You might also like

- Regional Trial Court Branch 51: Rtc2sor051@judiciary - Gov.phDocument4 pagesRegional Trial Court Branch 51: Rtc2sor051@judiciary - Gov.phMaricrisNo ratings yet

- Reviewer Labor RelDocument5 pagesReviewer Labor RelMaricrisNo ratings yet

- Donors TaxDocument6 pagesDonors TaxMaricrisNo ratings yet

- OCA Circular No. 209-2020Document31 pagesOCA Circular No. 209-2020MaricrisNo ratings yet

- OCA Circular No. 60-2021Document3 pagesOCA Circular No. 60-2021MaricrisNo ratings yet

- Special Power of AttorneyDocument1 pageSpecial Power of AttorneyMaricrisNo ratings yet

- Affidavit of Desistance: Regional Trial CourtDocument1 pageAffidavit of Desistance: Regional Trial CourtMaricrisNo ratings yet

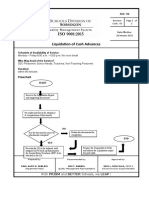

- ACC 02 PROCESS MANUAL Liquidation of Cash AdvancesDocument2 pagesACC 02 PROCESS MANUAL Liquidation of Cash AdvancesMaricrisNo ratings yet

- OCA Circular No. 51-2021Document2 pagesOCA Circular No. 51-2021MaricrisNo ratings yet

- ACC 03 PROCESS MANUAL Lddap Ada FacilityDocument2 pagesACC 03 PROCESS MANUAL Lddap Ada FacilityMaricrisNo ratings yet

- Labor Repair (Office Equipment) Labor Repair (Office Equipment)Document7 pagesLabor Repair (Office Equipment) Labor Repair (Office Equipment)MaricrisNo ratings yet

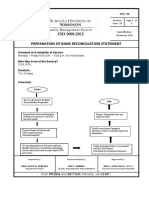

- ACC 06 PROCESS MANUAL Bank ReconDocument7 pagesACC 06 PROCESS MANUAL Bank ReconMaricrisNo ratings yet

- Republic of The Philippines: (Revised As of April 1992)Document1 pageRepublic of The Philippines: (Revised As of April 1992)MaricrisNo ratings yet

- Acc 01 Process Manual Mooe DownloadingDocument2 pagesAcc 01 Process Manual Mooe DownloadingMaricrisNo ratings yet

- Bir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of August, 2018Document10 pagesBir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of August, 2018MaricrisNo ratings yet

- Bir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of June, 2018Document5 pagesBir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of June, 2018MaricrisNo ratings yet

- Bir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of March, 2018Document10 pagesBir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of March, 2018MaricrisNo ratings yet

- Bir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of May, 2018Document5 pagesBir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of May, 2018MaricrisNo ratings yet

- Bulletin 05Document4 pagesBulletin 05Allan YdiaNo ratings yet

- Bir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of January, 2018Document5 pagesBir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of January, 2018MaricrisNo ratings yet

- Remedial Law (Civil Procedure) - San Beda 2011 PDFDocument123 pagesRemedial Law (Civil Procedure) - San Beda 2011 PDFRuby SantillanaNo ratings yet

- Handout No. 14Document22 pagesHandout No. 14MaricrisNo ratings yet

- Crim Law Reviewer 2Document82 pagesCrim Law Reviewer 2MaricrisNo ratings yet

- Willy and Sons Corporation - Sorsogon: Concepcion Carrier Product Specialist 09460098500/ 09277777854Document1 pageWilly and Sons Corporation - Sorsogon: Concepcion Carrier Product Specialist 09460098500/ 09277777854MaricrisNo ratings yet

- The Real Life Tara Mohr PDFDocument13 pagesThe Real Life Tara Mohr PDFMaricrisNo ratings yet

- 2017 Cashier's ReportDocument21 pages2017 Cashier's ReportMaricrisNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Types of Determinations in Sap SDDocument5 pagesTypes of Determinations in Sap SDMazharkhan ModiNo ratings yet

- Recent Advances in Cost Accounting and Cost SystemDocument6 pagesRecent Advances in Cost Accounting and Cost SystemDeepak ChandekarNo ratings yet

- Sumit Purohit Resume2 PDFDocument3 pagesSumit Purohit Resume2 PDFSUMIT S PUROHITNo ratings yet

- Chapter 07 SMDocument25 pagesChapter 07 SMTehniat HamzaNo ratings yet

- Final ReportDocument33 pagesFinal ReportMohammad azriNo ratings yet

- Business Studies Paper 5Document8 pagesBusiness Studies Paper 5SAMARPAN CHAKRABORTYNo ratings yet

- Pricing Wars: Signode Industries, IncDocument8 pagesPricing Wars: Signode Industries, IncraviNo ratings yet

- The Road Less Stupid - Keith J CunninghamDocument338 pagesThe Road Less Stupid - Keith J CunninghamChhunning Tiv100% (5)

- The Budgeting FrameworkDocument47 pagesThe Budgeting FrameworkRecruit guideNo ratings yet

- ProjectDocument36 pagesProjectVenkatesh Sastry VenkiNo ratings yet

- How To Transfer Land Title in The Philippines 2021Document8 pagesHow To Transfer Land Title in The Philippines 2021Eugene PicazoNo ratings yet

- Aggregate Sales and Operations PlanningDocument22 pagesAggregate Sales and Operations Planningreuniongroup gsc2020No ratings yet

- Deed of Conditional SaleDocument4 pagesDeed of Conditional SaleMJane PerezNo ratings yet

- Catalog PDFDocument222 pagesCatalog PDFLeandro100% (1)

- Jennonoverlinecrane 35286 Smoe - 12x30t Eotc 2x10ton GC Span 30m Hol 12mDocument6 pagesJennonoverlinecrane 35286 Smoe - 12x30t Eotc 2x10ton GC Span 30m Hol 12mjurieskNo ratings yet

- HLL: Reinventing Distribution: © 2010 IBS. All Rights ReservedDocument14 pagesHLL: Reinventing Distribution: © 2010 IBS. All Rights Reserved8055427395No ratings yet

- Test Bank - Law On SalesDocument14 pagesTest Bank - Law On SalesEdward NublaNo ratings yet

- Analyzing Food MarketsDocument45 pagesAnalyzing Food Marketsagricultural and biosystems engineeringNo ratings yet

- Power and Ideologies Behind Words and Images: A Semiotic Analysis of Olay Facebook 2016 AdvertisementsDocument33 pagesPower and Ideologies Behind Words and Images: A Semiotic Analysis of Olay Facebook 2016 AdvertisementsHannah PeralesNo ratings yet

- Rahul-Individual Essay - Copy 1Document7 pagesRahul-Individual Essay - Copy 1Rahul SinghNo ratings yet

- (I) Introduction To Marketing & Consumer Perception (Ii) Introduction To Retailer PerceptionDocument5 pages(I) Introduction To Marketing & Consumer Perception (Ii) Introduction To Retailer PerceptionAnil Kumar SinghNo ratings yet

- Sales Process: Customers and Customer Groups: SAP Business One Version 9.3Document16 pagesSales Process: Customers and Customer Groups: SAP Business One Version 9.3Abrans GarciaNo ratings yet

- Enterprise Analysis ReportDocument16 pagesEnterprise Analysis ReportGurmeetNo ratings yet

- Report On Marketing AuditDocument12 pagesReport On Marketing Auditm_dhrutiNo ratings yet

- Autodesk - Intrepid Case StudyDocument7 pagesAutodesk - Intrepid Case Studyvivekb67No ratings yet

- "From Startup To Scalable Enterprise Laying The Foundation" PDFDocument9 pages"From Startup To Scalable Enterprise Laying The Foundation" PDFshizzyNo ratings yet

- Imran Hossain: Career ObjectiveDocument3 pagesImran Hossain: Career ObjectiveYaseen Fida HossainNo ratings yet

- CXM Framework - OriginalDocument32 pagesCXM Framework - Originalamar_nokiatejNo ratings yet

- Youth Mentoring Program Business PlanDocument51 pagesYouth Mentoring Program Business PlanJoseph QuillNo ratings yet

- Platform Fee: United States & Puerto RicoDocument12 pagesPlatform Fee: United States & Puerto RicoLiang ChenNo ratings yet