You might also like

- Family Trusts and Other TrustsDocument5 pagesFamily Trusts and Other TrustsGreg Suefong100% (1)

- Family Trust Guide GWDocument24 pagesFamily Trust Guide GWreydel_santos100% (4)

- The Family Trust 11 Mar 13 Ws PDFDocument7 pagesThe Family Trust 11 Mar 13 Ws PDFkathyayini advocateNo ratings yet

- Beat Estate Tax Forever: The Unprecedented $5 Million Opportunity in 2012From EverandBeat Estate Tax Forever: The Unprecedented $5 Million Opportunity in 2012No ratings yet

- How To Set Up A Family TrustDocument7 pagesHow To Set Up A Family Trustjohnson080875% (4)

- Understanding Trusts: What Is A Trust?Document0 pagesUnderstanding Trusts: What Is A Trust?tku23No ratings yet

- JACK'S HANDY GUIDE TO TRUSTS: Staying Out of CourtFrom EverandJACK'S HANDY GUIDE TO TRUSTS: Staying Out of CourtRating: 5 out of 5 stars5/5 (1)

- Under The Radar How To Protect And Maintain Your Own Financial Fortress By Flying Under The RadarFrom EverandUnder The Radar How To Protect And Maintain Your Own Financial Fortress By Flying Under The RadarNo ratings yet

- The Everything Executor and Trustee Book: A Step-by-Step Guide to Estate and Trust AdministrationFrom EverandThe Everything Executor and Trustee Book: A Step-by-Step Guide to Estate and Trust AdministrationRating: 3 out of 5 stars3/5 (3)

- Asset Protection for the Rest of Us: A Layman's Guide to Asset Protection PlanningFrom EverandAsset Protection for the Rest of Us: A Layman's Guide to Asset Protection PlanningRating: 4.5 out of 5 stars4.5/5 (2)

- Living Trusts for Everyone: Why a Will Is Not the Way to Avoid Probate, Protect Heirs, and Settle Estates (Second Edition)From EverandLiving Trusts for Everyone: Why a Will Is Not the Way to Avoid Probate, Protect Heirs, and Settle Estates (Second Edition)Rating: 5 out of 5 stars5/5 (3)

- Business TrustDocument6 pagesBusiness TrustsentinelionNo ratings yet

- Trust and Estate ManagementDocument18 pagesTrust and Estate ManagementBhuvan100% (1)

- How The Rich Stay Rich - Using A Family Trust Company To Secure ADocument51 pagesHow The Rich Stay Rich - Using A Family Trust Company To Secure Aspcbanking100% (4)

- Nonprofit Law for Religious Organizations: Essential Questions & AnswersFrom EverandNonprofit Law for Religious Organizations: Essential Questions & AnswersRating: 5 out of 5 stars5/5 (1)

- Family TrustDocument91 pagesFamily TrustVence Williams100% (19)

- What Is A Title Holding TrustDocument6 pagesWhat Is A Title Holding Trusttraderash1020100% (2)

- Ubto TrustDocument9 pagesUbto TrustHisExcellency100% (1)

- The Living Trust Advisor: Everything You (and Your Financial Planner) Need to Know about Your Living TrustFrom EverandThe Living Trust Advisor: Everything You (and Your Financial Planner) Need to Know about Your Living TrustRating: 5 out of 5 stars5/5 (1)

- Business TrustDocument5 pagesBusiness Trustempoweredwendy758867% (3)

- The Business TrustDocument17 pagesThe Business TrustdbircS4264100% (5)

- TrustDocument91 pagesTrustmohiuddinduo593% (14)

- 50 Reasons To Use A Land TrustDocument23 pages50 Reasons To Use A Land TrustRandy Hughes83% (6)

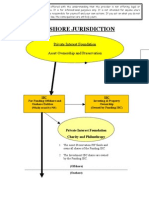

- 5 Minutes Offshore - The TrustDocument4 pages5 Minutes Offshore - The TrustOffshore Company Formation100% (1)

- Irrevocable TrustDocument11 pagesIrrevocable Trustamazing_pinoy50% (2)

- A Trust Can Either Be A Private Trust or A Public Charitable TrustDocument2 pagesA Trust Can Either Be A Private Trust or A Public Charitable TrustShwetaHarlalkaNo ratings yet

- The Complete Guide to Creating Your Own Living Trust A Step by Step Plan to Protect Your Assets, Limit Your Taxes, and Ensure Your Wishes are FulfilledFrom EverandThe Complete Guide to Creating Your Own Living Trust A Step by Step Plan to Protect Your Assets, Limit Your Taxes, and Ensure Your Wishes are FulfilledNo ratings yet

- Family Trusts: A Guide for Beneficiaries, Trustees, Trust Protectors, and Trust CreatorsFrom EverandFamily Trusts: A Guide for Beneficiaries, Trustees, Trust Protectors, and Trust CreatorsRating: 5 out of 5 stars5/5 (2)

- Designing An Income Only Irrevocable TrustDocument15 pagesDesigning An Income Only Irrevocable Trusttaurusho100% (2)

- Massachusetts Business TrustDocument16 pagesMassachusetts Business Trustal moore100% (5)

- Joint Living TrustDocument8 pagesJoint Living TrustRocketLawyer50% (2)

- Living Trust Explained PDFDocument21 pagesLiving Trust Explained PDFJay Steele100% (6)

- Living TrustDocument7 pagesLiving TrustRocketLawyer100% (30)

- Sample Family TrustDocument17 pagesSample Family Trustsheni67% (3)

- Arbitrating Trust IssuesDocument96 pagesArbitrating Trust IssuesMiz09100% (2)

- Family Trust Agreement PDFDocument13 pagesFamily Trust Agreement PDFThileep100% (3)

- The Benefits of A Revocable Living Trust - Financial SamuraiDocument41 pagesThe Benefits of A Revocable Living Trust - Financial SamuraiPatrick Duncan100% (1)

- Activating Funding Pure Business TrustDocument13 pagesActivating Funding Pure Business Trustjoe100% (16)

- Unincorporated Business TrustDocument9 pagesUnincorporated Business TrustSpencerRyanOneal98% (43)

- Irrevocable Trust DocumentDocument10 pagesIrrevocable Trust Documentpezet100100% (20)

- Self Settled TrustDocument3 pagesSelf Settled TrustAnonymous Ax12P2srNo ratings yet

- How To Unlock An Irrevocable Trust For Maximum Advantage - Provident Trust GroupDocument4 pagesHow To Unlock An Irrevocable Trust For Maximum Advantage - Provident Trust GroupLew Payne67% (3)

- Discretionary Trust FormDocument12 pagesDiscretionary Trust Formlerosenoir100% (1)

- Non Statutory Trust AgreementDocument23 pagesNon Statutory Trust Agreementterrorjoy100% (33)

- Common Law TrustDocument17 pagesCommon Law TrustTrey Sells97% (64)

- Trust - Land Trust in Real Estate Transactions III 2008Document38 pagesTrust - Land Trust in Real Estate Transactions III 2008Alvin Chartrand100% (1)

- Common Law Biz Trust SampleDocument12 pagesCommon Law Biz Trust Samplejoe blahNo ratings yet

- Trust InstructionsDocument9 pagesTrust Instructionsunapanther100% (1)

- TN Pour Over Will SampleDocument0 pagesTN Pour Over Will SampledennisborcherNo ratings yet

- Your Georgia Wills, Trusts, & Estates Explained Simply: Important Information You Need to Know for Georgia ResidentsFrom EverandYour Georgia Wills, Trusts, & Estates Explained Simply: Important Information You Need to Know for Georgia ResidentsNo ratings yet

- Trust InstructionsDocument99 pagesTrust InstructionsAhtazaban95% (20)

- Asset ProtectionDocument2 pagesAsset Protection05C1LL473No ratings yet

- Deed of Trust - p4PDocument10 pagesDeed of Trust - p4Plerosenoir100% (2)

- Revocable Living TrustDocument5 pagesRevocable Living Trustapi-246909910100% (3)

- Irrevocable TrustDocument6 pagesIrrevocable Trustunapanther100% (6)

- Free Business Trust ManualDocument101 pagesFree Business Trust ManualHarry100% (7)

- Lichtenstein Family TrustDocument38 pagesLichtenstein Family TrustTerry Lichtenstein100% (1)

- Nokia - Web Based Provision Configuration Guide For Symbian ClientsDocument9 pagesNokia - Web Based Provision Configuration Guide For Symbian ClientstestnationNo ratings yet

- Book 4 Music AlphabeticalDocument1 pageBook 4 Music AlphabeticaltestnationNo ratings yet

- Tooth-Organ Meridian Chart: Sense Organs Joints Spinal Segments Vertebrae OrgansDocument1 pageTooth-Organ Meridian Chart: Sense Organs Joints Spinal Segments Vertebrae Organsmoumona100% (1)

- How To Flip The Magnet On Spooky Remote v1.1Document4 pagesHow To Flip The Magnet On Spooky Remote v1.1testnationNo ratings yet

- Book 2 Music AlphabeticalDocument1 pageBook 2 Music AlphabeticaltestnationNo ratings yet

- Book 2 Music - CompleteDocument1 pageBook 2 Music - CompletetestnationNo ratings yet

- Due Diligence QuestionnaireDocument5 pagesDue Diligence QuestionnairetestnationNo ratings yet

- Book Music Master List Alphabetical v2Document1 pageBook Music Master List Alphabetical v2testnationNo ratings yet

- Book 8 Music Piano ListDocument2 pagesBook 8 Music Piano ListtestnationNo ratings yet

- Book 6: Faithfully (Journey) For The First Time v3 Right Here Waiting That's What Friends Are ForDocument2 pagesBook 6: Faithfully (Journey) For The First Time v3 Right Here Waiting That's What Friends Are FortestnationNo ratings yet

- Book 6 Music AlphabeticalDocument2 pagesBook 6 Music AlphabeticaltestnationNo ratings yet

- Book 2 Music - CompleteDocument1 pageBook 2 Music - CompletetestnationNo ratings yet

- Book 3 Music Piano ListDocument1 pageBook 3 Music Piano ListtestnationNo ratings yet

- Book 3 Music AlphabeticalDocument1 pageBook 3 Music AlphabeticaltestnationNo ratings yet

- FileDocument5 pagesFiletestnationNo ratings yet

- Move BGL Software To A New Stand-Alone PC or LaptopDocument13 pagesMove BGL Software To A New Stand-Alone PC or LaptoptestnationNo ratings yet

- Book 7 Music PianoDocument1 pageBook 7 Music PianotestnationNo ratings yet

- Book 5 Music AlphabeticalDocument1 pageBook 5 Music AlphabeticaltestnationNo ratings yet

- Book 7 Music Alphabetical PianoDocument1 pageBook 7 Music Alphabetical PianotestnationNo ratings yet

- FilelistingDocument5 pagesFilelistingtestnationNo ratings yet

- Homeopathic Potencies For Remedy MakerDocument1 pageHomeopathic Potencies For Remedy MakertestnationNo ratings yet

- The Energy Grid - Harmonic 695 PDFDocument1 pageThe Energy Grid - Harmonic 695 PDFtestnationNo ratings yet

- Funding Your Retirement Max Newnham P 266-267 PDFDocument1 pageFunding Your Retirement Max Newnham P 266-267 PDFtestnationNo ratings yet

- Spooky2 4 GeneratorsDocument9 pagesSpooky2 4 Generatorstestnation100% (1)

- Australian Trailer Plug Wiring InfoDocument1 pageAustralian Trailer Plug Wiring InfotestnationNo ratings yet

- Funding Your Retirement Max Newnham P 266-267Document1 pageFunding Your Retirement Max Newnham P 266-267testnationNo ratings yet

- Healing Codes WorkbookDocument77 pagesHealing Codes Workbookdeepflm100% (1)

- NONLINEAR (NLS) DIAGNOSTIC SYSTEMS (Basic Physics and Principles of Equipment)Document13 pagesNONLINEAR (NLS) DIAGNOSTIC SYSTEMS (Basic Physics and Principles of Equipment)testnation100% (1)

- 2011 Giant Cypress 3 SpecificationsDocument2 pages2011 Giant Cypress 3 SpecificationstestnationNo ratings yet

- 2011 Giant Suede SpecificationsDocument1 page2011 Giant Suede SpecificationstestnationNo ratings yet

- Azotic Coating Technology, Inc. v. Orient International Jewelry Trading, Inc. Et Al - Document No. 15Document2 pagesAzotic Coating Technology, Inc. v. Orient International Jewelry Trading, Inc. Et Al - Document No. 15Justia.comNo ratings yet

- Article 1157Document2 pagesArticle 1157Eliza Jayne Princess VizcondeNo ratings yet

- RIIHAN306A Carry Out Lifting Using Multiple Cranes: Release: 1Document11 pagesRIIHAN306A Carry Out Lifting Using Multiple Cranes: Release: 1Gia Minh Tieu TuNo ratings yet

- 88 - People Vs SenerisDocument8 pages88 - People Vs SenerisAnonymous CWcXthhZgxNo ratings yet

- Percentage Distribution of CICL by Sex: Age No. Percent 10 11 12 13 14 15 16 17 18 TotalDocument8 pagesPercentage Distribution of CICL by Sex: Age No. Percent 10 11 12 13 14 15 16 17 18 TotalShefferd BernalesNo ratings yet

- Civ QuamtoDocument71 pagesCiv QuamtoBee CG100% (1)

- Module 3 - Architectural CodeDocument41 pagesModule 3 - Architectural CodeRovic VincentNo ratings yet

- Air and Space LawDocument52 pagesAir and Space LawBharath SimhaReddyNaidu100% (1)

- Mechanic's LienDocument3 pagesMechanic's LienRocketLawyer71% (7)

- May Free Chapter - The Watch by Joydeep Roy-BhattacharyaDocument37 pagesMay Free Chapter - The Watch by Joydeep Roy-BhattacharyaRandomHouseAUNo ratings yet

- The Village Reporter - March 5th, 2014Document20 pagesThe Village Reporter - March 5th, 2014thevillagereporterNo ratings yet

- USDOR 0911-1013 Ab - Part5Document250 pagesUSDOR 0911-1013 Ab - Part5TeaPartyCheerNo ratings yet

- A.K. Jain Constitution 2nd Part PDFDocument353 pagesA.K. Jain Constitution 2nd Part PDFPragalbh Bhardwaj100% (1)

- Jesse U. Lucas V Jesus S. Lucas G.R. No. 190710 June 6, 2011 FactsDocument2 pagesJesse U. Lucas V Jesus S. Lucas G.R. No. 190710 June 6, 2011 FactsMichelle Valdez AlvaroNo ratings yet

- Group Assignment - IL - Mohd Izwan and Mohd Sukry-1Document46 pagesGroup Assignment - IL - Mohd Izwan and Mohd Sukry-1MohdIzwanNo ratings yet

- Maintenance Muslim Law ProjectDocument13 pagesMaintenance Muslim Law ProjectCharit MudgilNo ratings yet

- ElevatorDocument37 pagesElevatorVijayakumarVageesan100% (1)

- Fire Safety FacadesDocument58 pagesFire Safety Facadessloane01No ratings yet

- Canillo vs. Angeles DigestDocument3 pagesCanillo vs. Angeles DigestEmir Mendoza100% (2)

- Balindong vs. CA, G.R. Nos. 177600 and 178684, 19 October 2015Document3 pagesBalindong vs. CA, G.R. Nos. 177600 and 178684, 19 October 2015Gwendelyn Peñamayor-MercadoNo ratings yet

- Andres vs. Manufacturers Hanover Trust CorporationDocument9 pagesAndres vs. Manufacturers Hanover Trust Corporationral cbNo ratings yet

- Property DigestDocument2 pagesProperty DigestLen-Len CobsilenNo ratings yet

- CIB Industrial ReportDocument4 pagesCIB Industrial ReportWilliam HarrisNo ratings yet

- PLM vs. IAC PDFDocument17 pagesPLM vs. IAC PDFAivan Charles TorresNo ratings yet

- Consultant For Development and Operation of National Data and Analytics Platform (NDAP)Document157 pagesConsultant For Development and Operation of National Data and Analytics Platform (NDAP)antara choudhury khannaNo ratings yet

- Legaspi V. City of CebuDocument1 pageLegaspi V. City of CebuNico RavilasNo ratings yet

- Victimology Chapter 2Document3 pagesVictimology Chapter 2seanleboeuf100% (1)

- Thinking Skills and Problem Solving - Gang Violence 2Document16 pagesThinking Skills and Problem Solving - Gang Violence 2Shamma ThaufeeqNo ratings yet

- Unlawful Detainer Complaint 12.23.19Document33 pagesUnlawful Detainer Complaint 12.23.19GeekWireNo ratings yet

- Interview Questions For Student Visa (Australia) : Annual Fee)Document2 pagesInterview Questions For Student Visa (Australia) : Annual Fee)Azam ShaikhNo ratings yet