You might also like

- qUANTECHEXCEL SOLVERDocument3 pagesqUANTECHEXCEL SOLVERKristine Tiu100% (1)

- A Partnership With A Capital Less Than 3000 Is Void If It Is Unregistered With SECDocument4 pagesA Partnership With A Capital Less Than 3000 Is Void If It Is Unregistered With SECElla Mae TuratoNo ratings yet

- Business Cup Level 1 Quiz BeeDocument28 pagesBusiness Cup Level 1 Quiz BeeRowellPaneloSalapareNo ratings yet

- Review TestDocument1 pageReview TestKristine Joy Mendoza InciongNo ratings yet

- Exercise Workbook: Smartbooks BasicDocument21 pagesExercise Workbook: Smartbooks BasicAngelica TuazonNo ratings yet

- Chapter 6 - Income Tax For PartnershipDocument40 pagesChapter 6 - Income Tax For PartnershipNineteen Aùgùst100% (1)

- This Study Resource Was: I. DefinitionsDocument5 pagesThis Study Resource Was: I. DefinitionsCresenciano MalabuyocNo ratings yet

- Horizontal Analysis Interpretation PDFDocument2 pagesHorizontal Analysis Interpretation PDFAlison JcNo ratings yet

- ACEFIAR Quiz No. 7Document2 pagesACEFIAR Quiz No. 7Marriel Fate CullanoNo ratings yet

- Chapter 6 - Retained EarningsDocument30 pagesChapter 6 - Retained Earningslou-924No ratings yet

- CF Qualitative CharacteristicsDocument3 pagesCF Qualitative Characteristicspanda 1No ratings yet

- Accounting 101 - Reviewer (TEST QUIZ)Document18 pagesAccounting 101 - Reviewer (TEST QUIZ)AuroraNo ratings yet

- Definition of Terms: GROSS INCOME: Classification of Taxpayers, Compensation Income, and Business IncomeDocument13 pagesDefinition of Terms: GROSS INCOME: Classification of Taxpayers, Compensation Income, and Business IncomeSKEETER BRITNEY COSTANo ratings yet

- Far Prelims Week 1Document3 pagesFar Prelims Week 1hat dawgNo ratings yet

- rev-mat-2-IA Print PDFDocument31 pagesrev-mat-2-IA Print PDFAyaka FujiharaNo ratings yet

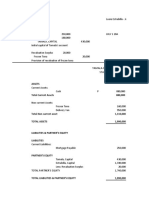

- Assets: Tamala & Estrabilla Tuna Fish Buy and Sell Statement of Financial Position As of July 1, 20ADocument2 pagesAssets: Tamala & Estrabilla Tuna Fish Buy and Sell Statement of Financial Position As of July 1, 20AAdam CuencaNo ratings yet

- Final AssignmentDocument10 pagesFinal AssignmentRuthNo ratings yet

- Krystal Guile Dagatan - Activity 2Document6 pagesKrystal Guile Dagatan - Activity 2Krystal Guile DagatanNo ratings yet

- 04 TP FinancialDocument4 pages04 TP Financialbless erika lendroNo ratings yet

- Standard Costing: Answer Key On Chapter 7Document5 pagesStandard Costing: Answer Key On Chapter 7Jaquelyn JacquesNo ratings yet

- AccountingDocument10 pagesAccountingCacjungoyNo ratings yet

- TXNT-Chapter 8 To 15Document51 pagesTXNT-Chapter 8 To 15Joylyn IgloriaNo ratings yet

- Chapter 6: Self-Test Taxation Discussion QuestionsDocument9 pagesChapter 6: Self-Test Taxation Discussion QuestionsUnnamed homosapienNo ratings yet

- Midterm Exam On Income Tax - QuestionsDocument11 pagesMidterm Exam On Income Tax - QuestionskeziahNo ratings yet

- Microeconomics Spoken PoetryDocument2 pagesMicroeconomics Spoken PoetryChris AnnNo ratings yet

- Evaluating Firm Performance - ReportDocument5 pagesEvaluating Firm Performance - ReportJeane Mae BooNo ratings yet

- Gray Electronic Repair ServicesDocument1 pageGray Electronic Repair ServicesFarman AfzalNo ratings yet

- Maris CorporationDocument2 pagesMaris CorporationmageNo ratings yet

- Orca Share Media1540033147945Document17 pagesOrca Share Media1540033147945Melady Sison CequeñaNo ratings yet

- Activity 2 ECODocument2 pagesActivity 2 ECOEugene AlipioNo ratings yet

- Assignment 1 Caro Coleen Sec27Document2 pagesAssignment 1 Caro Coleen Sec27Alyssa TordesillasNo ratings yet

- Law and Joint Obligations ModifiedDocument34 pagesLaw and Joint Obligations ModifiedAllanah AncotNo ratings yet

- Batangas State University: College of Accountancy, Business, Economics and International Hospitality ManagementDocument1 pageBatangas State University: College of Accountancy, Business, Economics and International Hospitality ManagementLedayl MaralitNo ratings yet

- Amended Bsa Handout For Gross Income Part 1Document40 pagesAmended Bsa Handout For Gross Income Part 1Dianne Lontac100% (1)

- 1 - Exercises On Relevant Cost 1Document7 pages1 - Exercises On Relevant Cost 1Temesgen AbezaNo ratings yet

- Regulation of Financial SystemDocument39 pagesRegulation of Financial SystemRamil ElambayoNo ratings yet

- A Feasiblity StudyDocument7 pagesA Feasiblity StudyLeigh Crisse Manaois100% (2)

- Assignment 3Document6 pagesAssignment 3Triechia LaudNo ratings yet

- Module 5 Co Ownership Estates and TrustsDocument10 pagesModule 5 Co Ownership Estates and TrustsChryshelle Anne Marie LontokNo ratings yet

- Lupisan-Baysa PDFDocument206 pagesLupisan-Baysa PDFRicart Von LauretaNo ratings yet

- MULTIPLE CHOICE: Choose The Best AnswerDocument3 pagesMULTIPLE CHOICE: Choose The Best AnswerEppie SeverinoNo ratings yet

- Repealed PD 692 Known As Revised Accountancy LawDocument8 pagesRepealed PD 692 Known As Revised Accountancy LawLian RamirezNo ratings yet

- ABS-CBN Corporation: Philippine Stock Exchange, IncDocument1 pageABS-CBN Corporation: Philippine Stock Exchange, IncRomy JulieNo ratings yet

- FAR2 CHAPTER 1 (PG 1-13)Document13 pagesFAR2 CHAPTER 1 (PG 1-13)Layla MainNo ratings yet

- 3rd ActivityDocument2 pages3rd Activitydar •No ratings yet

- Determination of Income Tax Due and Payable If There Is A Given Creditable Withholding TaxDocument12 pagesDetermination of Income Tax Due and Payable If There Is A Given Creditable Withholding Taxgellie mare flores100% (1)

- Chapter 10Document4 pagesChapter 10Judith Salome Basquinas0% (1)

- Tax ComputationsDocument22 pagesTax ComputationsArmy KamiNo ratings yet

- Eoq PDFDocument23 pagesEoq PDFMica Ella Gutierrez0% (1)

- 03 Performance Task 1TAXATIONDocument5 pages03 Performance Task 1TAXATIONRianna CclNo ratings yet

- Chapter 4 EXERCISES - Estates and TrustsDocument9 pagesChapter 4 EXERCISES - Estates and TrustscathyydumpNo ratings yet

- Tax 321 Prelim Quiz 1 Key PDFDocument13 pagesTax 321 Prelim Quiz 1 Key PDFJeda UsonNo ratings yet

- Problem 7Document5 pagesProblem 7businessdoctor23No ratings yet

- Final Exam Taxation 101Document8 pagesFinal Exam Taxation 101Live LoveNo ratings yet

- Fundamentals of Basic Accounting AlilingDocument11 pagesFundamentals of Basic Accounting AlilingEmil Enriquez100% (1)

- 11 Tax Exempt de Minimis Benefits To EmployeesDocument2 pages11 Tax Exempt de Minimis Benefits To EmployeesAdrian Mark GomezNo ratings yet

- De Minimis BenefitsDocument1 pageDe Minimis BenefitsEduard RiparipNo ratings yet

- De Minimis Benefits 2024Document1 pageDe Minimis Benefits 2024Love Heart BantilesNo ratings yet

- De Minimis BenefitsDocument2 pagesDe Minimis BenefitsClaudine SumalinogNo ratings yet

- Bacterial Blight (BB) : Local NameDocument2 pagesBacterial Blight (BB) : Local NameanneNo ratings yet

- Weed Management: How To Manage Weedy RiceDocument2 pagesWeed Management: How To Manage Weedy RiceanneNo ratings yet

- Memo Circular Nos 8 A 9 A and 14 - Guidelines SIDA Scholarship Programs 1 PDFDocument14 pagesMemo Circular Nos 8 A 9 A and 14 - Guidelines SIDA Scholarship Programs 1 PDFanneNo ratings yet

- Beneficial Organisms 1Document2 pagesBeneficial Organisms 1anneNo ratings yet

- CRA Profile PhilippinesDocument24 pagesCRA Profile PhilippinesanneNo ratings yet

- Cfvr-Concepcion Kaibel 102221 Lot 3Document32 pagesCfvr-Concepcion Kaibel 102221 Lot 3anneNo ratings yet

- Sample Board ResolutionDocument2 pagesSample Board ResolutionRuel Apostol II90% (98)

- Inclusionexclusiondisqualification of ArbDocument16 pagesInclusionexclusiondisqualification of ArbanneNo ratings yet

- History and Evolution of Major Agrarian Reform LawsDocument14 pagesHistory and Evolution of Major Agrarian Reform LawsanneNo ratings yet

- 1991 AO12 Rules and Procedures To Govern The Acquisition and Distribution of Homelots Under The CARPDocument2 pages1991 AO12 Rules and Procedures To Govern The Acquisition and Distribution of Homelots Under The CARPanneNo ratings yet

- Republic Act No 34Document4 pagesRepublic Act No 34anneNo ratings yet

- Section 4. Grounds. - The Following Are The Grounds For The Cancellation of Eps, CloasDocument5 pagesSection 4. Grounds. - The Following Are The Grounds For The Cancellation of Eps, CloasanneNo ratings yet

- Affidavit of Aggregate Landholding VendorDocument1 pageAffidavit of Aggregate Landholding VendoranneNo ratings yet

- Inclusionxclusiondisqualification of ArbsDocument14 pagesInclusionxclusiondisqualification of ArbsanneNo ratings yet

- INDEX of AGRARIAN Related Doj OpinionsDocument15 pagesINDEX of AGRARIAN Related Doj OpinionsanneNo ratings yet

- Index of The Vital Documents On Agrarian ReformDocument47 pagesIndex of The Vital Documents On Agrarian ReformanneNo ratings yet

- Answer With Counterclaim - Final For PrintingDocument11 pagesAnswer With Counterclaim - Final For PrintingPatrick PenachosNo ratings yet

- Department of Labor: Ncentral07Document70 pagesDepartment of Labor: Ncentral07USA_DepartmentOfLaborNo ratings yet

- Letter To OPM - Hiring Freeze Impact On U.S. Forest ServiceDocument2 pagesLetter To OPM - Hiring Freeze Impact On U.S. Forest ServiceRepSinemaNo ratings yet

- Chapter - V Findings and SuggestionsDocument18 pagesChapter - V Findings and SuggestionsAnbarasan SivarajanNo ratings yet

- English 10 Module q1 Week 5 6Document17 pagesEnglish 10 Module q1 Week 5 6Angelica Javillonar AngcoyNo ratings yet

- Labour LawDocument17 pagesLabour LawHESHVIENIE A P VIJAYARATNAMNo ratings yet

- OHS Consultation Procedure SampleDocument7 pagesOHS Consultation Procedure SampleJeffrey RafaelNo ratings yet

- TA Rules Annex IDocument1 pageTA Rules Annex IGowsigan AdhimoolamNo ratings yet

- McDonalds Human Resource Management Case StudyDocument11 pagesMcDonalds Human Resource Management Case StudyDinuja Kaveesha HettigeNo ratings yet

- Death Benefits Under EPF & MP Act. Duties and Liabilities of EmployersDocument50 pagesDeath Benefits Under EPF & MP Act. Duties and Liabilities of EmployersJc Duke M Eliyasar100% (1)

- TimeSheet-Calculator TrumpExcelRevised-2017 v1Document7 pagesTimeSheet-Calculator TrumpExcelRevised-2017 v1ianachieviciNo ratings yet

- Huhtamaki Employment ApplicationDocument4 pagesHuhtamaki Employment ApplicationLeah BautistaNo ratings yet

- 48 Duncan Assn. of Detailman Vs Glaxo Wellcome Phils G.R. No. 162994Document5 pages48 Duncan Assn. of Detailman Vs Glaxo Wellcome Phils G.R. No. 162994SDN HelplineNo ratings yet

- IHR PlanningDocument17 pagesIHR PlanningSphoorthi Iruvanti100% (1)

- Approval Rule Setup Joblevel Based On Invoice ValueDocument5 pagesApproval Rule Setup Joblevel Based On Invoice ValueMihai FildanNo ratings yet

- Bhushan Dipak Bhalerao: QUESS Corp LTDDocument9 pagesBhushan Dipak Bhalerao: QUESS Corp LTDBhushan BhaleraoNo ratings yet

- Strat 15finalDocument153 pagesStrat 15finalKowshik ChakrabortyNo ratings yet

- Edu 2015 10 MLC ExamDocument58 pagesEdu 2015 10 MLC ExamAyeshaAttiyaAliNo ratings yet

- Macroeconomics and AIDS (Trevor Neilson, Brian Brink)Document17 pagesMacroeconomics and AIDS (Trevor Neilson, Brian Brink)National Press FoundationNo ratings yet

- One Minute ManagerDocument13 pagesOne Minute Managerapi-3825047100% (1)

- MidLife CrisisDocument54 pagesMidLife CrisisIndian Railways Knowledge Portal100% (3)

- SIP FINAL Report Shivani SaumyaDocument43 pagesSIP FINAL Report Shivani SaumyaMonika SharmaNo ratings yet

- Carthage Central School District Board of Education Sept. 14, 2020, AgendaDocument2 pagesCarthage Central School District Board of Education Sept. 14, 2020, AgendaNewzjunkyNo ratings yet

- A Study On Employee Retention in BPO INdustry in KeralaDocument7 pagesA Study On Employee Retention in BPO INdustry in KeralaKristine BaldovizoNo ratings yet

- 2020.01.27 ICS Social Complete Handbook For Factories V2Document46 pages2020.01.27 ICS Social Complete Handbook For Factories V2Jucy NguyenNo ratings yet

- Non Traditional Investment ApproachesDocument7 pagesNon Traditional Investment ApproachesKriti Gupta100% (1)

- Investigation On How Motivation Impacts On Staff Turnover A Case Study On NDB Bank SrilankaDocument77 pagesInvestigation On How Motivation Impacts On Staff Turnover A Case Study On NDB Bank SrilankaMvK ThenuNo ratings yet

- Industrial DisputesDocument12 pagesIndustrial Disputeskajal0% (1)

- Leave PolicyDocument2 pagesLeave PolicyShivangi PandeyNo ratings yet

- Conference ProgramDocument47 pagesConference Programa_l_y_n100% (1)

- How to get US Bank Account for Non US ResidentFrom EverandHow to get US Bank Account for Non US ResidentRating: 5 out of 5 stars5/5 (1)

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProFrom EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProRating: 4.5 out of 5 stars4.5/5 (43)

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- Tax Savvy for Small Business: A Complete Tax Strategy GuideFrom EverandTax Savvy for Small Business: A Complete Tax Strategy GuideRating: 5 out of 5 stars5/5 (1)

- Tax-Free Wealth For Life: How to Permanently Lower Your Taxes And Build More WealthFrom EverandTax-Free Wealth For Life: How to Permanently Lower Your Taxes And Build More WealthNo ratings yet

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyFrom EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyRating: 4 out of 5 stars4/5 (52)

- Taxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCFrom EverandTaxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCRating: 4 out of 5 stars4/5 (5)

- Bookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessFrom EverandBookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessRating: 5 out of 5 stars5/5 (5)

- Small Business: A Complete Guide to Accounting Principles, Bookkeeping Principles and Taxes for Small BusinessFrom EverandSmall Business: A Complete Guide to Accounting Principles, Bookkeeping Principles and Taxes for Small BusinessNo ratings yet

- Founding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationFrom EverandFounding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationNo ratings yet

- Make Sure It's Deductible: Little-Known Tax Tips for Your Canadian Small Business, Fifth EditionFrom EverandMake Sure It's Deductible: Little-Known Tax Tips for Your Canadian Small Business, Fifth EditionNo ratings yet

- The Tax and Legal Playbook: Game-Changing Solutions To Your Small Business QuestionsFrom EverandThe Tax and Legal Playbook: Game-Changing Solutions To Your Small Business QuestionsRating: 3.5 out of 5 stars3.5/5 (9)

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingFrom EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingRating: 5 out of 5 stars5/5 (3)

- Official Guide to Financial Accounting using TallyPrime: Managing your Business Just Got SimplerFrom EverandOfficial Guide to Financial Accounting using TallyPrime: Managing your Business Just Got SimplerNo ratings yet

- The Payroll Book: A Guide for Small Businesses and StartupsFrom EverandThe Payroll Book: A Guide for Small Businesses and StartupsRating: 5 out of 5 stars5/5 (1)

- Taxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipFrom EverandTaxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipNo ratings yet

- S Corporation ESOP Traps for the UnwaryFrom EverandS Corporation ESOP Traps for the UnwaryNo ratings yet

- The Taxes, Accounting, Bookkeeping Bible: [3 in 1] The Most Complete and Updated Guide for the Small Business Owner with Tips and Loopholes to Save Money and Avoid IRS PenaltiesFrom EverandThe Taxes, Accounting, Bookkeeping Bible: [3 in 1] The Most Complete and Updated Guide for the Small Business Owner with Tips and Loopholes to Save Money and Avoid IRS PenaltiesNo ratings yet