You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- NPTEL Week 7Document4 pagesNPTEL Week 7Dippal IsraniNo ratings yet

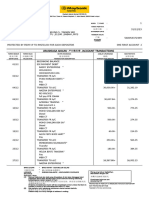

- Statement of Account: PageDocument6 pagesStatement of Account: PageSyedFarhanNo ratings yet

- Csit 101 Assignment 1Document4 pagesCsit 101 Assignment 1api-266983757No ratings yet

- Banking 1Document69 pagesBanking 1Shaifali GargNo ratings yet

- Statement 2710201701575611Document3 pagesStatement 2710201701575611Rohit Sunil Deshmukh100% (1)

- 3 New MessagesDocument1 page3 New Messagesjohnjuni300No ratings yet

- Final Report: Submitted By: TAIMOOR RIAZ 13044954-030 Submitted ToDocument65 pagesFinal Report: Submitted By: TAIMOOR RIAZ 13044954-030 Submitted ToSherryMirzaNo ratings yet

- Myhomem 2 UcommondashboardcasaDocument1 pageMyhomem 2 UcommondashboardcasaMuhammad DanialNo ratings yet

- TVL CSS11 Q4 M8Document16 pagesTVL CSS11 Q4 M8Richard Sugbo100% (1)

- Cancellation Request PDFDocument1 pageCancellation Request PDFScarlett RMNo ratings yet

- O Level Project 2Document17 pagesO Level Project 2PRINCENo ratings yet

- Accounting For DiscountsDocument2 pagesAccounting For DiscountsYamateNo ratings yet

- Amit Project GeneralDocument2 pagesAmit Project GeneralKrishna YadavNo ratings yet

- e-StatementBRImo 581201036477530 Oct2023 20231110 175401Document1 pagee-StatementBRImo 581201036477530 Oct2023 20231110 175401MuhammadIqbalHanafiNo ratings yet

- F Inv 433Document1 pageF Inv 433alsone07No ratings yet

- Ibs Lahad Datu 1 31/12/23Document4 pagesIbs Lahad Datu 1 31/12/23fidatulsyafikahsamsualam12No ratings yet

- Change Advice Letter For Customer PaymentsDocument1 pageChange Advice Letter For Customer PaymentsLiu Inn100% (2)

- Armwood Bus StopsDocument6 pagesArmwood Bus StopsTelerica JonesNo ratings yet

- HCIA-LTE Training Material V1.0 PrintDocument60 pagesHCIA-LTE Training Material V1.0 PrintSunday Olusegun OlasugbaNo ratings yet

- 13 Audit Notes For CA Final by CA Ashish GoyalDocument159 pages13 Audit Notes For CA Final by CA Ashish GoyalSuhag Patel100% (3)

- Quotation For New Internet Connection PDFDocument8 pagesQuotation For New Internet Connection PDFMayank 5040No ratings yet

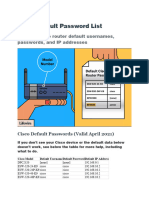

- Cisco Default Password ListDocument5 pagesCisco Default Password ListSiles Sandel100% (1)

- ST Asd Cra23 BtaDocument6 pagesST Asd Cra23 BtaFabiola FonsecaNo ratings yet

- ADvendio To Offer Free of Charge Google Doubleclick Dart Sales Manager (DSM) Data MigrationDocument3 pagesADvendio To Offer Free of Charge Google Doubleclick Dart Sales Manager (DSM) Data MigrationPR.comNo ratings yet

- Tota Sneha 3.0 YearsDocument2 pagesTota Sneha 3.0 YearsPrajjwal SinghNo ratings yet

- MGT 330 FinalDocument13 pagesMGT 330 FinalKANIZ FATEMANo ratings yet

- Simplex ES Net 1-2 Launch BulletinDocument7 pagesSimplex ES Net 1-2 Launch BulletinRodrigo Lima100% (1)

- Madura14e Ch07 FinalDocument33 pagesMadura14e Ch07 FinalfabianngxinlongNo ratings yet

- Colorplast Presentation BM PDFDocument34 pagesColorplast Presentation BM PDFSahibzada NizamuddinNo ratings yet

- Assignment: Software Defined Networking (SDN)Document12 pagesAssignment: Software Defined Networking (SDN)Rosemelyne WartdeNo ratings yet