You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Richard 2019Document29 pagesRichard 2019Richard MoszynskiNo ratings yet

- You Got A Frend SatbDocument5 pagesYou Got A Frend SatbSim BelsondraNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Capital One TaxDocument2 pagesCapital One Tax16baezmcNo ratings yet

- Ereceipt PDFDocument1 pageEreceipt PDFAnonymous ap9S5dwPigNo ratings yet

- Tax Planning For Setting New BusinessDocument6 pagesTax Planning For Setting New BusinessHardipsinh Yadav56% (9)

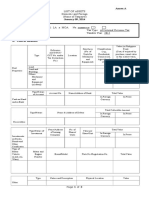

- List of AssetsDocument3 pagesList of AssetsArjam B. Bonsucan80% (5)

- Invoice 1534119076 PDFDocument1 pageInvoice 1534119076 PDFShanaka Tharoosh JayawardhanaNo ratings yet

- Ganpact CompanyDocument1 pageGanpact CompanyAsmin Sultana Ahmed100% (1)

- BIR Ruling No. 392-14Document4 pagesBIR Ruling No. 392-14Francis ArvyNo ratings yet

- CasesDocument191 pagesCasesFrancis ArvyNo ratings yet

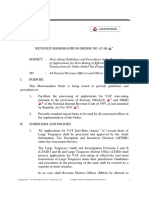

- Rmo 7-06Document239 pagesRmo 7-06Francis ArvyNo ratings yet

- 1st 6 Pages CasesDocument258 pages1st 6 Pages CasesFrancis ArvyNo ratings yet

- Cases Pages 12-15Document100 pagesCases Pages 12-15Francis ArvyNo ratings yet

- LAR Samplex IDocument7 pagesLAR Samplex IFrancis ArvyNo ratings yet

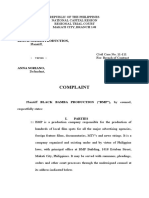

- Complaint: Black Mamba ProductionDocument7 pagesComplaint: Black Mamba ProductionFrancis ArvyNo ratings yet

- Cena Vs Gsis, Gsis v. CADocument3 pagesCena Vs Gsis, Gsis v. CAFrancis ArvyNo ratings yet

- Part 2 EscraDocument52 pagesPart 2 EscraFrancis ArvyNo ratings yet

- Customs Procedure CodesDocument9 pagesCustoms Procedure CodesTSEDEKENo ratings yet

- Pssbooklet PDFDocument142 pagesPssbooklet PDFForkLogNo ratings yet

- Pradnya Kale - Appointment LetterDocument3 pagesPradnya Kale - Appointment LetterPradnya KaleNo ratings yet

- GSTR-1 24ABQPV4297B1Z9 August 2017-18Document23 pagesGSTR-1 24ABQPV4297B1Z9 August 2017-18Aditya NagoriNo ratings yet

- 05 PartnershipDocument20 pages05 Partnershipjustine reine cornicoNo ratings yet

- Uber Direct Fare Addendum: Updated As of December 15, 2022Document4 pagesUber Direct Fare Addendum: Updated As of December 15, 2022SpamchurchNo ratings yet

- Revised TENTATIVE SCHEDULE FOR ONLINE COUNSELLING 09.10.2020 PDFDocument2 pagesRevised TENTATIVE SCHEDULE FOR ONLINE COUNSELLING 09.10.2020 PDFHarshit SrivastavaNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Amit SinghNo ratings yet

- Dave and Diane Starr of New Orleans Louisiana Both ofDocument1 pageDave and Diane Starr of New Orleans Louisiana Both ofCharlotteNo ratings yet

- Finance Act 2022 Analysis by KPMGDocument17 pagesFinance Act 2022 Analysis by KPMGSaviusNo ratings yet

- Pas 32, Pas 12 & Pas 33Document7 pagesPas 32, Pas 12 & Pas 33Olive Jean TiuNo ratings yet

- CHAPTER 3: Financial Documents in The International PaymentDocument33 pagesCHAPTER 3: Financial Documents in The International PaymentVũ Cao Kỳ DuyênNo ratings yet

- 6 For-TkyDocument36 pages6 For-TkyTotzkie LumpoyNo ratings yet

- Pupun00332990000691006 2023Document2 pagesPupun00332990000691006 2023GANGARAM TAMBENo ratings yet

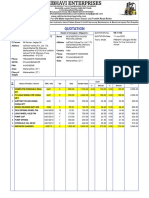

- Ve-1155!22!23-Inditech Valves Private Limited Hand Pallet Truck Repair QuotationDocument2 pagesVe-1155!22!23-Inditech Valves Private Limited Hand Pallet Truck Repair QuotationIndiTech ServiceNo ratings yet

- Oct PayslipDocument3 pagesOct PayslipRajanala Vignesh NaiduNo ratings yet

- GST PPT June19Document65 pagesGST PPT June19yash bhushanNo ratings yet

- Account StatementDocument4 pagesAccount StatementBoitumelo Karabo MosenekeNo ratings yet

- 197 - Excess Contribution and Deposit Correcti..Document1 page197 - Excess Contribution and Deposit Correcti..tdrkNo ratings yet

- Renu JanDocument6 pagesRenu JanSaravanan DhandapaniNo ratings yet

- Test Bank For Corporations Partnerships Estates and Trusts 2020 43th by RaabeDocument77 pagesTest Bank For Corporations Partnerships Estates and Trusts 2020 43th by RaabeJessica RiffleNo ratings yet

- Accounting Transaction, Services CompanyDocument3 pagesAccounting Transaction, Services CompanyCahyani PrastutiNo ratings yet