You might also like

- CHAPTER 42 - Accounting For Income TaxDocument18 pagesCHAPTER 42 - Accounting For Income TaxJoshua Wacangan100% (1)

- Notes in Preferential TaxationDocument57 pagesNotes in Preferential TaxationJeremae Ann Ceriaco100% (1)

- 2010 Illustrative Fs Sme Final Clean New - UnlockedDocument74 pages2010 Illustrative Fs Sme Final Clean New - UnlockedKendall JennerNo ratings yet

- Tax Practice Set ReviewerDocument9 pagesTax Practice Set Reviewerjjay_santosNo ratings yet

- HO1 - Accounting For Income TaxDocument5 pagesHO1 - Accounting For Income TaxCharlesNo ratings yet

- Module 02 - Bases Conversion and Development ActDocument22 pagesModule 02 - Bases Conversion and Development ActKyla Shmily GonzagaNo ratings yet

- Accounting For Income TaxesDocument25 pagesAccounting For Income TaxesKulet AkoNo ratings yet

- Module 1 PPT Introduction To TaxDocument24 pagesModule 1 PPT Introduction To TaxAhmad Farhad TaneenNo ratings yet

- Accounting Cash Definition ReconciliationDocument10 pagesAccounting Cash Definition ReconciliationjoannaberroNo ratings yet

- Auditing Special Purpose Financial StatementsDocument18 pagesAuditing Special Purpose Financial StatementscolleenyuNo ratings yet

- Notes To FsDocument10 pagesNotes To FsCynthia PenoliarNo ratings yet

- Lecture On Share Based Payments Share Appreciation RightsDocument8 pagesLecture On Share Based Payments Share Appreciation RightsChristine AltamarinoNo ratings yet

- INTACC 3.1LN Presentation of Financial StatementsDocument9 pagesINTACC 3.1LN Presentation of Financial StatementsAlvin BaternaNo ratings yet

- Quizz Chapter 21Document9 pagesQuizz Chapter 21Rachel EnokouNo ratings yet

- Government Accounting'Document22 pagesGovernment Accounting'Jayvee FelipeNo ratings yet

- Accounting for Payroll ProceduresDocument15 pagesAccounting for Payroll ProceduresDenise Aubrey GallardoNo ratings yet

- Toa Interim ReportingDocument17 pagesToa Interim ReportingEmmanuel SarmientoNo ratings yet

- Ifrs 9Document80 pagesIfrs 9Veer Pratab SinghNo ratings yet

- Topic 5a - Audit of Property - Plant and EquipmentDocument20 pagesTopic 5a - Audit of Property - Plant and EquipmentLANGITBIRUNo ratings yet

- Compound Financial InstrumentsDocument3 pagesCompound Financial Instrumentskevior2No ratings yet

- Ais Conversion CycleDocument51 pagesAis Conversion CycleAms Penaflor100% (6)

- At-5909 Risk AssessmentDocument8 pagesAt-5909 Risk AssessmentVeron BrionesNo ratings yet

- Taxn 3100 Instructional Module 1 PDFDocument5 pagesTaxn 3100 Instructional Module 1 PDFSandyNo ratings yet

- Framework of Philippine Standards On AuditingDocument2 pagesFramework of Philippine Standards On AuditingKaye SyNo ratings yet

- KY-385 KUCHEF Multi-Cooker IM-V1.2Document40 pagesKY-385 KUCHEF Multi-Cooker IM-V1.2al83rt777750% (2)

- Income Taxation Finals Quiz 2Document7 pagesIncome Taxation Finals Quiz 2Jericho DupayaNo ratings yet

- Pas 12 Income TaxesDocument4 pagesPas 12 Income TaxesFabrienne Kate Eugenio LiberatoNo ratings yet

- Johnstone - 9e - Auditing - Chapter 10 - PPT FINALDocument93 pagesJohnstone - 9e - Auditing - Chapter 10 - PPT FINALNurlinaEzzati0% (1)

- Audit - Sales and ReceivablesDocument6 pagesAudit - Sales and ReceivablesValentina Tan DuNo ratings yet

- Investment in AssociateDocument11 pagesInvestment in AssociateElla MontefalcoNo ratings yet

- Auditor's Responses To Assessed RisksDocument41 pagesAuditor's Responses To Assessed RisksPatrick GoNo ratings yet

- Quiz Discontinued OperationDocument2 pagesQuiz Discontinued OperationRose0% (1)

- Chapter 18 Policies Estimates and ErrorsDocument28 pagesChapter 18 Policies Estimates and ErrorsHammad Ahmad100% (1)

- Accounting Students Exam GAAP and Financial ReportingDocument7 pagesAccounting Students Exam GAAP and Financial ReportingJohnAllenMarillaNo ratings yet

- 3 Module 3 - Notes To Financial Statements AE 17 Intermediate Accounting 3Document14 pages3 Module 3 - Notes To Financial Statements AE 17 Intermediate Accounting 3CJ Granada100% (1)

- 13Document63 pages13amysilverbergNo ratings yet

- Controlling Payroll Cost - Critical Disciplines for Club ProfitabilityFrom EverandControlling Payroll Cost - Critical Disciplines for Club ProfitabilityNo ratings yet

- Chapter 6-Audit ReportDocument14 pagesChapter 6-Audit ReportDawit WorkuNo ratings yet

- IAS 16 Property Plant Equipment AccountingDocument6 pagesIAS 16 Property Plant Equipment AccountinghemantbaidNo ratings yet

- IAS 1 Presentation of Financial Statements PDFDocument4 pagesIAS 1 Presentation of Financial Statements PDFTEE YAN YING UnknownNo ratings yet

- Adjusting EntriesDocument43 pagesAdjusting EntriesCH Umair MerryNo ratings yet

- PAS 27 Consolidated and Separate FS ReviewedDocument14 pagesPAS 27 Consolidated and Separate FS ReviewedRonalynPuatuNo ratings yet

- Acc Business Combination NotesDocument118 pagesAcc Business Combination NotesTheresaNo ratings yet

- Agreed Upon Procedures vs. Consulting EngagementsDocument49 pagesAgreed Upon Procedures vs. Consulting EngagementsCharles B. Hall100% (1)

- Financial Asset MILLANDocument6 pagesFinancial Asset MILLANAlelie Joy dela CruzNo ratings yet

- PFRS 8 - Operating SegmentsDocument13 pagesPFRS 8 - Operating SegmentsYassi CurtisNo ratings yet

- Tax PlanningDocument21 pagesTax Planningpriyani0% (1)

- Income Tax Schemes, Accounting Periods, Accounting Methods and Reporting C4Document73 pagesIncome Tax Schemes, Accounting Periods, Accounting Methods and Reporting C4Diane CassionNo ratings yet

- StrataxDocument40 pagesStrataxAsh PadillaNo ratings yet

- TOPIC 3e - Risk and MaterialityDocument33 pagesTOPIC 3e - Risk and MaterialityLANGITBIRUNo ratings yet

- Accounting For Income TaxesDocument16 pagesAccounting For Income TaxesMUNAWAR ALI100% (5)

- Module 13 Regular Deductions 3Document16 pagesModule 13 Regular Deductions 3Donna Mae FernandezNo ratings yet

- The Petty Cash FundDocument10 pagesThe Petty Cash FundLilian TaiNo ratings yet

- Audit of General Insurance CompaniesDocument16 pagesAudit of General Insurance CompaniesTACS & CO.No ratings yet

- 015 - Quick-Notes - Financial Liabilities From Borrowings Part 2Document3 pages015 - Quick-Notes - Financial Liabilities From Borrowings Part 2Zatsumono YamamotoNo ratings yet

- Module 9 SHAREHOLDERS' EQUITYDocument3 pagesModule 9 SHAREHOLDERS' EQUITYNiño Mendoza MabatoNo ratings yet

- CH04 Revenue Cycle PDFDocument73 pagesCH04 Revenue Cycle PDFZion Ilagan0% (1)

- Ias 12Document45 pagesIas 12Reever RiverNo ratings yet

- Company Accounting - Powerpoint PresentationDocument29 pagesCompany Accounting - Powerpoint Presentationtammy_yau3199100% (1)

- Tax Effect Accounting (AASB 1020)Document40 pagesTax Effect Accounting (AASB 1020)Queenlizzie LamSamNo ratings yet

- Revenue and Construction ContractsDocument7 pagesRevenue and Construction ContractsHenry ListerNo ratings yet

- EquityDocument7 pagesEquityHenry ListerNo ratings yet

- Accounting For Financial InstrumentsDocument13 pagesAccounting For Financial InstrumentsHenry ListerNo ratings yet

- Financial Accounting StudyDocument9 pagesFinancial Accounting StudyHenry ListerNo ratings yet

- Extractive IndustriesDocument5 pagesExtractive IndustriesHenry ListerNo ratings yet

- Accounting For Provisions and Contingent LiabilitiesDocument8 pagesAccounting For Provisions and Contingent LiabilitiesHenry Lister100% (1)

- Guzman Cruz Cpas and Co.: Guideline For BIR Tax Deadlines During Enhanced Community Quarantine (ECQ) PeriodDocument2 pagesGuzman Cruz Cpas and Co.: Guideline For BIR Tax Deadlines During Enhanced Community Quarantine (ECQ) PeriodGerald SantosNo ratings yet

- Condition TypeDocument18 pagesCondition TypeDeepak SangramsinghNo ratings yet

- Income Taxation (TAX 101) TH Quiz No.3 ScoreDocument3 pagesIncome Taxation (TAX 101) TH Quiz No.3 ScoreMaricel MielNo ratings yet

- Invoice For Portable Toilets - Nuggets ParadeDocument1 pageInvoice For Portable Toilets - Nuggets Parade9newsNo ratings yet

- Law of Taxation Law-I Course SyllabusDocument2 pagesLaw of Taxation Law-I Course SyllabusAmanNo ratings yet

- Generator Registration Fees (El - Tax) Generator Registration Fees (El - Tax) Generator Registration Fees (El - Tax)Document1 pageGenerator Registration Fees (El - Tax) Generator Registration Fees (El - Tax) Generator Registration Fees (El - Tax)aaanathanNo ratings yet

- Assignment No. 4Document3 pagesAssignment No. 4Paula VillarubiaNo ratings yet

- Assessing public financial management frameworksDocument24 pagesAssessing public financial management frameworksSamer_AbdelMaksoudNo ratings yet

- Corruption PDFDocument19 pagesCorruption PDFJuan ValerNo ratings yet

- GST NotesDocument156 pagesGST NotesNishthaNo ratings yet

- F6ZWE 2015 Jun ADocument8 pagesF6ZWE 2015 Jun APhebieon MukwenhaNo ratings yet

- Tax.103 2 Corporate Income Taxation StudentsDocument23 pagesTax.103 2 Corporate Income Taxation StudentsJames R JunioNo ratings yet

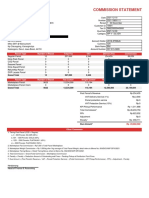

- Commission Statement: Mitra InformationDocument3 pagesCommission Statement: Mitra InformationZia Chusnul LabibNo ratings yet

- Answer KeyDocument13 pagesAnswer KeyRoronoa Zoro100% (1)

- Tax Q and A 1Document2 pagesTax Q and A 1Marivie UyNo ratings yet

- Tax AmnestyDocument3 pagesTax Amnestyapi-236234542No ratings yet

- .Apr 2022Document10 pages.Apr 2022SWAPNIL JADHAVNo ratings yet

- Starter Checklist v1.0Document2 pagesStarter Checklist v1.0Akalisue Hatebreeder TheopoisondigipackNo ratings yet

- Tax Invoice: 36AADCM3491M1Z2 30AAACC6253G1Z6Document1 pageTax Invoice: 36AADCM3491M1Z2 30AAACC6253G1Z6VIDHI JAINENDRASINH RANANo ratings yet

- Payroll TanodDocument2 pagesPayroll TanodRosalie Sareno Alvior100% (2)

- Payslip Summary for Rahul DasDocument3 pagesPayslip Summary for Rahul DasasdNo ratings yet

- Reconciling Bank Deposits and Interest Items for 7 YearsDocument4 pagesReconciling Bank Deposits and Interest Items for 7 YearsJerwin Cases TiamsonNo ratings yet

- Cpa Review School of The Philippines ManilaDocument5 pagesCpa Review School of The Philippines ManilaSamuel Cedrick AbalosNo ratings yet

- CIR v. Algue, Inc., G.R. No. L-28896Document1 pageCIR v. Algue, Inc., G.R. No. L-28896fay garneth buscato100% (2)

- Phil. Health ContributionsDocument5 pagesPhil. Health Contributionshae123467% (9)

- ABC Co. Started Its OperationsDocument1 pageABC Co. Started Its OperationsQueen ValleNo ratings yet

- Country Responses To The Financial Crisis KosovoDocument39 pagesCountry Responses To The Financial Crisis KosovoInternational Consortium on Governmental Financial Management50% (2)

- Lifeblood DoctrineDocument1 pageLifeblood DoctrineEric Roy Malik0% (1)

- Exercises 5-1 Taxation SolutionsDocument56 pagesExercises 5-1 Taxation SolutionsDevonNo ratings yet

- 1.MFRS 112Document46 pages1.MFRS 112Yau Xiang Ying100% (1)