdchristensen5No ratings yet

- TM Allocation - Darden 2014Document5 pagesTM Allocation - Darden 2014dchristensen5No ratings yet

- A Review and Integration of Empirical Research On Materiality: Two Decades LaterDocument36 pagesA Review and Integration of Empirical Research On Materiality: Two Decades Laterdchristensen5No ratings yet

- 831 Syllabus Fall 2014Document8 pages831 Syllabus Fall 2014dchristensen5No ratings yet

- Carson Et Al. (WP, 2012)Document124 pagesCarson Et Al. (WP, 2012)dchristensen5No ratings yet

- Ethridge Et Al. (JBER, 2007)Document8 pagesEthridge Et Al. (JBER, 2007)dchristensen5No ratings yet

- 01 - Problems Solutions - 12EDocument30 pages01 - Problems Solutions - 12Edchristensen5No ratings yet

- QC 00010Document32 pagesQC 00010dchristensen5No ratings yet

- Blay Et Al. (AJPT, 2011)Document26 pagesBlay Et Al. (AJPT, 2011)dchristensen5No ratings yet

- Construction Invoices Received by TBCDocument4 pagesConstruction Invoices Received by TBCdchristensen5No ratings yet

- Away Game Expense InvoicesDocument2 pagesAway Game Expense Invoicesdchristensen5No ratings yet

- Date Amount Debit Credit To Date Amount Debit Credit To: Handout 4. General JournalDocument5 pagesDate Amount Debit Credit To Date Amount Debit Credit To: Handout 4. General Journaldchristensen5No ratings yet

- Equipement Purchase Orders, Invoices, and Receiving SlipsDocument1 pageEquipement Purchase Orders, Invoices, and Receiving Slipsdchristensen5No ratings yet

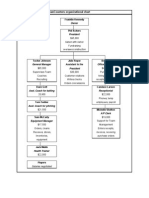

- Handout 1. Tallahassee Beancounters Organizational Chart: OwnerDocument1 pageHandout 1. Tallahassee Beancounters Organizational Chart: Ownerdchristensen5No ratings yet

- ConcessionsDocument1 pageConcessionsdchristensen5No ratings yet

- Account # Account Name Type of Account: Handout 5. Chart of AccountsDocument1 pageAccount # Account Name Type of Account: Handout 5. Chart of Accountsdchristensen5No ratings yet

- Game Schedule May - September: Date Opponent LocationDocument1 pageGame Schedule May - September: Date Opponent Locationdchristensen5No ratings yet

- The Economics of Ethics: A New Perspective On Agency TheoryDocument11 pagesThe Economics of Ethics: A New Perspective On Agency Theorydchristensen5No ratings yet

- 01SV Intro To Animal ProductsDocument16 pages01SV Intro To Animal Productsdchristensen5No ratings yet

- Problem 1 - CH 11Document1 pageProblem 1 - CH 11dchristensen5No ratings yet

- Barron's, Exam Oct 30Document4 pagesBarron's, Exam Oct 30dchristensen5No ratings yet

- Chapter 1 ChartDocument1 pageChapter 1 Chartdchristensen5No ratings yet

- LITR 100-Introduction To Literature in English-Saeed GhaziDocument4 pagesLITR 100-Introduction To Literature in English-Saeed Ghaziosattarahme10% (1)

- Usmle 1Document2 pagesUsmle 1Mey KhNo ratings yet

- B2 First Summer Course Learner BriefingDocument3 pagesB2 First Summer Course Learner BriefingSponge ELTNo ratings yet

- Microsoft Word - UMT Viva - An Overview - AtfieDocument1 pageMicrosoft Word - UMT Viva - An Overview - AtfieZul-AtfiNo ratings yet

- Cagayan de Oro National High SchoolDocument2 pagesCagayan de Oro National High SchoolJarven SaguinNo ratings yet

- PMP Examination Content Outline - 2010Document20 pagesPMP Examination Content Outline - 2010Adi CoratuNo ratings yet

- Study in Canada - Colleges in Canada - Universities in CanadaDocument21 pagesStudy in Canada - Colleges in Canada - Universities in CanadaAnonymous eXAYxVWaQNo ratings yet

- Monitoring Tool For Quarterly TestDocument3 pagesMonitoring Tool For Quarterly TestAnna Dominique Daen100% (2)

- Revenge Unit PlanDocument33 pagesRevenge Unit Planapi-535407654No ratings yet

- Issb NotesDocument15 pagesIssb NotesHasnain Ahmed100% (1)

- SPSD Assignment 2020 - VD1Document2 pagesSPSD Assignment 2020 - VD1Mary KarmacharyaNo ratings yet

- The Bold School Framework For Strategic Blended LearningDocument2 pagesThe Bold School Framework For Strategic Blended Learningapi-300878138No ratings yet

- Group Dynamics - Milgram's ExperimentDocument5 pagesGroup Dynamics - Milgram's ExperimentAbhishek MishraNo ratings yet

- Tips Upsr 2016Document24 pagesTips Upsr 2016kimiabiologi100% (1)

- Yolanda Paramitha ProceedingDocument6 pagesYolanda Paramitha Proceedingyolanda paramithaNo ratings yet

- Debate: Teaching Strategies: Discussion MethodDocument18 pagesDebate: Teaching Strategies: Discussion MethodBrixValdriz100% (1)

- Syllabus NWU - ACA - 010: FIELD STUDY 5 (Learning Assessment Strategies)Document14 pagesSyllabus NWU - ACA - 010: FIELD STUDY 5 (Learning Assessment Strategies)Mark GanitanoNo ratings yet

- Nilesh PDFDocument2 pagesNilesh PDFSHASHI SHEKHARNo ratings yet

- 0653 w16 Ms 62Document5 pages0653 w16 Ms 62yuke kristinaNo ratings yet

- Saint Theresa College of Tandag, Inc.: Outcomes-Based Education (OBE) Course Syllabus inDocument8 pagesSaint Theresa College of Tandag, Inc.: Outcomes-Based Education (OBE) Course Syllabus inRico T. MusongNo ratings yet

- Chapter 11 Factorial ANOVADocument32 pagesChapter 11 Factorial ANOVALis GuziNo ratings yet

- Https Niva - Vidyanikethan.edu Examination ExaminationApplicationAcknowledgement - Aspx PDFDocument2 pagesHttps Niva - Vidyanikethan.edu Examination ExaminationApplicationAcknowledgement - Aspx PDFKotte lokeshNo ratings yet

- Weekly Lesson Plan English VI: 1 PartialDocument2 pagesWeekly Lesson Plan English VI: 1 PartialPerla OlguinNo ratings yet

- Human Resource Development: Biyani's Think TankDocument57 pagesHuman Resource Development: Biyani's Think Tanksunny rockyNo ratings yet