You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Reserve Bank of India Foreign Exchange Department Central Office Mumbai - 400 001Document2 pagesReserve Bank of India Foreign Exchange Department Central Office Mumbai - 400 001api-25886395No ratings yet

- NullDocument20 pagesNullapi-25886395No ratings yet

- NullDocument13 pagesNullapi-25886395No ratings yet

- Reserve Bank of India Foreign Exchange Department Central Office Mumbai - 400 001Document2 pagesReserve Bank of India Foreign Exchange Department Central Office Mumbai - 400 001api-25886395No ratings yet

- (Published in The Gazette of IndiaDocument6 pages(Published in The Gazette of Indiaapi-25886395No ratings yet

- Important Notice: As Per Recent RBI GuidelinesDocument1 pageImportant Notice: As Per Recent RBI Guidelinesapi-25886395No ratings yet

- Itr-V: Income Tax Return Verification Form IndianDocument1 pageItr-V: Income Tax Return Verification Form Indianapi-25886395No ratings yet

- Form ITR-1Document3 pagesForm ITR-1Rajeev PuthuparambilNo ratings yet

- NotificationDocument7 pagesNotificationapi-25886395No ratings yet

- Highlights of BudgetDocument3 pagesHighlights of Budgetapi-25886395No ratings yet

- Report Highlights: India's GDP To Quadruple To INR 205 TRNDocument7 pagesReport Highlights: India's GDP To Quadruple To INR 205 TRNapi-25886395No ratings yet

- Legal DigestDocument1 pageLegal Digestapi-25886395No ratings yet

- Securities and Exchange Board of India: WWW - Corpfiling.co - inDocument1 pageSecurities and Exchange Board of India: WWW - Corpfiling.co - inapi-25886395No ratings yet

- Important Notice: As Per Recent RBI GuidelinesDocument1 pageImportant Notice: As Per Recent RBI Guidelinesapi-25886395No ratings yet

- Highlights of BudgetDocument3 pagesHighlights of Budgetapi-25886395No ratings yet

- NullDocument22 pagesNullapi-25886395No ratings yet

- Key Features of Budget 2010-2011Document14 pagesKey Features of Budget 2010-2011api-25886395No ratings yet

- S&P CNX Nif T yDocument15 pagesS&P CNX Nif T yapi-25886395No ratings yet

- Views On Union BudgetDocument1 pageViews On Union Budgetapi-25886395No ratings yet

- Key Features of Budget 2010-2011Document14 pagesKey Features of Budget 2010-2011api-25886395No ratings yet

- (Published in The Gazette of IndiaDocument6 pages(Published in The Gazette of Indiaapi-25886395No ratings yet

- Reserve Bank of India: UBD - PCB.Cir. No. 50 /13.05.000/2007-08Document1 pageReserve Bank of India: UBD - PCB.Cir. No. 50 /13.05.000/2007-08api-25886395No ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- RESERVE BANK of INDIA Foreign Exchange DepartmentDocument2 pagesRESERVE BANK of INDIA Foreign Exchange Departmentapi-25886395No ratings yet

- Speech of Mamata Banerjee Introducing The RailwayDocument47 pagesSpeech of Mamata Banerjee Introducing The Railwayapi-25886395No ratings yet

- Speech of Mamata Banerjee Introducing The RailwayDocument47 pagesSpeech of Mamata Banerjee Introducing The Railwayapi-25886395No ratings yet

- RBI - BPLR To Base Rate ChangeDocument4 pagesRBI - BPLR To Base Rate Changeankit_gupta_92No ratings yet

- Rbi/2009-10/323 Dpss - Co.chd - No. 1832 / 04.07.05 / 2009-10Document6 pagesRbi/2009-10/323 Dpss - Co.chd - No. 1832 / 04.07.05 / 2009-10api-25886395No ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Linear Tech FY03 Exec Summary Recommends Dividend HikeDocument9 pagesLinear Tech FY03 Exec Summary Recommends Dividend HikeTestNo ratings yet

- Dissertation Titles in Accounting and FinanceDocument6 pagesDissertation Titles in Accounting and FinanceBuyACollegePaperOnlineSingapore100% (1)

- Mercury Mining Investment LTD - Audited Reports For 2022Document16 pagesMercury Mining Investment LTD - Audited Reports For 2022tankodanjumacNo ratings yet

- Business Finance 2Document19 pagesBusiness Finance 2Paul Manaloto100% (6)

- Tutorials on risk and return analysisDocument4 pagesTutorials on risk and return analysisraju RJNo ratings yet

- Jyothy Lab AR 2019 20 Web Upload - Medium Size 140720Document269 pagesJyothy Lab AR 2019 20 Web Upload - Medium Size 140720Sam vermNo ratings yet

- 1 GR No. 221626-2019-Light Rail Transit Authority v. Quezon CityDocument19 pages1 GR No. 221626-2019-Light Rail Transit Authority v. Quezon City0506sheltonNo ratings yet

- Fauji Fertilizer Co (1) - LTD Aruba KhanDocument33 pagesFauji Fertilizer Co (1) - LTD Aruba KhanYasir Ahmed Farhan50% (2)

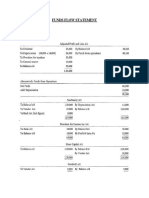

- Funds Flow Statement: Numerical 1Document4 pagesFunds Flow Statement: Numerical 1Neelu AhluwaliaNo ratings yet

- Direct Line Group 2021 Annual ReportDocument262 pagesDirect Line Group 2021 Annual ReportArpita PriyadarshiniNo ratings yet

- Session 3 - Companies Act - Merger, Amalgamation, Share Capital & DebentureDocument88 pagesSession 3 - Companies Act - Merger, Amalgamation, Share Capital & DebentureVaibhav JainNo ratings yet

- Sources of FinanceDocument11 pagesSources of FinanceMitala RogersNo ratings yet

- Chapter 332-The Income Tax Act R.e.2022Document104 pagesChapter 332-The Income Tax Act R.e.2022Ishmael OneyaNo ratings yet

- Pract 1Document12 pagesPract 1Kylie TarnateNo ratings yet

- Model Question Papers: Class 11Document52 pagesModel Question Papers: Class 11Ronak SudhirNo ratings yet

- Introduction to Cesim Global Challenge SimulationDocument21 pagesIntroduction to Cesim Global Challenge SimulationDhawal PanchalNo ratings yet

- Balance sheet and cash flow analysisDocument1,832 pagesBalance sheet and cash flow analysisjadhavshankar100% (1)

- What Amount Should Be Reported As Diluted Earnings Per Share?Document6 pagesWhat Amount Should Be Reported As Diluted Earnings Per Share?carinaNo ratings yet

- Question SheetDocument2 pagesQuestion SheetHarsh DubeNo ratings yet

- Hudson, M. Scenarios For Recovery - How To Write Down The Debts and Restructure The Financial SystemDocument28 pagesHudson, M. Scenarios For Recovery - How To Write Down The Debts and Restructure The Financial SystemxdimitrisNo ratings yet

- Chapter4 AcfarDocument13 pagesChapter4 AcfarKristyll Mae BenemeritoNo ratings yet

- Project BiyayaDocument20 pagesProject BiyayaStephanie CalaraNo ratings yet

- Schedule 14A: Maple Parent Holdings Corp. Consolidated Financial Statements Table of ContentsDocument489 pagesSchedule 14A: Maple Parent Holdings Corp. Consolidated Financial Statements Table of ContentsChulbul PandeyNo ratings yet

- Read With Companies (Declaration and Payment of Dividend) Rules, 2014Document27 pagesRead With Companies (Declaration and Payment of Dividend) Rules, 2014nsk2231No ratings yet

- Pets at Home Fy24 Interims Rns Vfinal CombinedDocument43 pagesPets at Home Fy24 Interims Rns Vfinal Combinedrichard87bNo ratings yet

- Cash FlowDocument15 pagesCash FlowCandy BayonaNo ratings yet

- Financial Ratios Analysis for AAV Mfg CorpDocument5 pagesFinancial Ratios Analysis for AAV Mfg CorpAngelita Dela cruzNo ratings yet

- Form 3251BDocument2 pagesForm 3251BHarish ChandNo ratings yet

- Lecture 2 Depreciation, Accruals and CashflowDocument30 pagesLecture 2 Depreciation, Accruals and CashflowSalahuddin KhanNo ratings yet

- Cost of Capital Calculations for Preference Shares, Bonds, Common Stock & WACCDocument5 pagesCost of Capital Calculations for Preference Shares, Bonds, Common Stock & WACCshikha_asr2273No ratings yet