You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- I. Liquidity Ratios: Current Assets/current LiablitiesDocument14 pagesI. Liquidity Ratios: Current Assets/current LiablitiesdevinhyNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Oracle Forms and Report Builder 6iDocument168 pagesOracle Forms and Report Builder 6iSyed Abdul Khaliq BariNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Using Client-Side Dynamic SQL: The EXEC - SQL PackageDocument31 pagesUsing Client-Side Dynamic SQL: The EXEC - SQL PackagedevinhyNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- MafaDocument54 pagesMafaShrinidhi TssNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Analysis of Financial Statements: Stice - Stice - SkousenDocument52 pagesAnalysis of Financial Statements: Stice - Stice - SkousenmeshNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Functions of Central BankDocument7 pagesFunctions of Central BankJohn RobertsonNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Account ClassificationDocument3 pagesAccount ClassificationUsama MukhtarNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- APF 55 Oct15 SinglesDocument100 pagesAPF 55 Oct15 SinglesAmir ZarehNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- A Study On Investors Perception Towards Sharemarket in Sharekhan LTDDocument10 pagesA Study On Investors Perception Towards Sharemarket in Sharekhan LTDSANAULLAH SULTANPURNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- MS-4 Dec 2012 PDFDocument4 pagesMS-4 Dec 2012 PDFAnonymous Uqrw8OwFWuNo ratings yet

- Applied Auditing 2Document11 pagesApplied Auditing 2Leny Joy DupoNo ratings yet

- Selfridges - Company CapsuleDocument14 pagesSelfridges - Company Capsulekidszalor1412No ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Swedish Match Case SolutionDocument5 pagesSwedish Match Case SolutionKaran AggarwalNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Azizi Completes 479-Unit Aura in Downtown Jebel Ali - Projects and Tende...Document20 pagesAzizi Completes 479-Unit Aura in Downtown Jebel Ali - Projects and Tende...Sanabel EliasNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Etm 2011 4 30 1Document1 pageEtm 2011 4 30 1pahwacNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- JWCh07 PDFDocument29 pagesJWCh07 PDF007featherNo ratings yet

- Industrialisation by InvitationDocument10 pagesIndustrialisation by InvitationLashaniaNo ratings yet

- PDFDocument124 pagesPDFadsfNo ratings yet

- Understanding Bonds and DebenturesDocument16 pagesUnderstanding Bonds and Debenturesbishal bothraNo ratings yet

- The Economic Times - Business News, Personal Finance, Financial News, India Stock Market Investing, Economy News, SENSEX, NIFTY, NSE, BSE Live, IPO News PDFDocument5 pagesThe Economic Times - Business News, Personal Finance, Financial News, India Stock Market Investing, Economy News, SENSEX, NIFTY, NSE, BSE Live, IPO News PDFKaushik BalachandarNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- HST Solar-Slide DeckDocument5 pagesHST Solar-Slide DeckSaad YoussefiNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Cancelled NBFCDocument336 pagesCancelled NBFCAANo ratings yet

- Economic Growth in Nehru EraDocument15 pagesEconomic Growth in Nehru Erakoushikonomics4002100% (9)

- Real Estate Agent Company ProfileDocument14 pagesReal Estate Agent Company ProfileAkash Ranjan100% (1)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Nepal COSDocument45 pagesNepal COSLeo KhkNo ratings yet

- Conceptual Framework Lecture Notes: The Framework at A GlanceDocument11 pagesConceptual Framework Lecture Notes: The Framework at A Glancenicole bancoro100% (1)

- Events Prevented Calculator OverviewDocument5 pagesEvents Prevented Calculator OverviewAlvaro MuñozNo ratings yet

- Stand ChartDocument804 pagesStand Chartnagaraj100No ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- OFTC Lesson 18 - Integrating Order Flow With Traditional Technical AnalysisDocument34 pagesOFTC Lesson 18 - Integrating Order Flow With Traditional Technical AnalysisThanhdat VoNo ratings yet

- Strategic Management: Jpmorgan Chase & CoDocument16 pagesStrategic Management: Jpmorgan Chase & CoBea Garcia100% (1)

- A Study On HDFC Mutual FundDocument88 pagesA Study On HDFC Mutual FundSagar Paul'gNo ratings yet

- Govt. InterventionDocument20 pagesGovt. InterventionRadhika IyerNo ratings yet

- Durgesh Singh Charts PDFDocument11 pagesDurgesh Singh Charts PDFHimanshu Jeerawala75% (4)

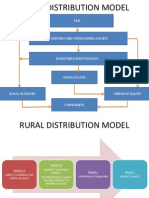

- Hul Distribution ModelDocument5 pagesHul Distribution ModelBhavik LodhaNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)