You might also like

- Alfalaval UVvsECDocument13 pagesAlfalaval UVvsECDeepak ShoriNo ratings yet

- ItfDocument3 pagesItfDeepak Shori100% (1)

- PDF 1Document45 pagesPDF 1Deepak ShoriNo ratings yet

- Safety Data Sheet: Product Name: MOBILGARD 540Document11 pagesSafety Data Sheet: Product Name: MOBILGARD 540Deepak ShoriNo ratings yet

- FocDocument7 pagesFocDeepak ShoriNo ratings yet

- Autocar Spare Parts Price SurveyDocument10 pagesAutocar Spare Parts Price SurveyDeepak ShoriNo ratings yet

- IMO News - Autumn Issue - 2017Document36 pagesIMO News - Autumn Issue - 2017Deepak ShoriNo ratings yet

- SofDocument2 pagesSofDeepak ShoriNo ratings yet

- Ethics in ShipbrokingDocument4 pagesEthics in ShipbrokingDeepak ShoriNo ratings yet

- ItfDocument3 pagesItfDeepak Shori100% (1)

- EthicsDocument8 pagesEthicsDeepak ShoriNo ratings yet

- Variance AnalysisDocument1 pageVariance AnalysisDeepak ShoriNo ratings yet

- Ship ManagementDocument24 pagesShip ManagementDeepak ShoriNo ratings yet

- IccDocument3 pagesIccDeepak ShoriNo ratings yet

- Special Circular: Revised Himalaya Clause For Bills of Lading and Other ContractsDocument3 pagesSpecial Circular: Revised Himalaya Clause For Bills of Lading and Other ContractsDeepak ShoriNo ratings yet

- Updated Glossary in Co TermsDocument13 pagesUpdated Glossary in Co TermsDeepak ShoriNo ratings yet

- Law of TortsDocument41 pagesLaw of TortsDeepak ShoriNo ratings yet

- IntroductionDocument2 pagesIntroductionDeepak ShoriNo ratings yet

- Public and Private CompanyDocument22 pagesPublic and Private CompanyDeepak ShoriNo ratings yet

- Public and Private CompanyDocument22 pagesPublic and Private CompanyDeepak ShoriNo ratings yet

- 01 IntroductiontoTransportationDocument23 pages01 IntroductiontoTransportationDeepak ShoriNo ratings yet

- UC40+ User GuideDocument2 pagesUC40+ User GuideDeepak ShoriNo ratings yet

- Adler V Dickson The HimalayaDocument18 pagesAdler V Dickson The HimalayaDeepak ShoriNo ratings yet

- Ics Exams 2013 Questions SLDocument1 pageIcs Exams 2013 Questions SLDeepak ShoriNo ratings yet

- Ics Exams 2013 Questions SFDocument2 pagesIcs Exams 2013 Questions SFDeepak Shori100% (1)

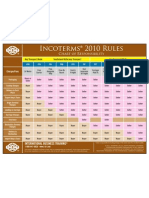

- Incoterms 2010 at A GlanceDocument1 pageIncoterms 2010 at A GlanceAftab UddinNo ratings yet

- Ics Exams 2013 Questions SBDocument1 pageIcs Exams 2013 Questions SBDeepak ShoriNo ratings yet

- Port Agency 2014Document3 pagesPort Agency 2014Deepak Shori100% (1)

- Ics Exams 2013 Questions SSPDocument2 pagesIcs Exams 2013 Questions SSPDeepak ShoriNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Credit Insurance PPT BasicDocument8 pagesCredit Insurance PPT Basicshikha82No ratings yet

- Indigo ProspectusDocument557 pagesIndigo Prospectusvbt999123yahoo100% (1)

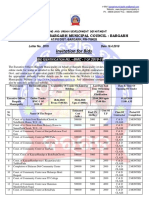

- Invitation For Bids: Office of The Bargarh Municipal Council: BargarhDocument3 pagesInvitation For Bids: Office of The Bargarh Municipal Council: BargarhANJANI KUMAR SRIWASNo ratings yet

- 1allianz PDFDocument26 pages1allianz PDFFarah Najeehah ZolkalpliNo ratings yet

- Bos 28432 CP 14Document53 pagesBos 28432 CP 14Basant Ojha100% (1)

- Employer's Annual Federal Unemployment (FUTA) Tax ReturnDocument4 pagesEmployer's Annual Federal Unemployment (FUTA) Tax ReturnFrank LamNo ratings yet

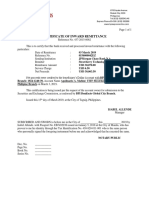

- Certificate of Inward RemittanceDocument1 pageCertificate of Inward RemittanceLauriz EsquivelNo ratings yet

- Summer Tranning Report (NPA)Document66 pagesSummer Tranning Report (NPA)shagunNo ratings yet

- Merger Report of HDFC-CBOP by Atmakuri RammohanDocument23 pagesMerger Report of HDFC-CBOP by Atmakuri RammohanRam Mohan Atmakuri100% (21)

- Extracts of The Minutes of The Meeting of The Board of Directors of UDAYAN FINSTOCK PVTDocument3 pagesExtracts of The Minutes of The Meeting of The Board of Directors of UDAYAN FINSTOCK PVTmaheshwariNo ratings yet

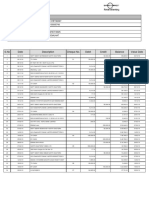

- Account Statement From 1 Jan 2021 To 31 Jan 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Jan 2021 To 31 Jan 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancevenkNo ratings yet

- Policy For Issuing CurriculumDocument7 pagesPolicy For Issuing Curriculumrichi_roma18No ratings yet

- Sber Bank User GuideDocument62 pagesSber Bank User GuidearunmirandaNo ratings yet

- Section 125 Digested CasesDocument6 pagesSection 125 Digested CasesRobNo ratings yet

- MarketingofFinancialServices FlyerDocument3 pagesMarketingofFinancialServices FlyerJeet SinghNo ratings yet

- Mda CibcDocument12 pagesMda CibcAlexandertheviNo ratings yet

- MBA Finance ProjectDocument73 pagesMBA Finance Projectsabaris477No ratings yet

- Trade Repository08112017Document14 pagesTrade Repository08112017speedenquiryNo ratings yet

- Loans & AdvancesDocument97 pagesLoans & AdvancesVishal Vish50% (4)

- Chapter 29 Procedures and Reports On Special Purpose Audit EngagementsDocument30 pagesChapter 29 Procedures and Reports On Special Purpose Audit EngagementsClar Aaron BautistaNo ratings yet

- I. What Is Equitable Mortgage?Document6 pagesI. What Is Equitable Mortgage?Jhon Allain HisolaNo ratings yet

- Zaid Ahmad PDFDocument1 pageZaid Ahmad PDFzaidNo ratings yet

- Functional DocumentDocument16 pagesFunctional DocumentKotresh NerkiNo ratings yet

- BALANCE CASH HOLDING AssignDocument3 pagesBALANCE CASH HOLDING AssignJarra Abdurahman100% (2)

- MHI AuthorisationDocument21 pagesMHI Authorisationnainesh959No ratings yet

- Week 1-5Document2 pagesWeek 1-5Or Gio100% (1)

- PDFDocument1 pagePDFAnkit JainNo ratings yet

- UCO Bank Repo Linked LoansDocument5 pagesUCO Bank Repo Linked LoansAshutoshNo ratings yet

- Actuarial 2Document33 pagesActuarial 2Rochana RamanayakaNo ratings yet

- Clinton Iraq EmailDocument4 pagesClinton Iraq EmailandrewperezdcNo ratings yet