You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- CH 11Document28 pagesCH 11Mike Cheshire0% (1)

- Masterlist of Position Category Updated 10.25.2021Document20 pagesMasterlist of Position Category Updated 10.25.2021johnmarcNo ratings yet

- Medi-Caps University, Indore: Department of Management Studies and CommerceDocument21 pagesMedi-Caps University, Indore: Department of Management Studies and CommercePiyush ManwaniNo ratings yet

- AmazonDocument4 pagesAmazonNehas22No ratings yet

- Air SHS Abm PM-Q4 Mod13Document15 pagesAir SHS Abm PM-Q4 Mod13TOZAMANo ratings yet

- Types of Exchange RateDocument15 pagesTypes of Exchange RateAnu KumariNo ratings yet

- CBSE Economics Class 11 Term 1 Objective Question BankDocument144 pagesCBSE Economics Class 11 Term 1 Objective Question BankMohammed Roshan100% (3)

- Brand Equity Management SystemDocument13 pagesBrand Equity Management SystemVarun SrivastavaNo ratings yet

- Loyalty Presentation - Net CarrotsDocument15 pagesLoyalty Presentation - Net CarrotsNisha TrivediNo ratings yet

- STMT CASH 001 CAPA018903 Nov2022-2Document8 pagesSTMT CASH 001 CAPA018903 Nov2022-2Diana diazNo ratings yet

- Variable IC Mock Exam - 02062020 PDFDocument30 pagesVariable IC Mock Exam - 02062020 PDFMikaella Sarmiento100% (1)

- The Fundamentals of Customer AcquisitionDocument39 pagesThe Fundamentals of Customer AcquisitionMandarinaNo ratings yet

- Product ObsolescenceDocument7 pagesProduct ObsolescenceARPITA SELOTNo ratings yet

- SIP REPORT On Angel BrokingDocument80 pagesSIP REPORT On Angel BrokingPrajwal BNo ratings yet

- ID Fresh Foods Group 2Document9 pagesID Fresh Foods Group 2Shivam TripathiNo ratings yet

- Marketing Management PDFDocument226 pagesMarketing Management PDFjhonNo ratings yet

- Home Assignment On Elasticity of DemandDocument3 pagesHome Assignment On Elasticity of DemandSk Ahasanur Rahman 1935043681No ratings yet

- Bank of BarodaDocument111 pagesBank of BarodaRahul Kr JhaNo ratings yet

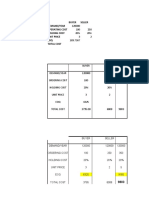

- Buyer Seller Demand/Year Operating Cost Holding Cost Unit Price EOQ Total CostDocument7 pagesBuyer Seller Demand/Year Operating Cost Holding Cost Unit Price EOQ Total CostNeha SmritiNo ratings yet

- Shadow of Smart MoneyDocument61 pagesShadow of Smart MoneyRonnie Romero100% (1)

- SubhikshaDocument31 pagesSubhikshaPradeep BandiNo ratings yet

- Micro-U4L2A44-How Many Workers Should Be HiredDocument2 pagesMicro-U4L2A44-How Many Workers Should Be HiredAdvika PunjeNo ratings yet

- Quiz 1 Study GuideDocument7 pagesQuiz 1 Study Guideusernames358No ratings yet

- Test BankDocument269 pagesTest BankmerveNo ratings yet

- Market AnomaliesDocument3 pagesMarket AnomaliesAusama MemonNo ratings yet

- Managerial EconomicsDocument20 pagesManagerial Economics4PredicationNo ratings yet

- Lesson 1 Introduction To Agricultural MarketingDocument3 pagesLesson 1 Introduction To Agricultural MarketingSittie Ainah MacapundagNo ratings yet

- Introducing and Naming New Products and Brand ExtensionsDocument16 pagesIntroducing and Naming New Products and Brand ExtensionsHUỲNH TRẦN THIỆN PHÚCNo ratings yet

- Master The MarketsDocument144 pagesMaster The Marketsicm6394% (16)

- Market Mechanism in Economics: Examples and GraphsDocument11 pagesMarket Mechanism in Economics: Examples and Graphskripasini balajiNo ratings yet