You might also like

- Judicial. IRS Form56Document66 pagesJudicial. IRS Form56Shane Christopher Family of Buczek94% (17)

- Answering Brief of Defendants-Appellees: Ronald Pierce et al vs. Chief Justice Tani Cantil-Sakauye Judicial Council Chair and Steven Jahr Judicial Council Administrative Director - Federal Class Action Lawsuit for Alleged Illegal Use of California Vexatious Litigant Law by Family Court Judges in Child Custody Disputes - Ventura County - Tulare County - Sacramento County - San Mateo County - Santa Clara County - Riverside County - San Francisco County - US District Court for the Northern District of California Judge Jeffrey S. White - US Courts for the Ninth Circuit - 9th Circuit Court of Appeal Class Action for Injunctive and Declaratory ReliefDocument171 pagesAnswering Brief of Defendants-Appellees: Ronald Pierce et al vs. Chief Justice Tani Cantil-Sakauye Judicial Council Chair and Steven Jahr Judicial Council Administrative Director - Federal Class Action Lawsuit for Alleged Illegal Use of California Vexatious Litigant Law by Family Court Judges in Child Custody Disputes - Ventura County - Tulare County - Sacramento County - San Mateo County - Santa Clara County - Riverside County - San Francisco County - US District Court for the Northern District of California Judge Jeffrey S. White - US Courts for the Ninth Circuit - 9th Circuit Court of Appeal Class Action for Injunctive and Declaratory ReliefCalifornia Judicial Branch News Service - Investigative Reporting Source Material & Story Ideas100% (1)

- Procurement Manual: Network of Centers For Civic Engagement (Ncce)Document10 pagesProcurement Manual: Network of Centers For Civic Engagement (Ncce)RodasNo ratings yet

- Internal Audit ManualDocument7 pagesInternal Audit ManualAdolph Christian GonzalesNo ratings yet

- New Audit Plan ISADocument6 pagesNew Audit Plan ISAindrawanNo ratings yet

- What Is The Difference Between Authorization and ApprovalDocument1 pageWhat Is The Difference Between Authorization and ApprovalbilmNo ratings yet

- NGO GuidelinesDocument116 pagesNGO GuidelinesSusman786100% (3)

- Consolidations: Ifrs 10 IAS 27Document93 pagesConsolidations: Ifrs 10 IAS 27Sadiq AhmedNo ratings yet

- Accountant TestDocument3 pagesAccountant TestMax SuperNo ratings yet

- CFA Level 1 (Book-B)Document170 pagesCFA Level 1 (Book-B)butabutt100% (1)

- Complete Revision Notes Auditing 1Document90 pagesComplete Revision Notes Auditing 1Marwin Ace100% (1)

- Per User Guide and Logbook2Document76 pagesPer User Guide and Logbook2Anthony LawNo ratings yet

- CIA P1 SII Independence and ObjectivityDocument47 pagesCIA P1 SII Independence and ObjectivityJayAr Dela Rosa100% (1)

- Eyob Finance ManualDocument46 pagesEyob Finance ManualMiki DeregeNo ratings yet

- Ffp-English-Finance and Accounting Manual - v3 PDFDocument78 pagesFfp-English-Finance and Accounting Manual - v3 PDFTin Zaw ThantNo ratings yet

- Audit Practices ManualDocument354 pagesAudit Practices ManualRaif QelaNo ratings yet

- Example of A Management Representation LetterDocument2 pagesExample of A Management Representation LettersonicefuNo ratings yet

- Financial Statements and Performance Analysis: DR Leslie Mitchell Financial ControlDocument31 pagesFinancial Statements and Performance Analysis: DR Leslie Mitchell Financial Controlosaleemi100% (1)

- Boracay Foundation, Inc. v. Province of AklanDocument3 pagesBoracay Foundation, Inc. v. Province of Aklankjhenyo21850263% (8)

- Fundamentals of AuditingDocument3 pagesFundamentals of AuditingRashid Khan Safi100% (1)

- Evidence Case Digests 1Document37 pagesEvidence Case Digests 1Ken ArnozaNo ratings yet

- Cruz vs. Cristobal 498 SCRA 37, August 07, 2006Document7 pagesCruz vs. Cristobal 498 SCRA 37, August 07, 2006HaroldDeLeonNo ratings yet

- The Cash Basis IPSAS An Alternative ViewDocument7 pagesThe Cash Basis IPSAS An Alternative ViewInternational Consortium on Governmental Financial ManagementNo ratings yet

- Chapter 1 Audit f8 - 2.3Document25 pagesChapter 1 Audit f8 - 2.3JosephineMicheal17No ratings yet

- Lagos State Local Government Audit ManualDocument217 pagesLagos State Local Government Audit ManualAndy Wynne100% (1)

- CRPC Notes by CCSDocument6 pagesCRPC Notes by CCSPunam ChauhanNo ratings yet

- The Nature and Operations of The IASBDocument12 pagesThe Nature and Operations of The IASBTran AnhNo ratings yet

- 5.public Sector AuditDocument15 pages5.public Sector AuditMtanaNo ratings yet

- Audit CodeDocument140 pagesAudit CodeKhurram SherazNo ratings yet

- Local Govt-Audit ManualDocument131 pagesLocal Govt-Audit ManualNoah Mzyece DhlaminiNo ratings yet

- True and Fair View of Financial StatementsDocument2 pagesTrue and Fair View of Financial Statementsbhaibahi0% (1)

- Local Gov, Statutory Bodies, Public EntDocument17 pagesLocal Gov, Statutory Bodies, Public EntethandanfordNo ratings yet

- Financial Reporting and EthicsDocument309 pagesFinancial Reporting and EthicsOlabisi OdewoleNo ratings yet

- IPSAS in Your Pocket - January 2021Document61 pagesIPSAS in Your Pocket - January 2021Megha AgarwalNo ratings yet

- Commercial Audit ManualDocument404 pagesCommercial Audit ManualMohit SharmaNo ratings yet

- Fundamentals of Financial Auditing 1Document24 pagesFundamentals of Financial Auditing 1Raja Ghufran Arif100% (1)

- UntitledDocument21 pagesUntitleddhirajpironNo ratings yet

- ISQC1 What's New-01.02.18 PDFDocument13 pagesISQC1 What's New-01.02.18 PDFTumi Makatane MasekanaNo ratings yet

- Public Sector AccountingDocument458 pagesPublic Sector AccountingIssa AdiemaNo ratings yet

- Deloitte Au Audit Chart Accounts 0812Document31 pagesDeloitte Au Audit Chart Accounts 0812Suman Beemisetty100% (1)

- QMF Approved and CirculatedDocument78 pagesQMF Approved and CirculatedMuhammad Amir Usman100% (1)

- Advanced Taxation - United Kingdom (ATX-UK) : Syllabus and Study GuideDocument25 pagesAdvanced Taxation - United Kingdom (ATX-UK) : Syllabus and Study GuideIsavic AlsinaNo ratings yet

- Statutory Audit ModuleDocument75 pagesStatutory Audit ModulecaanusinghNo ratings yet

- Permanent File FormatDocument14 pagesPermanent File Formatgmk_t84No ratings yet

- Practitioner's Guide To Audit of Small EntitiesDocument315 pagesPractitioner's Guide To Audit of Small Entitiesswat2kk5No ratings yet

- 17-BSA 700 and 705Document16 pages17-BSA 700 and 705Sohel Rana100% (1)

- International Standard of AuditingDocument4 pagesInternational Standard of AuditingSuvro AvroNo ratings yet

- Past Year Acw 482 - Analysis and Development of Accounting Information System June 08Document7 pagesPast Year Acw 482 - Analysis and Development of Accounting Information System June 08Nabila69No ratings yet

- Audit Procedure in BangladeshDocument14 pagesAudit Procedure in BangladeshSahed UzzamanNo ratings yet

- Audit and Assurance Singapore ACCADocument7 pagesAudit and Assurance Singapore ACCAwguateNo ratings yet

- Public Sector Auditing My Homework and Discussion AnswersDocument25 pagesPublic Sector Auditing My Homework and Discussion AnswersLoganPearcy100% (1)

- Audit Chapter 3Document18 pagesAudit Chapter 3Nur ShahiraNo ratings yet

- Chap 17Document34 pagesChap 17ridaNo ratings yet

- Audit Manual PDFDocument33 pagesAudit Manual PDFSaiful AnwarNo ratings yet

- F7 Technical ArticlesDocument121 pagesF7 Technical ArticlesNicquain0% (1)

- ISA 240 Summary: The Auditor's Responsibilities Relating To Fraud in An Audit of Financial StatementsDocument4 pagesISA 240 Summary: The Auditor's Responsibilities Relating To Fraud in An Audit of Financial StatementsAnonymous XlHWbwyeq5100% (1)

- Chap 1 - Text Accounting TheoryDocument36 pagesChap 1 - Text Accounting TheoryAhmadYaseen100% (2)

- اسئلة انترفيو محاسبة عربي وانجليزىDocument22 pagesاسئلة انترفيو محاسبة عربي وانجليزىmustafa1001No ratings yet

- Audit of Trade Receivables and Sales BalancesDocument2 pagesAudit of Trade Receivables and Sales BalancesDiane VillarmaNo ratings yet

- Auditing NotesDocument65 pagesAuditing NotesTushar GaurNo ratings yet

- Lecture 10 Audit FinalisationDocument21 pagesLecture 10 Audit FinalisationShibin Jayaprasad100% (1)

- How To Prepare Projected Financial StatementsDocument4 pagesHow To Prepare Projected Financial StatementsNamy Lyn GumameraNo ratings yet

- Payslip Sample 1111Document1 pagePayslip Sample 1111顺蔡No ratings yet

- The Auditing ProfessionDocument10 pagesThe Auditing Professionmqondisi nkabindeNo ratings yet

- Generally Accepted Auditing Standards A Complete Guide - 2020 EditionFrom EverandGenerally Accepted Auditing Standards A Complete Guide - 2020 EditionNo ratings yet

- Concept Note of The Proposed ResearchDocument3 pagesConcept Note of The Proposed ResearchMtanaNo ratings yet

- IIA Calender 2019Document5 pagesIIA Calender 2019MtanaNo ratings yet

- EconomicsDocument11 pagesEconomicsMtanaNo ratings yet

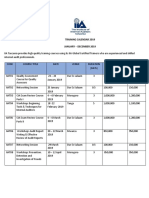

- Training Calender 2020 PDFDocument5 pagesTraining Calender 2020 PDFMtana100% (1)

- Training Calender 2020 PDFDocument5 pagesTraining Calender 2020 PDFMtana100% (1)

- PaperDocument15 pagesPaperMtanaNo ratings yet

- Economic AssignmentDocument1 pageEconomic AssignmentMtanaNo ratings yet

- Finance Term PaperDocument10 pagesFinance Term PaperMtanaNo ratings yet

- Marketing AnalysisDocument8 pagesMarketing AnalysisMtanaNo ratings yet

- 460 Term Paper ExampleDocument18 pages460 Term Paper ExampleLyra Kay BatiancilaNo ratings yet

- Presentation On The New Nbaa Bylaws: Registration and Practicing Bylaws 2017 By: Agnes Kessy (Adv.) 28 April 2017Document23 pagesPresentation On The New Nbaa Bylaws: Registration and Practicing Bylaws 2017 By: Agnes Kessy (Adv.) 28 April 2017MtanaNo ratings yet

- Electronic World Trade Platform: FactsheetDocument1 pageElectronic World Trade Platform: FactsheetMtanaNo ratings yet

- Principles of Fraud Detection Part1Document2 pagesPrinciples of Fraud Detection Part1MtanaNo ratings yet

- Term Paper GuidelinesDocument8 pagesTerm Paper GuidelinesNer InnNo ratings yet

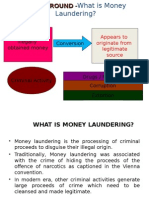

- Accountants Annual Conference - Overview of Money LaunderingDocument23 pagesAccountants Annual Conference - Overview of Money LaunderingMtanaNo ratings yet

- 2 How MGMT Perpetrates FraudDocument3 pages2 How MGMT Perpetrates FraudMtanaNo ratings yet

- Misappropriation of AssetsDocument2 pagesMisappropriation of AssetsMtanaNo ratings yet

- Environmental Audititing 2006Document15 pagesEnvironmental Audititing 2006MtanaNo ratings yet

- Accountants Annual Conference - Overview of Money LaunderingDocument23 pagesAccountants Annual Conference - Overview of Money LaunderingMtanaNo ratings yet

- Transport RoomDocument4 pagesTransport Roomsabatino123No ratings yet

- United States v. Vincent Sumpter, 4th Cir. (2012)Document5 pagesUnited States v. Vincent Sumpter, 4th Cir. (2012)Scribd Government DocsNo ratings yet

- Bradford v. Cobb County Sheriff&apos S Department Et Al - Document No. 4Document2 pagesBradford v. Cobb County Sheriff&apos S Department Et Al - Document No. 4Justia.comNo ratings yet

- Res JudiceDocument4 pagesRes JudiceSandeep SinghNo ratings yet

- 649 653Document6 pages649 653Clifford TubanaNo ratings yet

- United States Court of Appeals, Third CircuitDocument2 pagesUnited States Court of Appeals, Third CircuitScribd Government DocsNo ratings yet

- United States v. Alfred Erdos, 474 F.2d 157, 4th Cir. (1973)Document8 pagesUnited States v. Alfred Erdos, 474 F.2d 157, 4th Cir. (1973)Scribd Government DocsNo ratings yet

- Administrative Tribunal ProjectDocument17 pagesAdministrative Tribunal ProjectAnsh Patel100% (1)

- State of M.P. v. Narayan Singh and Ors.Document2 pagesState of M.P. v. Narayan Singh and Ors.Siddharth Badkul100% (1)

- 122 Autencio vs. MañaraDocument11 pages122 Autencio vs. MañaraBory SanotsNo ratings yet

- Motion To Produce Suspect From Police CustodyDocument5 pagesMotion To Produce Suspect From Police CustodyosianemoNo ratings yet

- James Earle v. Robert Benoit, 850 F.2d 836, 1st Cir. (1988)Document26 pagesJames Earle v. Robert Benoit, 850 F.2d 836, 1st Cir. (1988)Scribd Government DocsNo ratings yet

- United States Court of Appeals, Fourth CircuitDocument2 pagesUnited States Court of Appeals, Fourth CircuitScribd Government DocsNo ratings yet

- Kafker Final 4Document13 pagesKafker Final 4New England Law ReviewNo ratings yet

- Proposed OrderDocument9 pagesProposed OrderABC Action NewsNo ratings yet

- United States v. Adewale Aladekoba, 4th Cir. (2012)Document3 pagesUnited States v. Adewale Aladekoba, 4th Cir. (2012)Scribd Government DocsNo ratings yet

- Crispin D. Baizas and Associates For Petitioners. Isidro T. Almeda For RespondentsDocument33 pagesCrispin D. Baizas and Associates For Petitioners. Isidro T. Almeda For RespondentselCrisNo ratings yet

- Republic of The Philippines Vs Hidalgo, 534 SCRA 619Document13 pagesRepublic of The Philippines Vs Hidalgo, 534 SCRA 619Vince EnageNo ratings yet

- Jay Morton v. Jack W. Browne, 438 F.2d 1205, 1st Cir. (1971)Document2 pagesJay Morton v. Jack W. Browne, 438 F.2d 1205, 1st Cir. (1971)Scribd Government DocsNo ratings yet

- Ajit Yadav OrderDocument44 pagesAjit Yadav OrderAjit YadavNo ratings yet

- United States v. Lonnie Whatley, 11th Cir. (2013)Document47 pagesUnited States v. Lonnie Whatley, 11th Cir. (2013)Scribd Government DocsNo ratings yet

- G.R. No. 78994 March 11, 1988 Jose Acuna Bautista, Also Known As "Ramon Revilla", vs. Commission On ElectionsDocument7 pagesG.R. No. 78994 March 11, 1988 Jose Acuna Bautista, Also Known As "Ramon Revilla", vs. Commission On ElectionsrethiramNo ratings yet

- Garcia Fule v. CADocument12 pagesGarcia Fule v. CARichard KoNo ratings yet

- PersonalWeb Technologies v. Amazon Web Services Et. Al.Document16 pagesPersonalWeb Technologies v. Amazon Web Services Et. Al.PriorSmartNo ratings yet