You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Recent Trends in GLOBAL TRADE of Developing CountriesDocument32 pagesRecent Trends in GLOBAL TRADE of Developing CountriesVarsha JaisinghaniNo ratings yet

- BFM PDFDocument30 pagesBFM PDFVarsha Jaisinghani100% (1)

- Credit Card FinalDocument73 pagesCredit Card FinalVarsha JaisinghaniNo ratings yet

- Credit Card FinalDocument73 pagesCredit Card FinalVarsha JaisinghaniNo ratings yet

- Mergers and AcquisitionDocument60 pagesMergers and AcquisitionVarsha JaisinghaniNo ratings yet

- Credit Card FinalDocument73 pagesCredit Card FinalVarsha JaisinghaniNo ratings yet

- Mergers and AcquisitionDocument61 pagesMergers and AcquisitionVarsha JaisinghaniNo ratings yet

- Mergers and AcquisitionDocument61 pagesMergers and AcquisitionVarsha JaisinghaniNo ratings yet

- As-2 Valuation of Inventories2Document19 pagesAs-2 Valuation of Inventories2Varsha JaisinghaniNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- PSG Ex - 8.2PSG Ex - 8.2 - Monthly Report Template - Monthly Report TemplateDocument25 pagesPSG Ex - 8.2PSG Ex - 8.2 - Monthly Report Template - Monthly Report TemplateJohn WilliamsNo ratings yet

- BS Assignment - ExcelDocument63 pagesBS Assignment - ExcelSOURABH DENo ratings yet

- Planning Tools and Techniques: With Duane WeaverDocument24 pagesPlanning Tools and Techniques: With Duane WeaverAbdirahmanNo ratings yet

- Boston Creamery, IncDocument10 pagesBoston Creamery, IncAto SumartoNo ratings yet

- Reston Association: Review of The Tetra/Lake House Project, StoneTurn Group, February 28, 2017Document31 pagesReston Association: Review of The Tetra/Lake House Project, StoneTurn Group, February 28, 2017Terry MaynardNo ratings yet

- 8508Document9 pages8508ZunairaAslamNo ratings yet

- International Organisations QuestionsDocument22 pagesInternational Organisations QuestionsparapiripoNo ratings yet

- SAP Funds Management Configuration-FMDocument59 pagesSAP Funds Management Configuration-FMLiordi74% (27)

- 2024 2025 Proposed BudgetDocument255 pages2024 2025 Proposed BudgetWVLT NewsNo ratings yet

- Assessment of Government Budgetary Control Procedures and Utilization (In Case of Hawassa University)Document22 pagesAssessment of Government Budgetary Control Procedures and Utilization (In Case of Hawassa University)samuel debebe100% (1)

- Key Findings in The Forensic Investigation of The Public DebtDocument21 pagesKey Findings in The Forensic Investigation of The Public DebtRob G.No ratings yet

- OS ReportDocument72 pagesOS ReportPrasanth C NairNo ratings yet

- Budgetary ControlDocument29 pagesBudgetary ControlJagadeesh MohanNo ratings yet

- Personal Financial Planning 14th Edition Billingsley Test BankDocument56 pagesPersonal Financial Planning 14th Edition Billingsley Test BankBen Williams100% (37)

- Marketing Plan ProposalDocument2 pagesMarketing Plan ProposalRachel Phoon QianweiNo ratings yet

- Top 20 Financial KPIs Every CFO Dashboard Should HaveDocument5 pagesTop 20 Financial KPIs Every CFO Dashboard Should HavekPrasad80% (1)

- Financial Management in The Sport Industry 2nd Brown Solution Manual DownloadDocument12 pagesFinancial Management in The Sport Industry 2nd Brown Solution Manual DownloadElizabethLewisixmt100% (41)

- Easthampton Mayor Nicole LaChapelle Advertises For Chief of StaffDocument4 pagesEasthampton Mayor Nicole LaChapelle Advertises For Chief of StaffMary Serreze100% (1)

- Lawyers Against Monopoly and Poverty (Lamp) vs. The Secretary of Budget and Management, GR No. 164987 April 24, 2012Document7 pagesLawyers Against Monopoly and Poverty (Lamp) vs. The Secretary of Budget and Management, GR No. 164987 April 24, 2012Ashley Kate PatalinjugNo ratings yet

- A3 BSBFIM501 Manage Budgets and Financial PlansDocument5 pagesA3 BSBFIM501 Manage Budgets and Financial PlansMaya Roton0% (1)

- Lo Council Packet 2Document144 pagesLo Council Packet 2api-50056604No ratings yet

- Tutorial Budget StudentDocument4 pagesTutorial Budget StudentDanial NorazmanNo ratings yet

- Sample Fresher MBA ResumeDocument6 pagesSample Fresher MBA ResumeAshish ChauhanNo ratings yet

- Chapter 09 Testbank Solution Manual Management AccountingDocument47 pagesChapter 09 Testbank Solution Manual Management AccountingTrinh LêNo ratings yet

- Case Studies Internal ControlDocument3 pagesCase Studies Internal Controlakq153No ratings yet

- Financial Management Operations Manual (Fmom)Document29 pagesFinancial Management Operations Manual (Fmom)Tawagin Mo Akong MertsNo ratings yet

- JTN FY16 Guidelines - FINALDocument9 pagesJTN FY16 Guidelines - FINALYaacov MaymanNo ratings yet

- Controlling-2012 20130211075746.531 XDocument217 pagesControlling-2012 20130211075746.531 XSatyadev PulipakaNo ratings yet

- Solved The Following Budget Data Are For A Country Having Both PDFDocument1 pageSolved The Following Budget Data Are For A Country Having Both PDFM Bilal SaleemNo ratings yet

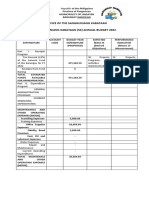

- Office of The Sangguniang Kabataan Sangguniang Kabataan (SK) Annual Budget 2022Document11 pagesOffice of The Sangguniang Kabataan Sangguniang Kabataan (SK) Annual Budget 2022John Reybren Malogan100% (1)