You might also like

- A Very Interesting Read About Disease-Specific Costing GuidelineDocument10 pagesA Very Interesting Read About Disease-Specific Costing GuidelineJeisson MorenoNo ratings yet

- Rev4 - Epp - Unit Cost RS - RD Rosyadi - 05 12 2021Document7 pagesRev4 - Epp - Unit Cost RS - RD Rosyadi - 05 12 2021rosyd rosyadiNo ratings yet

- Acumen Medicare MedicaidDocument184 pagesAcumen Medicare MedicaidAgeNo ratings yet

- The Impact of Agglomeration Economies On Hospital Input PricesDocument4 pagesThe Impact of Agglomeration Economies On Hospital Input PricesGuillermo RodriguezNo ratings yet

- The Marketing Challenges of Healthcare Enterpreeurship An Emperical Invesigation in NigeriaDocument17 pagesThe Marketing Challenges of Healthcare Enterpreeurship An Emperical Invesigation in NigeriaHumming BirdNo ratings yet

- Demand Estimation, Elasticity, and Forecating of Medicam ToothpasteDocument17 pagesDemand Estimation, Elasticity, and Forecating of Medicam Toothpastesaeedawais47No ratings yet

- Scope of Health EconomicsDocument33 pagesScope of Health EconomicsSanjeev Chougule100% (2)

- Costing Princples and Business Control Systems (Assessement Criteria 1.1)Document22 pagesCosting Princples and Business Control Systems (Assessement Criteria 1.1)asus13018333% (3)

- Kiss ADocument22 pagesKiss AJean M Huaman FiallegaNo ratings yet

- 5 Cost Behaviors and Cost Structure of Public Hospitals in India - Analysis From The Perspective of Congestion CostsDocument10 pages5 Cost Behaviors and Cost Structure of Public Hospitals in India - Analysis From The Perspective of Congestion CostsChitranshu ChandelNo ratings yet

- Module 6-Key Attributes of Cost AnalysesDocument3 pagesModule 6-Key Attributes of Cost AnalysesLou CalderonNo ratings yet

- 7Ps in Corporate Hospitals - Administrators' Perspective: Full Length Research PaperDocument17 pages7Ps in Corporate Hospitals - Administrators' Perspective: Full Length Research Paperjohn488No ratings yet

- Document PDFDocument17 pagesDocument PDFwempieNo ratings yet

- BCG Competing On Outcomes Nov 2013 Tcm80-149649Document0 pagesBCG Competing On Outcomes Nov 2013 Tcm80-149649Yuddy SaputraNo ratings yet

- Walker, 2011 The Methods of Cost Effectiveness Analysis To InformDocument32 pagesWalker, 2011 The Methods of Cost Effectiveness Analysis To InformSeah Jia huiNo ratings yet

- Supervised Consumption Site Enables Cost Savings BDocument7 pagesSupervised Consumption Site Enables Cost Savings BnalgatronNo ratings yet

- Capitation Payment Method As A Policy Tool, Versus Fee For Services, or The Financial Sustainability of The National Health Insurance in Sudan: Algadarif State Case Study.Document15 pagesCapitation Payment Method As A Policy Tool, Versus Fee For Services, or The Financial Sustainability of The National Health Insurance in Sudan: Algadarif State Case Study.National Graduate ConferenceNo ratings yet

- Moving From Specific To Generic: Generic Modelling in Health CareDocument5 pagesMoving From Specific To Generic: Generic Modelling in Health CareoptisearchNo ratings yet

- A Literature Review On The Identification of Variables For Measuring Hospital Efficiency in The Data Envelopment Analysis (DEA)Document15 pagesA Literature Review On The Identification of Variables For Measuring Hospital Efficiency in The Data Envelopment Analysis (DEA)Nokky Farra FazriaNo ratings yet

- Book of Abstract, V2.0Document296 pagesBook of Abstract, V2.0Nitin Dhir KhatriNo ratings yet

- Fortis 1)Document62 pagesFortis 1)ravitsinghairNo ratings yet

- A Literature Review of Indirect Costs Associated With StrokeDocument7 pagesA Literature Review of Indirect Costs Associated With Strokec5j2ksrgNo ratings yet

- Quality Improvement in Reducing Falls in A Medical-Surgical-TelemDocument41 pagesQuality Improvement in Reducing Falls in A Medical-Surgical-Telemtahani tttNo ratings yet

- Policy Suggestions To Obama Transition TeamDocument3 pagesPolicy Suggestions To Obama Transition Teamhuffpostfund100% (1)

- AHA BundledPayment ReportDocument20 pagesAHA BundledPayment Reportbikram2128100% (1)

- The Direct Medical Costs Of: Healthcare-Associated Infections in U.S. Hospitals and The Benefits of PreventionDocument16 pagesThe Direct Medical Costs Of: Healthcare-Associated Infections in U.S. Hospitals and The Benefits of PreventionjnplnceNo ratings yet

- Patients Perception of Service Quality Towards in Hospitals of Dakshina Kannada District of KarnatakaDocument8 pagesPatients Perception of Service Quality Towards in Hospitals of Dakshina Kannada District of KarnatakaIJAR JOURNALNo ratings yet

- GS China Hospitals Jan2014Document31 pagesGS China Hospitals Jan2014Sanghoon JiNo ratings yet

- An Analysis On Marketing Mix in Hospitals: Related PapersDocument22 pagesAn Analysis On Marketing Mix in Hospitals: Related PapersTriska AFNo ratings yet

- Westminster International University Coursework SubmissionDocument11 pagesWestminster International University Coursework SubmissionMurodullo BazarovNo ratings yet

- NRES Thesis - Chapter 1 3Y3-7Document16 pagesNRES Thesis - Chapter 1 3Y3-7acorpuz_4No ratings yet

- Application of ABC in Healthcare IndustriesDocument3 pagesApplication of ABC in Healthcare IndustriesVijayalakshmi SridharNo ratings yet

- Effect of Costing Methods On Unit Cost of Hospital Medical ServicesDocument10 pagesEffect of Costing Methods On Unit Cost of Hospital Medical Servicesbarkiest24No ratings yet

- Excellence in Diagnostic CareDocument20 pagesExcellence in Diagnostic CareDominic LiangNo ratings yet

- Hospital Payment Systems Based On Diagnosis-Related Groups: Experiences in Low-And Middle-Income CountriesDocument12 pagesHospital Payment Systems Based On Diagnosis-Related Groups: Experiences in Low-And Middle-Income CountriesRaditya TriNo ratings yet

- Activity Based ManagementDocument26 pagesActivity Based Managementfortune90100% (2)

- Coordinating Health ServicesDocument25 pagesCoordinating Health ServicesbdivanNo ratings yet

- Hospital BenchmarkingDocument11 pagesHospital BenchmarkingDana ApostolNo ratings yet

- Accounting DissertationDocument9 pagesAccounting DissertationAngela NixxNo ratings yet

- Running Head: Feasibility Study of New Line of Service in Health Industry 1Document13 pagesRunning Head: Feasibility Study of New Line of Service in Health Industry 1Faustino Licud IIINo ratings yet

- Standart CostingDocument13 pagesStandart Costingboba milkNo ratings yet

- Dghpsim: Supporting Smart Thinking To Improve Hospital PerformanceDocument7 pagesDghpsim: Supporting Smart Thinking To Improve Hospital Performancearnold FernandezNo ratings yet

- Overbooking Italian Helthcare Center (Simpler)Document13 pagesOverbooking Italian Helthcare Center (Simpler)nikhilaNo ratings yet

- Cost Accounting Practices in BangladeshDocument21 pagesCost Accounting Practices in BangladeshSourav MahadiNo ratings yet

- Using Propensity Score Methods To Analyse Individual Patient Level Cost Effectiveness Data From Observational StudiesDocument33 pagesUsing Propensity Score Methods To Analyse Individual Patient Level Cost Effectiveness Data From Observational Studiesrks_rmrctNo ratings yet

- Contemporary Accting Res - 2014 - Holzhacker - The Impact of Changes in Regulation On Cost BehaviorDocument33 pagesContemporary Accting Res - 2014 - Holzhacker - The Impact of Changes in Regulation On Cost BehaviorMohamed EL-MihyNo ratings yet

- Activity Based Costing Model in Laboratory of Care Hospital: Ali Habibi Dr. Kamal Javanmard Ravi Kumar TatiDocument11 pagesActivity Based Costing Model in Laboratory of Care Hospital: Ali Habibi Dr. Kamal Javanmard Ravi Kumar TatiraviktatiNo ratings yet

- 1 SMDocument8 pages1 SMTantri Widiana PutriNo ratings yet

- Implementasi Metode Activity Based Costing Dalam Menentukan Unit Cost Poliklinik (Studi Kasus Pada Rumah Sakit Nasional Diponegoro)Document8 pagesImplementasi Metode Activity Based Costing Dalam Menentukan Unit Cost Poliklinik (Studi Kasus Pada Rumah Sakit Nasional Diponegoro)Tantri Widiana PutriNo ratings yet

- Economic and Social Burden of Severe SepsisDocument11 pagesEconomic and Social Burden of Severe SepsisolfianyNo ratings yet

- Application of Quality Function Deployment in Healthcare Services: A ReviewDocument8 pagesApplication of Quality Function Deployment in Healthcare Services: A ReviewIJRASETPublicationsNo ratings yet

- Pharmaceutical Services Cost Analysis Using Time-Driven Activity-Based Costing: A Contribution To Improve Community Pharmacies' ManagementDocument11 pagesPharmaceutical Services Cost Analysis Using Time-Driven Activity-Based Costing: A Contribution To Improve Community Pharmacies' ManagementKuntoro Flieg Nach ÖsterreichNo ratings yet

- How To Determine Cost Effective Analysis - RatikaDocument14 pagesHow To Determine Cost Effective Analysis - Ratikatifanny carolinaNo ratings yet

- Economic EvaluationDocument4 pagesEconomic Evaluationkajojo joyNo ratings yet

- Cost BenefitDocument11 pagesCost BenefitGabriel EllisNo ratings yet

- Industry Healthcare AnalysisDocument31 pagesIndustry Healthcare AnalysisMirza Farhan BegNo ratings yet

- Hirsch: by Ruchlin andDocument16 pagesHirsch: by Ruchlin andredha craftNo ratings yet

- Cost Analysis of Mirwais and Nangarhar Regional Hospitals in AfghanistanDocument12 pagesCost Analysis of Mirwais and Nangarhar Regional Hospitals in AfghanistanNational Graduate ConferenceNo ratings yet

- Introduction to Clinical Effectiveness and Audit in HealthcareFrom EverandIntroduction to Clinical Effectiveness and Audit in HealthcareNo ratings yet

- EIB Working Papers 2019/06 - Promoting energy audits: Results from an experimentFrom EverandEIB Working Papers 2019/06 - Promoting energy audits: Results from an experimentNo ratings yet

- Tecnia Journal Vol 6 No1Document85 pagesTecnia Journal Vol 6 No1chaitanya23No ratings yet

- Practical ComponentDocument10 pagesPractical Componentchaitanya23No ratings yet

- BM Module 7Document24 pagesBM Module 7chaitanya23No ratings yet

- Projectreport 141008015527 Conversion Gate01Document78 pagesProjectreport 141008015527 Conversion Gate01chaitanya23No ratings yet

- Solution-Services Management (14mbamm303)Document22 pagesSolution-Services Management (14mbamm303)chaitanya23No ratings yet

- Mba I Accounting For Management (14mba13) AssignmentDocument1 pageMba I Accounting For Management (14mba13) Assignmentchaitanya23No ratings yet

- Management Lessons On An Aircraft Carrier at SeaDocument5 pagesManagement Lessons On An Aircraft Carrier at Seachaitanya23No ratings yet

- PartexDocument11 pagesPartexMirza Mehedi AlamNo ratings yet

- Basics of ExcelDocument79 pagesBasics of Excelchaitanya23No ratings yet

- Mba I Accounting For Management (14mba13) SolutionDocument9 pagesMba I Accounting For Management (14mba13) Solutionchaitanya23No ratings yet

- Mba III Services Management (14mbamm303) NotesDocument113 pagesMba III Services Management (14mbamm303) NotesZoheb Ali K100% (14)

- Solution-Services Management (14mbamm303)Document22 pagesSolution-Services Management (14mbamm303)chaitanya23No ratings yet

- Consumer Learning Schiffman07Document55 pagesConsumer Learning Schiffman07chaitanya23No ratings yet

- Question Paper Services Management (14mbamm303)Document2 pagesQuestion Paper Services Management (14mbamm303)chaitanya23No ratings yet

- Mba-i-Accounting For Management (14mba13) - Question PaperDocument2 pagesMba-i-Accounting For Management (14mba13) - Question Paperchaitanya23No ratings yet

- ABCDocument5 pagesABCchaitanya23No ratings yet

- Question Paper Services Management (14mbamm303)Document2 pagesQuestion Paper Services Management (14mbamm303)chaitanya23No ratings yet

- YuanDocument18 pagesYuanchaitanya23No ratings yet

- Personality Test ResultDocument8 pagesPersonality Test Resultchaitanya23No ratings yet

- YuanDocument18 pagesYuanchaitanya23No ratings yet

- Toyota ProjectDocument12 pagesToyota Projectchaitanya23No ratings yet

- Marginal Costing ResearchDocument5 pagesMarginal Costing Researchchaitanya23No ratings yet

- Factoral DesignsDocument24 pagesFactoral Designschaitanya23No ratings yet

- QuestionaireDocument4 pagesQuestionairechaitanya23No ratings yet

- BRM (M-4)Document33 pagesBRM (M-4)chaitanya23No ratings yet

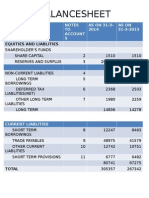

- Balance SheetDocument4 pagesBalance Sheetchaitanya23No ratings yet

- The Recent Gang Rape of A 23Document4 pagesThe Recent Gang Rape of A 23chaitanya23No ratings yet

- Maruti Suzuki Bal Sheet AnalysisDocument13 pagesMaruti Suzuki Bal Sheet Analysischaitanya23No ratings yet

- Trial Memorandum of The PetitionerDocument11 pagesTrial Memorandum of The PetitionerAbegail Protacio GuardianNo ratings yet

- Journalism of Courage: SINCE 1932Document16 pagesJournalism of Courage: SINCE 1932kulvir singNo ratings yet

- Request For Check Replacement Form: Dr. Trifony D. LuchanaDocument1 pageRequest For Check Replacement Form: Dr. Trifony D. LuchanaReslyn YanocNo ratings yet

- HealthInsurance-forIndiasMissingMiddle 28-10-2021 230116 211000Document65 pagesHealthInsurance-forIndiasMissingMiddle 28-10-2021 230116 211000Amit PaliwalNo ratings yet

- The Cham 18 NovDocument2 pagesThe Cham 18 NovKevin PhaomeiNo ratings yet

- War's Offensive On Women - The Humanitarian Challenge in Bosnia, Kosovo, and Afghanistan by Julie A. Mertus (2000)Document176 pagesWar's Offensive On Women - The Humanitarian Challenge in Bosnia, Kosovo, and Afghanistan by Julie A. Mertus (2000)Anonymous yu09qxYCM100% (1)

- State of New Jersey Medicaid Fraud Division Provider Exclusion ReportDocument109 pagesState of New Jersey Medicaid Fraud Division Provider Exclusion ReportppstreloNo ratings yet

- Welcome Home - A Guide To Services For TCHC Tenants - 2012Document122 pagesWelcome Home - A Guide To Services For TCHC Tenants - 2012amanda_cain_4No ratings yet

- SB 5 As Passed by The SenateDocument294 pagesSB 5 As Passed by The SenateED. DICKAUNo ratings yet

- SOPs of Oakdale TandooriDocument4 pagesSOPs of Oakdale TandooriSalman M. AhmedNo ratings yet

- OSHA Hazard Alert Reports Preventable Incidents That CertifyMeOnline - Com Aims To AddressDocument3 pagesOSHA Hazard Alert Reports Preventable Incidents That CertifyMeOnline - Com Aims To AddressPR.comNo ratings yet

- Notice of Cmucat Result: Central Mindanao UniversityDocument2 pagesNotice of Cmucat Result: Central Mindanao UniversityLANI JOY TABAMONo ratings yet

- CDC Built Environment AssessDocument112 pagesCDC Built Environment AssessPaco TrooperNo ratings yet

- Living Will...Document14 pagesLiving Will...gilbertmalcolmNo ratings yet

- Scaffolds ChecklistDocument6 pagesScaffolds ChecklistYuli RahmawatiNo ratings yet

- Edristi August English 2018Document103 pagesEdristi August English 2018shivam_2607No ratings yet

- Construction Manager/ Desalination Plant Resident Engineer: Job DescriptionDocument3 pagesConstruction Manager/ Desalination Plant Resident Engineer: Job DescriptionYr QuerubinNo ratings yet

- PRUlink One EngDocument11 pagesPRUlink One Engsabrewilde29No ratings yet

- Notice: Valid Existing Rights Determination Requests: Daniel Boone National Forest, KY Existing Forest Service Road UseDocument5 pagesNotice: Valid Existing Rights Determination Requests: Daniel Boone National Forest, KY Existing Forest Service Road UseJustia.comNo ratings yet

- Comment Draft Report Appendices (Rev 1)Document175 pagesComment Draft Report Appendices (Rev 1)dangatz4763No ratings yet

- Essex County District Attorney's Report On The Police Shooting of Denis ReynosoDocument5 pagesEssex County District Attorney's Report On The Police Shooting of Denis Reynosobaystateexaminer0% (1)

- Non Binary Gender FactsheetDocument3 pagesNon Binary Gender Factsheetapi-283123617No ratings yet

- Proposal For King's Inn Site in Kingston, NYDocument4 pagesProposal For King's Inn Site in Kingston, NYDaily FreemanNo ratings yet

- User'S Manual: Workloadindicators OfstaffingneedDocument56 pagesUser'S Manual: Workloadindicators OfstaffingneedKang DjamalNo ratings yet

- HSWA 1974 Main PointsDocument2 pagesHSWA 1974 Main Pointsdestiny910No ratings yet

- Philippine environmental laws on air and water pollutionDocument12 pagesPhilippine environmental laws on air and water pollutionIELTSNo ratings yet

- Manila Standard Today - Monday (September 24, 2012) IssueDocument16 pagesManila Standard Today - Monday (September 24, 2012) IssueManila Standard TodayNo ratings yet

- Winter Internship ReportDocument13 pagesWinter Internship ReportSachin KumarNo ratings yet

- Spta. Annual PlanDocument2 pagesSpta. Annual PlanJonathan Siriban BiasNo ratings yet