You might also like

- Prest On Basics (F&O) - YashodhanDocument13 pagesPrest On Basics (F&O) - YashodhanAkshay SahooNo ratings yet

- Welcome To Stock Market Trading Sharing SessionDocument47 pagesWelcome To Stock Market Trading Sharing SessionOlegario S. Sumaya IIINo ratings yet

- Title of The Project Comes Here: A.M.I.EDocument5 pagesTitle of The Project Comes Here: A.M.I.EHimanshu JaniNo ratings yet

- Marketing Analytics: The Big Book ofDocument38 pagesMarketing Analytics: The Big Book ofEmmanuel OduroNo ratings yet

- The Robert Donato Approach to Enhancing Customer Service and Cultivating RelationshipsFrom EverandThe Robert Donato Approach to Enhancing Customer Service and Cultivating RelationshipsNo ratings yet

- Building Your Financial Future: A Practical Guide For Young AdultsFrom EverandBuilding Your Financial Future: A Practical Guide For Young AdultsNo ratings yet

- Investment Portfolio Management A Complete Guide - 2020 EditionFrom EverandInvestment Portfolio Management A Complete Guide - 2020 EditionNo ratings yet

- Facebook for Business - A Beginner's Guide to Growing Your FollowersFrom EverandFacebook for Business - A Beginner's Guide to Growing Your FollowersNo ratings yet

- The Forex Options Course: A Self-Study Guide to Trading Currency OptionsFrom EverandThe Forex Options Course: A Self-Study Guide to Trading Currency OptionsNo ratings yet

- Digital Marketing Trends and Prospects: Develop an effective Digital Marketing strategy with SEO, SEM, PPC, Digital Display Ads & Email Marketing techniques. (English Edition)From EverandDigital Marketing Trends and Prospects: Develop an effective Digital Marketing strategy with SEO, SEM, PPC, Digital Display Ads & Email Marketing techniques. (English Edition)No ratings yet

- Retail-Iation: Serious and Humorous Observations on Bad Shopping BehaviorFrom EverandRetail-Iation: Serious and Humorous Observations on Bad Shopping BehaviorNo ratings yet

- Growth Strategy Process Flow A Complete Guide - 2020 EditionFrom EverandGrowth Strategy Process Flow A Complete Guide - 2020 EditionNo ratings yet

- Ecommerce WebsiteDocument23 pagesEcommerce WebsiteShahnur AlamNo ratings yet

- Investigating The Property Pre-Exchange SearchesDocument40 pagesInvestigating The Property Pre-Exchange SearchesFh FhNo ratings yet

- DRM-5 Options BasicsDocument22 pagesDRM-5 Options BasicsqazxswNo ratings yet

- Lecture 1 - Into To TA Dow TheoryDocument29 pagesLecture 1 - Into To TA Dow TheoryAnonymous acRCvQDNo ratings yet

- Digital Marketing CourseDocument5 pagesDigital Marketing CourseAswin JayakumarNo ratings yet

- Options Basics Tutorial: Best Brokers For Options TradingDocument33 pagesOptions Basics Tutorial: Best Brokers For Options TradingasadrekarimiNo ratings yet

- OptionsDocument13 pagesOptionsashraf240881No ratings yet

- Options: The Upside Without The DownsideDocument32 pagesOptions: The Upside Without The DownsidebalamanichalaNo ratings yet

- English: App Subscription SpecialsDocument11 pagesEnglish: App Subscription Specialsanon_267862261No ratings yet

- Contract and Service Level AgreementDocument4 pagesContract and Service Level Agreementdavid ahiomeNo ratings yet

- Case Study of Buisness Tycoon (Mukesh Jagtiani) : BY Vanshika MathurDocument7 pagesCase Study of Buisness Tycoon (Mukesh Jagtiani) : BY Vanshika MathurVANSHIKA MATHURNo ratings yet

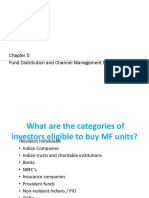

- Ch-5 Fund Distribution and Channel Management PracticesDocument10 pagesCh-5 Fund Distribution and Channel Management PracticesrishabhNo ratings yet

- Options Market: Introduction ToDocument40 pagesOptions Market: Introduction ToKurtNo ratings yet

- Risk Management and Derivatives - 2Document43 pagesRisk Management and Derivatives - 2mahesh8169No ratings yet

- Entrepreneurial Process: Here Are The 5 Critical Stages You Will Go Through As An EntrepreneurDocument30 pagesEntrepreneurial Process: Here Are The 5 Critical Stages You Will Go Through As An EntrepreneurDela Rosa ClairielleNo ratings yet

- Product Knowledge Guide 21-3Document10 pagesProduct Knowledge Guide 21-3Matheem AhmedNo ratings yet

- Final How To Start Trading With DTA PDFDocument43 pagesFinal How To Start Trading With DTA PDFNKNo ratings yet

- Money Management PlannerDocument4 pagesMoney Management PlannerlaxmiccNo ratings yet

- 1.1 Why Do I Want To Be A Trader?: 1. Self AssessmentDocument11 pages1.1 Why Do I Want To Be A Trader?: 1. Self AssessmentyhaodforNo ratings yet

- Develop and Use A Savings Plan MaterialDocument9 pagesDevelop and Use A Savings Plan MaterialDo DothingsNo ratings yet

- CRM Stands For Customer Relationship ManagementDocument8 pagesCRM Stands For Customer Relationship ManagementRavindra GoyalNo ratings yet

- OFS Trading System EnglishDocument33 pagesOFS Trading System EnglishkahfieNo ratings yet

- Guide Using The Marketing Plan TemplateDocument5 pagesGuide Using The Marketing Plan TemplateAbbad100% (1)

- Step by Step Manual: Preparing Yourself To The Path of Trading MasteryDocument7 pagesStep by Step Manual: Preparing Yourself To The Path of Trading Masteryshares_leoneNo ratings yet

- Business Sales PitchDocument2 pagesBusiness Sales PitchEmphorasoft gmailNo ratings yet

- MYKS!Document337 pagesMYKS!vagabond2010No ratings yet

- Compete With The Big Boys and Win! A David and Goliath StoryDocument12 pagesCompete With The Big Boys and Win! A David and Goliath StoryRed SnapperNo ratings yet

- Employee Handbook Template 04Document9 pagesEmployee Handbook Template 04petebakarNo ratings yet

- IMC Term Project QuestionnaireDocument5 pagesIMC Term Project QuestionnaireHamrah SiddiquiNo ratings yet

- 4.sales ForecastDocument28 pages4.sales ForecastSourav SinhaNo ratings yet

- Buying A Call Option - Varsity by ZerodhaDocument112 pagesBuying A Call Option - Varsity by ZerodhaSwapnil Jaiswal100% (1)

- Research About Pitching and Components of Business PlanDocument4 pagesResearch About Pitching and Components of Business PlanMyb CrisostomoNo ratings yet

- A To Z Web Hosting GuideDocument9 pagesA To Z Web Hosting Guidenorman daytoNo ratings yet

- Anatomy of An SMPDocument35 pagesAnatomy of An SMPScott KramerNo ratings yet

- Social Media ProposalDocument2 pagesSocial Media Proposal0307aliNo ratings yet

- Introduction To Linkedin: Resource GuideDocument25 pagesIntroduction To Linkedin: Resource GuideJoe BlowNo ratings yet

- Marketing TipsDocument6 pagesMarketing TipsParas ShahNo ratings yet

- Debt CollectionDocument12 pagesDebt CollectionTaranisaNo ratings yet

- What Is Evidence-Based Reading Instruction and How Do You Know It When You See ItDocument13 pagesWhat Is Evidence-Based Reading Instruction and How Do You Know It When You See ItTaranisaNo ratings yet

- Eat More Weigh LessDocument8 pagesEat More Weigh LessTaranisaNo ratings yet

- Literacy Begins at HomeDocument8 pagesLiteracy Begins at HomeTaranisaNo ratings yet

- Medicines by Design: U.S. Department of Health and Human ServicesDocument60 pagesMedicines by Design: U.S. Department of Health and Human ServicesChandru SNo ratings yet

- American Grand Strategy and The Future of U.S. LandpowerDocument500 pagesAmerican Grand Strategy and The Future of U.S. LandpowerTaranisa100% (1)

- Preserving Animal SkullsDocument4 pagesPreserving Animal SkullsTaranisaNo ratings yet

- Looking at My Genes, What Can They Tell MeDocument4 pagesLooking at My Genes, What Can They Tell MeTaranisaNo ratings yet

- A Chronology of Middle Missouri Plains Village SitesDocument346 pagesA Chronology of Middle Missouri Plains Village SitesTaranisaNo ratings yet

- Hallucinogens and Dissociative DrugsDocument8 pagesHallucinogens and Dissociative DrugsTaranisaNo ratings yet

- How To Grow PeppersDocument2 pagesHow To Grow PeppersTaranisa100% (1)

- Public Health CompediumDocument124 pagesPublic Health CompediumTaranisaNo ratings yet

- WinesDocument15 pagesWinesRose ann rodriguezNo ratings yet

- Neither This Nor That by Jean KleinDocument6 pagesNeither This Nor That by Jean KleinTarun Patwal60% (5)

- Biphasic Liquid Dosage FromDocument8 pagesBiphasic Liquid Dosage FromSwaroopSinghJakhar100% (1)

- Sf1 Cinderella JuneDocument60 pagesSf1 Cinderella JuneLaLa FullerNo ratings yet

- Initiatives For Field StaffDocument1 pageInitiatives For Field Staffkalpesh thakerNo ratings yet

- Important MCQ Colloction For PartDocument154 pagesImportant MCQ Colloction For PartNazia Ali86% (7)

- Chapter4 Cost AllocationDocument14 pagesChapter4 Cost AllocationNetsanet BelayNo ratings yet

- PENC N BONDIDocument5 pagesPENC N BONDIYLND100% (1)

- US8236919Document4 pagesUS8236919Billy FowlerNo ratings yet

- NCP RequirementsDocument3 pagesNCP RequirementsJasmine JarapNo ratings yet

- Ayurvedic and Naturopathic Way of Life by Manthena Sathyanarayana RajuDocument7 pagesAyurvedic and Naturopathic Way of Life by Manthena Sathyanarayana RajuvishnuprakashNo ratings yet

- People. Passion. Possibilities.: .30 .11 Thread Relief As RequiredDocument40 pagesPeople. Passion. Possibilities.: .30 .11 Thread Relief As RequiredFranciscoNo ratings yet

- Epsom Salt ClassDocument7 pagesEpsom Salt ClassSofia marisa fernandesNo ratings yet

- Lesson 30 PDFDocument5 pagesLesson 30 PDFLaura B.No ratings yet

- Labor Standards Course Outline 2019-2020Document7 pagesLabor Standards Course Outline 2019-2020Rommel BellonesNo ratings yet

- Notes On Substance AbuseDocument15 pagesNotes On Substance Abusesarguss14100% (1)

- 68BDocument5 pages68BJamie Schultz100% (1)

- Aircraft EnginesDocument20 pagesAircraft EnginesAlberto Martinez IgualadaNo ratings yet

- User Munual For DENAIR Diesel Portable Air CompressorDocument25 pagesUser Munual For DENAIR Diesel Portable Air CompressorBoumediene CHIKHAOUINo ratings yet

- Applicationformpdf COLUMBANDocument1 pageApplicationformpdf COLUMBANRIMANDO LAFUENTENo ratings yet

- Learning Intervention Program (Lip) Plan Second Quarter SY 2020 - 2021Document3 pagesLearning Intervention Program (Lip) Plan Second Quarter SY 2020 - 2021Laarni Kiamco Ortiz EpanNo ratings yet

- Horizontal and Vertical Dis AllowanceDocument12 pagesHorizontal and Vertical Dis Allowancesuhaspujari93No ratings yet

- Unit 11 - Late AdulthoodDocument14 pagesUnit 11 - Late AdulthoodEvet VaxbmNo ratings yet

- Latihan Soal Tentang Public PlacesDocument3 pagesLatihan Soal Tentang Public PlacesRiimha AmbarwatiNo ratings yet

- Central Banks Retail Forex DealersDocument7 pagesCentral Banks Retail Forex DealersBCom HonsNo ratings yet

- Operation - Manual Sondex A/S SFD 6: Customer: Newbuilding No: Order No.: Sondex Order No.: Encl.Document132 pagesOperation - Manual Sondex A/S SFD 6: Customer: Newbuilding No: Order No.: Sondex Order No.: Encl.AlexDor100% (1)

- TwoStep Linkage SSP9028 v10Document1 pageTwoStep Linkage SSP9028 v10David BriggsNo ratings yet

- The Neurovascular Bundle of The Anterior Compartment ofDocument30 pagesThe Neurovascular Bundle of The Anterior Compartment ofAnnapurna Bose100% (2)

- Transcritical Co2 Refrigeration - PDFDocument11 pagesTranscritical Co2 Refrigeration - PDFHector Fabian Hernandez Algarra100% (1)

- Fdocuments - in - List of Private Laboratories Empanelled by KSPCB As Per of Empanelment LabsDocument7 pagesFdocuments - in - List of Private Laboratories Empanelled by KSPCB As Per of Empanelment LabsKartik RajputNo ratings yet