You might also like

- Assad Associates VAT Act 2014Document9 pagesAssad Associates VAT Act 2014Marc MarcoNo ratings yet

- Presentation On Taxation To The Construction Industry Federation of Zimbabwe (Cifoz)Document44 pagesPresentation On Taxation To The Construction Industry Federation of Zimbabwe (Cifoz)Franco DurantNo ratings yet

- 7tax Administration LectureDocument48 pages7tax Administration LectureHawa MudalaNo ratings yet

- Obligations: 1. RegistrationDocument5 pagesObligations: 1. RegistrationPhilip AlamboNo ratings yet

- 5.1-Module 5Document3 pages5.1-Module 5Arpita ArtaniNo ratings yet

- Withholding Tax SystemDocument8 pagesWithholding Tax Systemjeric aquipelNo ratings yet

- Guide 04: Tax Overview For Businesses, Investors & IndividualsDocument8 pagesGuide 04: Tax Overview For Businesses, Investors & IndividualsAbdul NafiNo ratings yet

- Tax-Free Exchanges That Are Not Subject To Income Tax, Capital Gains Tax, Documentary Stamp Tax And/or Value-Added Tax, As The Case May BeDocument7 pagesTax-Free Exchanges That Are Not Subject To Income Tax, Capital Gains Tax, Documentary Stamp Tax And/or Value-Added Tax, As The Case May BeJouhara ObeñitaNo ratings yet

- Tanzania Revenue Authority - VAT RefundDocument1 pageTanzania Revenue Authority - VAT RefundMICHAEL MBILINYINo ratings yet

- Tax ReviewerDocument17 pagesTax ReviewerSab CardNo ratings yet

- VAT Taxpayer Guide (Input Tax)Document54 pagesVAT Taxpayer Guide (Input Tax)NstrNo ratings yet

- Inome Tax April 15Document2 pagesInome Tax April 15brainNo ratings yet

- Tax AuditDocument9 pagesTax AuditUmar Sajjad AwanNo ratings yet

- Summary Law No. 7 - 2021 - Harmonize Regulations of TaxationDocument8 pagesSummary Law No. 7 - 2021 - Harmonize Regulations of Taxationtina SibagariangNo ratings yet

- Tax Brief - June 2012Document8 pagesTax Brief - June 2012Rheneir MoraNo ratings yet

- Withholding Tax Rates MalawiDocument2 pagesWithholding Tax Rates Malawianraomca100% (1)

- Amnisty For Tax and Custom DutiesDocument12 pagesAmnisty For Tax and Custom DutieserishysiNo ratings yet

- VAT Taxpayer Guide - VAT Return FilingDocument16 pagesVAT Taxpayer Guide - VAT Return FilingNeeyum Njaanum0021No ratings yet

- Taxation Report Vina MarieDocument12 pagesTaxation Report Vina MarieAnonymous gmDxRbnwONo ratings yet

- Kuwait IncomeTax Decree PDFDocument8 pagesKuwait IncomeTax Decree PDFChristian D. Orbe100% (1)

- SPDF May 2007Document8 pagesSPDF May 2007BfpCamarinesNorteNo ratings yet

- VAT RefundDocument2 pagesVAT RefundERICK MLINGWANo ratings yet

- VAT RefundDocument45 pagesVAT RefundPatrick Tan100% (1)

- Facts:: Book ValueDocument2 pagesFacts:: Book Valueultra gayNo ratings yet

- Tax Vat Week4Document73 pagesTax Vat Week4Neil FrangilimanNo ratings yet

- Filing Tax ReturnsDocument10 pagesFiling Tax ReturnsSamNo ratings yet

- Income Tax in GeneralDocument6 pagesIncome Tax in GeneralMatt Marqueses PanganibanNo ratings yet

- Value Added Tax-PDocument20 pagesValue Added Tax-PMa. Corazon CaramalesNo ratings yet

- Boi Bir RulingDocument172 pagesBoi Bir RulingChristine Fe BobisNo ratings yet

- RR 1 - 1998Document3 pagesRR 1 - 1998Lady Ann CayananNo ratings yet

- Faqs Withholding TaxDocument50 pagesFaqs Withholding TaxHarryNo ratings yet

- Value-Added Tax: DescriptionDocument26 pagesValue-Added Tax: DescriptionGIGI BODONo ratings yet

- Chapter 1 General Overview of The Tunisian Tax System: I-IntroductionDocument5 pagesChapter 1 General Overview of The Tunisian Tax System: I-IntroductionsaiyanNo ratings yet

- Lecture 12 Tax Law - UpdatedDocument39 pagesLecture 12 Tax Law - UpdatedAatir ImranNo ratings yet

- Advanced Taxation & Fiscal Policy Nov 2011Document7 pagesAdvanced Taxation & Fiscal Policy Nov 2011Samuel DwumfourNo ratings yet

- CASE DOCTRINES - 2020 Jurisprudence Updates (SC and CTA Cases)Document12 pagesCASE DOCTRINES - 2020 Jurisprudence Updates (SC and CTA Cases)Carlota VillaromanNo ratings yet

- Value Added Tax ActDocument18 pagesValue Added Tax ActStephen Amobi OkoronkwoNo ratings yet

- Tax Law AnswersDocument63 pagesTax Law AnswersMiamor NatividadNo ratings yet

- Service Tax1Document8 pagesService Tax1Suman pendharkarNo ratings yet

- American Express and BurmeisterDocument19 pagesAmerican Express and Burmeistercha chaNo ratings yet

- Handout PDFDocument23 pagesHandout PDFElla CayNo ratings yet

- National TaxationDocument18 pagesNational TaxationShiela Joy CorpuzNo ratings yet

- Imposition If TaxDocument14 pagesImposition If TaxEDWARD BIRYETEGANo ratings yet

- Vol7 - No2.pdf.. TaxationDocument6 pagesVol7 - No2.pdf.. TaxationReyboom BautistaNo ratings yet

- Possibilities in Taxation For The 2017 Bar Examinations: (Project Phoenix)Document54 pagesPossibilities in Taxation For The 2017 Bar Examinations: (Project Phoenix)Ihon BaldadoNo ratings yet

- Assessment ReturnDocument10 pagesAssessment ReturnTriila manillaNo ratings yet

- Kup EngDocument34 pagesKup Engbelajar bisnisNo ratings yet

- Fort Bonifacio Vs CIR DigestDocument3 pagesFort Bonifacio Vs CIR Digestminri72150% (4)

- Amnesty As A Tax Compliance ToolDocument20 pagesAmnesty As A Tax Compliance ToolREJAY89No ratings yet

- Bir Regulations No. 14-2003Document12 pagesBir Regulations No. 14-2003Haryeth CamsolNo ratings yet

- Uae Corporate Tax Law SummaryDocument37 pagesUae Corporate Tax Law SummarypankajNo ratings yet

- Fort Bonifacio Vs CIRDocument2 pagesFort Bonifacio Vs CIRCessy Ciar KimNo ratings yet

- TX102 Topic 1 Module 3Document21 pagesTX102 Topic 1 Module 3Richard Rhamil Carganillo Garcia Jr.No ratings yet

- Tax Administration Self Assessment Regulations NigeriaDocument3 pagesTax Administration Self Assessment Regulations NigeriaMark allenNo ratings yet

- Case Digest #3 - CIR Vs - Mirant PagbilaoDocument3 pagesCase Digest #3 - CIR Vs - Mirant PagbilaoMark AmistosoNo ratings yet

- Filing of Returns and PaymentDocument6 pagesFiling of Returns and PaymentyanyanersNo ratings yet

- Input TaxDocument23 pagesInput TaxIana Gonzaga FajardoNo ratings yet

- VAT Guide For VendorsDocument106 pagesVAT Guide For VendorsUrvashi KhedooNo ratings yet

- QuizDocument14 pagesQuizJepoy Nisperos ReyesNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Mama Samia 3 Years (Daily News)Document1 pageMama Samia 3 Years (Daily News)Anonymous FnM14a0No ratings yet

- Press Release - Absa Group Reports Resilient Earnings in Tough Environment - Underlying Business Strong and GrowingDocument7 pagesPress Release - Absa Group Reports Resilient Earnings in Tough Environment - Underlying Business Strong and GrowingAnonymous FnM14a0No ratings yet

- Public Notice Bank of Tanzania Continues With Its Efforts To Address Foreign Currency ShortagesDocument1 pagePublic Notice Bank of Tanzania Continues With Its Efforts To Address Foreign Currency ShortagesAnonymous FnM14a0No ratings yet

- Tanzania Mortgage Market Update 31 December 2023Document7 pagesTanzania Mortgage Market Update 31 December 2023Anonymous FnM14a0100% (1)

- TIOB March Magazine 2024 - 240306 - 162000Document28 pagesTIOB March Magazine 2024 - 240306 - 162000Anonymous FnM14a0No ratings yet

- Airtel Africa PLC - Results For Half Year Ended 30 September 2023Document56 pagesAirtel Africa PLC - Results For Half Year Ended 30 September 2023Anonymous FnM14a0No ratings yet

- Bank of Tanzania: AaaaaDocument31 pagesBank of Tanzania: AaaaaAnonymous FnM14a0No ratings yet

- Notice To The Public Bank of Tanzania Extends Statutory Administration of Yetu Microfinance Bank PLCDocument1 pageNotice To The Public Bank of Tanzania Extends Statutory Administration of Yetu Microfinance Bank PLCAnonymous FnM14a0No ratings yet

- Tanzania Mortgage Market Update 31 December 2022Document6 pagesTanzania Mortgage Market Update 31 December 2022Anonymous FnM14a0No ratings yet

- Tba Bankers Magazine March 2024Document35 pagesTba Bankers Magazine March 2024Anonymous FnM14a0100% (1)

- HMF in Tanzania Final ReportDocument193 pagesHMF in Tanzania Final ReportAnonymous FnM14a0100% (1)

- Bot MPCDocument3 pagesBot MPCAnonymous FnM14a0No ratings yet

- CRDB Bank Board VacanciesDocument1 pageCRDB Bank Board VacanciesAnonymous FnM14a0No ratings yet

- Monetary Policy Committee Meeting Statement: Benki Kuu Ya Tanzania Bank of TanzaniaDocument3 pagesMonetary Policy Committee Meeting Statement: Benki Kuu Ya Tanzania Bank of TanzaniaAnonymous FnM14a0No ratings yet

- CEOrt - Article For Publishing - 27.02.2023Document3 pagesCEOrt - Article For Publishing - 27.02.2023Anonymous FnM14a0No ratings yet

- Bank of Tanzania: AaaaaDocument33 pagesBank of Tanzania: AaaaaAnonymous FnM14a0No ratings yet

- Chairperson AdvertDocument1 pageChairperson AdvertAnonymous FnM14a0No ratings yet

- Bank of Tanzania: AaaaaDocument33 pagesBank of Tanzania: AaaaaAnonymous FnM14a0No ratings yet

- Tanzania February Updater 2023Document7 pagesTanzania February Updater 2023Anonymous FnM14a0No ratings yet

- CamScanner 02-08-2023 09.16Document1 pageCamScanner 02-08-2023 09.16Anonymous FnM14a0No ratings yet

- CamScanner 01-31-2023 11.21Document1 pageCamScanner 01-31-2023 11.21Anonymous FnM14a0No ratings yet

- CRDB Board VacanciesDocument1 pageCRDB Board VacanciesAnonymous FnM14a0100% (1)

- December 2022: Bank of TanzaniaDocument31 pagesDecember 2022: Bank of TanzaniaAnonymous FnM14a0No ratings yet

- Appointment: Bruce Mwile MwasengaDocument1 pageAppointment: Bruce Mwile MwasengaAnonymous FnM14a0No ratings yet

- Notice To The PublicDocument1 pageNotice To The PublicAnonymous FnM14a0No ratings yet

- Appointment of Mr. Francis Majige Nanai As The New Executive DirectorDocument1 pageAppointment of Mr. Francis Majige Nanai As The New Executive DirectorAnonymous FnM14a0No ratings yet

- MOF InvitationDocument2 pagesMOF InvitationAnonymous FnM14a0No ratings yet

- Appointment: Bruce Mwile MwasengaDocument1 pageAppointment: Bruce Mwile MwasengaAnonymous FnM14a0No ratings yet

- Letter HeadDocument1 pageLetter HeadAnonymous FnM14a0No ratings yet

- Dun & BradstreetDocument1 pageDun & BradstreetAnonymous FnM14a0No ratings yet

- Last Contracts OutlineDocument18 pagesLast Contracts Outlinerambo110No ratings yet

- Forms PDF Principles Sale of InsuranceDocument1 pageForms PDF Principles Sale of InsuranceYves Sieni Locarte YslNo ratings yet

- FFIEC ITBooklet E-BankingDocument84 pagesFFIEC ITBooklet E-BankingChico Setyo AsmoroNo ratings yet

- What Is An Extrajudicial Settlement of EstateDocument13 pagesWhat Is An Extrajudicial Settlement of EstateAnonymous NsXevyNo ratings yet

- Cajiuat v. MathayDocument5 pagesCajiuat v. MathayKylaNo ratings yet

- The United Insurance Company of Pakistan LTDDocument2 pagesThe United Insurance Company of Pakistan LTDAli RiazNo ratings yet

- A Study On Investors Perception Towards Derivative MarketDocument26 pagesA Study On Investors Perception Towards Derivative MarketRajani KanthNo ratings yet

- Pitmanshorthandw00harr BWDocument228 pagesPitmanshorthandw00harr BWRakesh Thadiwal71% (7)

- GAC+JD FinalsDocument3 pagesGAC+JD FinalsAmod JadhavNo ratings yet

- Pooja PDFDocument3 pagesPooja PDFch poojaNo ratings yet

- Sarojpradhanmantrijandhanyojana 151229170610Document89 pagesSarojpradhanmantrijandhanyojana 151229170610RASHMI KUMARI SAHOONo ratings yet

- A New Approach To Segmentation For The Changing Insurance IndustryDocument4 pagesA New Approach To Segmentation For The Changing Insurance Industrypriyanka555No ratings yet

- Axis Reinsurance Oveview - FinalDocument10 pagesAxis Reinsurance Oveview - Finalapi-252940667No ratings yet

- FaqsDocument1 pageFaqsAndy GambleNo ratings yet

- Jurnal Penyesuaian (Kieso Modified)Document39 pagesJurnal Penyesuaian (Kieso Modified)Hervin DiahNo ratings yet

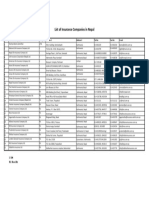

- List of Insurance Companies in Nepal: S. No. Insurance Company Category Address 1 Address 2 Tel No: Fax No: E-MailDocument1 pageList of Insurance Companies in Nepal: S. No. Insurance Company Category Address 1 Address 2 Tel No: Fax No: E-MailUmesh KumarNo ratings yet

- Income Decleration PDFDocument2 pagesIncome Decleration PDFvijay dabhiNo ratings yet

- Buyer Information Sheet: Ropa Disposal CommitteeDocument3 pagesBuyer Information Sheet: Ropa Disposal CommitteeEmmy Bags WalletNo ratings yet

- Sergio Naguiat vs. NLRCDocument15 pagesSergio Naguiat vs. NLRCEnan IntonNo ratings yet

- ISHRAT AFZA National Insurance Certificate of Insurance Cum Policy Shedule Ok TestedDocument1 pageISHRAT AFZA National Insurance Certificate of Insurance Cum Policy Shedule Ok TestedAnil SharmaNo ratings yet

- Solvency RatioDocument4 pagesSolvency RatioZakariyaKhanNo ratings yet

- Save and Learn Money Market Fund ProspectusDocument43 pagesSave and Learn Money Market Fund ProspectusEunice QueNo ratings yet

- Report Palm Haul Sdn. BHDDocument15 pagesReport Palm Haul Sdn. BHDAsan BerlinNo ratings yet

- Credit Mandiri BankDocument8 pagesCredit Mandiri BankVie ViEnNo ratings yet

- MotorSecure Add On Covers PolicyWordingsDocument14 pagesMotorSecure Add On Covers PolicyWordingsRicha BandraNo ratings yet

- Dispute Settlement in Marine InsuranceDocument8 pagesDispute Settlement in Marine InsuranceRavindra Purohit75% (4)

- TDS 23-24Document2 pagesTDS 23-24Taharat Ahmed ChowdhuryNo ratings yet

- S ChakrabortyDocument3 pagesS ChakrabortyAB Block01No ratings yet

- 03 Cost BehaviourDocument24 pages03 Cost BehaviourArindam DasNo ratings yet

- Circular No. 902Document10 pagesCircular No. 902jc cayananNo ratings yet