You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- List The Elements of A New-Venture Team?Document11 pagesList The Elements of A New-Venture Team?Amethyst OnlineNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Corporate Books and Records Chapter 11Document17 pagesCorporate Books and Records Chapter 11NingClaudioNo ratings yet

- PWC Revenue From Contracts With Customers 2016Document298 pagesPWC Revenue From Contracts With Customers 2016hui7411100% (1)

- PWC Guide To Accounting For Derivative Instruments and Hedging ActivitiesDocument594 pagesPWC Guide To Accounting For Derivative Instruments and Hedging Activitieshui7411100% (2)

- PWC Revenue From Contracts With Customers 2016 PDFDocument298 pagesPWC Revenue From Contracts With Customers 2016 PDFhui7411No ratings yet

- Financialreportingdevelopments Bb0977 Derivativeshedging 10october2013Document637 pagesFinancialreportingdevelopments Bb0977 Derivativeshedging 10october2013Yan YanNo ratings yet

- Guide To Accounting For Stock-Based Compensation: A Multidisciplinary ApproachDocument362 pagesGuide To Accounting For Stock-Based Compensation: A Multidisciplinary ApproachEdgar BrownNo ratings yet

- Implementing IFRS 15 Revenue From: Contracts With CustomersDocument24 pagesImplementing IFRS 15 Revenue From: Contracts With Customershui7411No ratings yet

- All POB NOTESDocument249 pagesAll POB NOTESTyra Robinson74% (23)

- KPMG Financial Instruments - The Complete StandardDocument4 pagesKPMG Financial Instruments - The Complete Standardhui7411No ratings yet

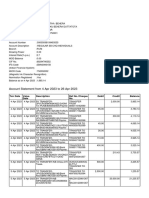

- Account statement from 4 Apr 2023 to 26 Apr 2023Document7 pagesAccount statement from 4 Apr 2023 to 26 Apr 2023BIKRAM KUMAR BEHERANo ratings yet

- PWC Agricultural Assets AccountingDocument24 pagesPWC Agricultural Assets Accountingfaheemshelot100% (1)

- KPMG Impact of IFRS - BankingDocument36 pagesKPMG Impact of IFRS - Bankinghui7411No ratings yet

- Chapter 14 - Control AccountDocument12 pagesChapter 14 - Control AccountFalila Banu ShaikhNo ratings yet

- Guide To Big Data For FinanceDocument14 pagesGuide To Big Data For FinancePedro Alam SargesNo ratings yet

- Akta Kerja 1955 (Bi)Document94 pagesAkta Kerja 1955 (Bi)lengcai100% (2)

- Hedge AccountingDocument8 pagesHedge Accountinghui7411100% (1)

- Chanda Kocchar Conflict of InterestDocument11 pagesChanda Kocchar Conflict of InterestThe Indian Express100% (2)

- Market Strategy Comparison of HDFC Bank and ICICI BankDocument66 pagesMarket Strategy Comparison of HDFC Bank and ICICI BankKamal Bamba100% (2)

- BDO A Guide To Accounting For Financial Instruments in The Public Sector 2011Document7 pagesBDO A Guide To Accounting For Financial Instruments in The Public Sector 2011hui7411No ratings yet

- Financial Instruments (April 2009)Document51 pagesFinancial Instruments (April 2009)Imran AuliyaNo ratings yet

- NOTH Hedge AccountingDocument60 pagesNOTH Hedge Accountingcaldaseletronica280No ratings yet

- Hong Kong Institute of Certified Public Accountants - Accounting Guideline 5 - Merger Accounting For Common Control Combinations 2008Document13 pagesHong Kong Institute of Certified Public Accountants - Accounting Guideline 5 - Merger Accounting For Common Control Combinations 2008hui7411No ratings yet

- IFRS Hot Topic 2008-02 Loan CommitmentsDocument7 pagesIFRS Hot Topic 2008-02 Loan Commitmentshui7411No ratings yet

- A Practical Guide To Hedging - Operational and Accounting Controls, Financial Reporting, and Federal Income Taxes From New York Mercantile ExchangeDocument64 pagesA Practical Guide To Hedging - Operational and Accounting Controls, Financial Reporting, and Federal Income Taxes From New York Mercantile Exchangehui7411No ratings yet

- PWC Hedge Accounting - Outlook For Proposed Changes From The IASB 2010Document15 pagesPWC Hedge Accounting - Outlook For Proposed Changes From The IASB 2010hui7411No ratings yet

- FRS 113 - Fair Value MeasurementsDocument87 pagesFRS 113 - Fair Value Measurementshui7411No ratings yet

- KPMG IFRS Newsletter - Financial Instruments - The Future of IFRS Financial Instruments AccountingDocument10 pagesKPMG IFRS Newsletter - Financial Instruments - The Future of IFRS Financial Instruments Accountinghui7411No ratings yet

- KPMG IFRS Practice Issues For Banks Fair Value Measurement of Derivatives - The BasicsDocument40 pagesKPMG IFRS Practice Issues For Banks Fair Value Measurement of Derivatives - The Basicshui7411No ratings yet

- IFRS Hot Topic 2008-02 Loan CommitmentsDocument7 pagesIFRS Hot Topic 2008-02 Loan Commitmentshui7411No ratings yet

- AC301 Off Balance Sheet FinancingDocument25 pagesAC301 Off Balance Sheet Financinghui7411No ratings yet

- Incoterms Shipping GuideDocument60 pagesIncoterms Shipping GuidejumbotronNo ratings yet

- Financial Instruments Accounting: March 2004Document238 pagesFinancial Instruments Accounting: March 2004hui7411No ratings yet

- Final Project - Acuil Deng Adiang PDFDocument80 pagesFinal Project - Acuil Deng Adiang PDFadiang AcuilNo ratings yet

- Pre2 Notesl Leo CcbrpocDocument15 pagesPre2 Notesl Leo CcbrpocCarla Jane Mirasol ApolinarioNo ratings yet

- I.TAx 302Document4 pagesI.TAx 302tadepalli patanjaliNo ratings yet

- Most Important Terms & ConditionsDocument6 pagesMost Important Terms & ConditionsshanmarsNo ratings yet

- Deed of UndertakingDocument5 pagesDeed of UndertakingPeter Roderick M. OlpocNo ratings yet

- 2341 SafestBanksPR 9 09Document2 pages2341 SafestBanksPR 9 09Danny J. BrouillardNo ratings yet

- SwiftDocument61 pagesSwiftdebarghya.official2021No ratings yet

- Estatement20230706 000233440Document3 pagesEstatement20230706 000233440Mia NahilaNo ratings yet

- Investment Portfolio Analysis of Fewa Finance CompanyDocument130 pagesInvestment Portfolio Analysis of Fewa Finance CompanyBijaya DhakalNo ratings yet

- Security DB by LinkedinDocument2 pagesSecurity DB by LinkedinNazim KhanNo ratings yet

- 469 General Awareness Questions from 2017 ExamsDocument18 pages469 General Awareness Questions from 2017 ExamsHaider BangashNo ratings yet

- Working Capital ManagementDocument59 pagesWorking Capital ManagementjuanferchoNo ratings yet

- Punjab National Bank V Surendra Prasad SinhaDocument3 pagesPunjab National Bank V Surendra Prasad SinhaRenuNo ratings yet

- AssignmentDocument8 pagesAssignmentNawaz ShaikhNo ratings yet

- Summer Bonanza TermsDocument55 pagesSummer Bonanza TermsHaresh Kumar UlaganambiNo ratings yet

- NAB CEO Press Conference Transcript PDFDocument4 pagesNAB CEO Press Conference Transcript PDFmrfutschNo ratings yet

- Assistant Protocol OfficerDocument3 pagesAssistant Protocol OfficerMEHRU NADEEMNo ratings yet

- TGMCDocument90 pagesTGMCRavi KumarNo ratings yet

- Global Finance - Introduction ADocument268 pagesGlobal Finance - Introduction AfirebirdshockwaveNo ratings yet

- SUBCONTRACTOR PREQUALIFICATION QUESTIONNAIREDocument18 pagesSUBCONTRACTOR PREQUALIFICATION QUESTIONNAIREEy-ey ChioNo ratings yet

- PT Bank Rakyat Indonesia (Persero)Document380 pagesPT Bank Rakyat Indonesia (Persero)RyanSoetopoNo ratings yet

- Associated Bank vs. CA (G.R. No. 123793 June 29, 1998) - 6Document9 pagesAssociated Bank vs. CA (G.R. No. 123793 June 29, 1998) - 6Amir Nazri KaibingNo ratings yet