You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Get Homework/Assignment DoneDocument7 pagesGet Homework/Assignment DoneHomework PingNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Project On Muthoot FinanceDocument57 pagesProject On Muthoot FinanceHomework Ping100% (4)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- SAP Case BackgroundDocument21 pagesSAP Case BackgroundHomework PingNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Homework HelpDocument6 pagesHomework HelpHomework PingNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Case Study Fluid ExcessDocument6 pagesCase Study Fluid ExcessHomework PingNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- 01 Mayflower Study GuideDocument8 pages01 Mayflower Study GuideHomework PingNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Philosophy of Law CasesDocument72 pagesPhilosophy of Law CasesHomework PingNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Cases Until ExecutiveDocument19 pagesCases Until ExecutiveHomework PingNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Get Homework/Assignment DoneDocument9 pagesGet Homework/Assignment DoneHomework PingNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Sparkling Glass Case StudyDocument8 pagesSparkling Glass Case StudyHomework Ping100% (3)

- Case StudyDocument5 pagesCase StudyHomework PingNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Get Homework/Assignment DoneDocument24 pagesGet Homework/Assignment DoneHomework PingNo ratings yet

- Get Homework/Assignment DoneDocument13 pagesGet Homework/Assignment DoneHomework PingNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Get Homework/Assignment DoneDocument21 pagesGet Homework/Assignment DoneHomework PingNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Get Homework/Assignment DoneDocument8 pagesGet Homework/Assignment DoneHomework PingNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Astro Case Study 415972Document5 pagesAstro Case Study 415972Homework PingNo ratings yet

- Get Homework/Assignment Done: Homework Help Research Paper Help Online Tutoring Click Here For Freelancing Tutoring SitesDocument9 pagesGet Homework/Assignment Done: Homework Help Research Paper Help Online Tutoring Click Here For Freelancing Tutoring SitesHomework PingNo ratings yet

- Get Homework/Assignment DoneDocument7 pagesGet Homework/Assignment DoneHomework PingNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Yuvienco Vs DacuycuyDocument5 pagesYuvienco Vs DacuycuyHomework PingNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- FF3 TutorialDocument52 pagesFF3 TutorialHomework PingNo ratings yet

- Harvard Case Study Toy WorldDocument19 pagesHarvard Case Study Toy WorldHomework Ping100% (1)

- Case Study No 1Document5 pagesCase Study No 1Homework PingNo ratings yet

- 7.1 AFM - International Investment Appraisal - 251223Document17 pages7.1 AFM - International Investment Appraisal - 251223Kushagra BhandariNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Bali Fixed Departure Oct - Dec O SeriesDocument6 pagesBali Fixed Departure Oct - Dec O SeriesSumit NandaNo ratings yet

- SafariDocument1 pageSafarijayNo ratings yet

- CMC Global - Offer Letter - Mr. Nguyen Huu Phuoc - 170122Document1 pageCMC Global - Offer Letter - Mr. Nguyen Huu Phuoc - 170122kamusuyurikunNo ratings yet

- Phil Tax Midterm ExamDocument25 pagesPhil Tax Midterm ExamDanica VetuzNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Sap Accounting EntriesDocument7 pagesSap Accounting Entriesperera_kushan7365No ratings yet

- Payment ReceiptDocument1 pagePayment Receiptkutra chawlaNo ratings yet

- Income From House PropertyDocument74 pagesIncome From House PropertyHarshit YNo ratings yet

- Practical Accounting of Cash Flow From Operating ActivitiesDocument13 pagesPractical Accounting of Cash Flow From Operating ActivitiesDJ Nicart63% (8)

- Joy Global Inc: FORM 10-KDocument123 pagesJoy Global Inc: FORM 10-KfiahstoneNo ratings yet

- 3657 Atmpa0825cDocument5 pages3657 Atmpa0825cnithinmamidala999No ratings yet

- The Must-Know Facts About Housing Allowance: TaxesDocument4 pagesThe Must-Know Facts About Housing Allowance: Taxeseasygoing1No ratings yet

- 11 Handout 1Document4 pages11 Handout 1Jeffer Jay GubalaneNo ratings yet

- Ratio Analysis of Mahindra N Mahindra LTDDocument15 pagesRatio Analysis of Mahindra N Mahindra LTDMamta60% (5)

- QuestionsDocument9 pagesQuestionsOlivia Jane100% (1)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Jeag Gabriel Final123Document29 pagesJeag Gabriel Final123Jessa MaeNo ratings yet

- Cambridge O Level: Economics 2281/11Document12 pagesCambridge O Level: Economics 2281/11Jack KowmanNo ratings yet

- Icici PruDocument1 pageIcici PruPraveen KumarNo ratings yet

- Final ProjectDocument5 pagesFinal ProjectAkshayNo ratings yet

- Jun 2007 - Qns Mod BDocument16 pagesJun 2007 - Qns Mod BHubbak Khan100% (1)

- "A Study On GST Implementation in FMCG Sector" Table of ContentsDocument49 pages"A Study On GST Implementation in FMCG Sector" Table of ContentsPravallika0% (2)

- Taxpayer Bill of RightsDocument1 pageTaxpayer Bill of RightsCyrine CalagosNo ratings yet

- IRBs Public Ruling No 5 of 2019 - Employee Buy Out Payments Taxable As Perquisites LHAG Update 20200221Document4 pagesIRBs Public Ruling No 5 of 2019 - Employee Buy Out Payments Taxable As Perquisites LHAG Update 20200221Ann YeoNo ratings yet

- Union Budget ReportDocument25 pagesUnion Budget ReportSUBHAM KUMAR PANDANo ratings yet

- Work Book: 7 Steps To Jobs, Careers and God's CallingDocument14 pagesWork Book: 7 Steps To Jobs, Careers and God's CallingTim KraussNo ratings yet

- BSBFIA402 Report On Financial Activity: Instructor WorkbookDocument20 pagesBSBFIA402 Report On Financial Activity: Instructor WorkbookAlexDriveNo ratings yet

- Sensata Technologies Holland B.V: InvoiceDocument2 pagesSensata Technologies Holland B.V: InvoiceDayana IvanovaNo ratings yet

- Set 2 Social Science MajorsDocument4 pagesSet 2 Social Science MajorsPeter ReidNo ratings yet

- Pfm15e Im Ch11Document40 pagesPfm15e Im Ch11vdav hadhNo ratings yet

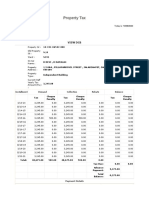

- House Tax ReceiptDocument2 pagesHouse Tax ReceiptAkshaya Raman RamNo ratings yet

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (15)