You might also like

- Acct1511 Final VersionDocument29 pagesAcct1511 Final VersioncarolinetsangNo ratings yet

- Acct1511 Final VersionDocument27 pagesAcct1511 Final VersioncarolinetsangNo ratings yet

- Final Exam f02Document13 pagesFinal Exam f02Omar Ahmed ElkhalilNo ratings yet

- Financial Management: Thursday 9 June 2011Document9 pagesFinancial Management: Thursday 9 June 2011catcat1122No ratings yet

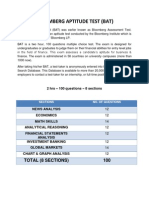

- Bloomberg Aptitude Test (BAT)Document10 pagesBloomberg Aptitude Test (BAT)Shivgan Joshi100% (1)

- Basic Financial Statements Analysis DoneDocument17 pagesBasic Financial Statements Analysis DoneAjmal SalamNo ratings yet

- Assignment May2011 ADocument6 pagesAssignment May2011 AZyn Wann HoNo ratings yet

- Question 1 (40marks - 48 Minutes)Document8 pagesQuestion 1 (40marks - 48 Minutes)dianimNo ratings yet

- Lesson 1Document8 pagesLesson 1Amangeldi SalimzhanovNo ratings yet

- IF1 - Practice ProblemsDocument198 pagesIF1 - Practice ProblemssaikrishnavnNo ratings yet

- Level 1 - Financial StatementDocument11 pagesLevel 1 - Financial StatementVimmi BanuNo ratings yet

- 2011 End of Session ExaminationDocument7 pages2011 End of Session Examinationleolau2015No ratings yet

- Cat/fia (FFM)Document9 pagesCat/fia (FFM)theizzatirosli100% (1)

- Test Bank For Financial Statement Analysis and Valuation 2nd Edition EastonDocument29 pagesTest Bank For Financial Statement Analysis and Valuation 2nd Edition Eastonagnesgrainneo30No ratings yet

- Using Bloomberg To Get The Data You NeedDocument36 pagesUsing Bloomberg To Get The Data You Needte_gantengNo ratings yet

- Comm 217 ProjectDocument3 pagesComm 217 Projectthemichaelmccarthy12No ratings yet

- CH 3 - The Statement of Financial Position and Financial DisclosuresDocument37 pagesCH 3 - The Statement of Financial Position and Financial DisclosuresZulqarnain KhokharNo ratings yet

- Acct1511 Final VersionDocument33 pagesAcct1511 Final VersioncarolinetsangNo ratings yet

- Comprehensive ExamDocument37 pagesComprehensive ExamAngeline DionicioNo ratings yet

- Acp5efm13 J CombinedDocument36 pagesAcp5efm13 J CombinedHan HowNo ratings yet

- Model Paper Financial AccountingDocument6 pagesModel Paper Financial AccountingzurwahmirzaNo ratings yet

- Financial AccountingDocument66 pagesFinancial AccountingFaisal SaleemNo ratings yet

- Test Bank For Financial Statement Analysis and Valuation 5th Edition by Easton Mcanally Sommers ZhangDocument30 pagesTest Bank For Financial Statement Analysis and Valuation 5th Edition by Easton Mcanally Sommers Zhangagnesgrainneo30100% (1)

- Test Bank For Financial Statement Analysis and Valuation 5th Edition by Easton Mcanally Sommers ZhangDocument30 pagesTest Bank For Financial Statement Analysis and Valuation 5th Edition by Easton Mcanally Sommers ZhangLucille Alexander100% (37)

- ACCT 201 Exam 1Document16 pagesACCT 201 Exam 1Steve ZaluchaNo ratings yet

- The Home DepotDocument14 pagesThe Home DepotDaniel NastaseNo ratings yet

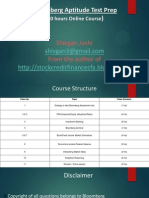

- Bloomberg Aptitude TestDocument35 pagesBloomberg Aptitude TestShivgan Joshi100% (1)

- Report Banking RiabkovDocument6 pagesReport Banking RiabkovKostia RiabkovNo ratings yet

- Impairment 10tipsDocument13 pagesImpairment 10tipsTindo MoyoNo ratings yet

- Financial Managemnet 3B LAO 2020 FinalDocument11 pagesFinancial Managemnet 3B LAO 2020 Finalsabelo.j.nkosi.5No ratings yet

- Georgetown Case Competition: ConfidentialDocument17 pagesGeorgetown Case Competition: ConfidentialPatrick BensonNo ratings yet

- ACCT504 Case Study 1Document15 pagesACCT504 Case Study 1sinbad97100% (1)

- WSJ Jpmfiling0510Document191 pagesWSJ Jpmfiling0510Reza Abusaidi100% (1)

- FR MJ23 Examiner's Report - FINALDocument24 pagesFR MJ23 Examiner's Report - FINALdeepshikhagupta514No ratings yet

- Fin 621 Final Term Papers 99 25 Sure Solved 2Document78 pagesFin 621 Final Term Papers 99 25 Sure Solved 2Javaid IqbalNo ratings yet

- Accounting 201 FALL 2000 Exam 2Document11 pagesAccounting 201 FALL 2000 Exam 2Corey ArmstrongNo ratings yet

- Chapter 3Document17 pagesChapter 3Phan Anh HaoNo ratings yet

- Capital Markets & Investments - BGK Chapter 1Document46 pagesCapital Markets & Investments - BGK Chapter 1张泷颢No ratings yet

- Examiner's Report: F3/FFA Financial Accounting June 2012Document4 pagesExaminer's Report: F3/FFA Financial Accounting June 2012Ahmad Hafid HanifahNo ratings yet

- M8 PracticeDocument22 pagesM8 PracticeleeminleeNo ratings yet

- Ba 623 Case AnalysisDocument8 pagesBa 623 Case AnalysisSarah Jane OrillosaNo ratings yet

- F551 A01Document11 pagesF551 A01Osman AnwarNo ratings yet

- Acct 504 Week 8 Final Exam All 4 Sets - DevryDocument17 pagesAcct 504 Week 8 Final Exam All 4 Sets - Devrycoursehomework0% (1)

- Acct1511 2013s2c2 Handout 2 PDFDocument19 pagesAcct1511 2013s2c2 Handout 2 PDFcelopurpleNo ratings yet

- Loan-Loss Provisions of Commercial Banks and Adequate Disclosure: A NoteDocument7 pagesLoan-Loss Provisions of Commercial Banks and Adequate Disclosure: A NoteabhinavatripathiNo ratings yet

- Acct3708 Finals, Sem 2, 2010Document11 pagesAcct3708 Finals, Sem 2, 2010nessawhoNo ratings yet

- Chapter 17Document48 pagesChapter 17Shiv NarayanNo ratings yet

- Intermediate Accounting Kieso 13e Comp. TestDocument13 pagesIntermediate Accounting Kieso 13e Comp. TestRJKcNo ratings yet

- Multiple Choice Questions: Section-IDocument6 pagesMultiple Choice Questions: Section-Isah108_pk796No ratings yet

- Multiple Choice Questions: Section-IDocument6 pagesMultiple Choice Questions: Section-ItysonhishamNo ratings yet

- Module 6 Ratio Analysis and InterpretationDocument9 pagesModule 6 Ratio Analysis and InterpretationHeart MacedaNo ratings yet

- f9 2014 Dec QDocument13 pagesf9 2014 Dec QreadtometooNo ratings yet

- Accounting Ratio PDFDocument10 pagesAccounting Ratio PDFMuhammad KaleemNo ratings yet

- Handbook of Basel III Capital: Enhancing Bank Capital in PracticeFrom EverandHandbook of Basel III Capital: Enhancing Bank Capital in PracticeNo ratings yet

- The Essentials of Finance and Accounting for Nonfinancial ManagersFrom EverandThe Essentials of Finance and Accounting for Nonfinancial ManagersRating: 5 out of 5 stars5/5 (1)

- Consumer Lending Revenues World Summary: Market Values & Financials by CountryFrom EverandConsumer Lending Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Miscellaneous Nondepository Credit Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Nondepository Credit Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Cost of Doing Business Study, 2012 EditionFrom EverandCost of Doing Business Study, 2012 EditionNo ratings yet

- Secondary Market Financing Revenues World Summary: Market Values & Financials by CountryFrom EverandSecondary Market Financing Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Measuring Business Interruption Losses and Other Commercial Damages: An Economic ApproachFrom EverandMeasuring Business Interruption Losses and Other Commercial Damages: An Economic ApproachNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.27Document1 pageWeek 9 Portfolio Performance Evaluation - Color.27jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.28Document1 pageWeek 9 Portfolio Performance Evaluation - Color.28jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.29Document1 pageWeek 9 Portfolio Performance Evaluation - Color.29jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.21Document1 pageWeek 9 Portfolio Performance Evaluation - Color.21jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.22Document1 pageWeek 9 Portfolio Performance Evaluation - Color.22jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.25Document1 pageWeek 9 Portfolio Performance Evaluation - Color.25jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.26Document1 pageWeek 9 Portfolio Performance Evaluation - Color.26jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.16Document1 pageWeek 9 Portfolio Performance Evaluation - Color.16jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.24Document1 pageWeek 9 Portfolio Performance Evaluation - Color.24jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.17Document1 pageWeek 9 Portfolio Performance Evaluation - Color.17jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.14Document1 pageWeek 9 Portfolio Performance Evaluation - Color.14jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.19Document1 pageWeek 9 Portfolio Performance Evaluation - Color.19jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.20Document1 pageWeek 9 Portfolio Performance Evaluation - Color.20jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.15Document1 pageWeek 9 Portfolio Performance Evaluation - Color.15jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.5Document1 pageWeek 9 Portfolio Performance Evaluation - Color.5jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.8Document1 pageWeek 9 Portfolio Performance Evaluation - Color.8jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.6Document1 pageWeek 9 Portfolio Performance Evaluation - Color.6jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.13Document1 pageWeek 9 Portfolio Performance Evaluation - Color.13jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.3Document1 pageWeek 9 Portfolio Performance Evaluation - Color.3jonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.11Document1 pageWeek 9 Portfolio Performance Evaluation - Color.11jonNo ratings yet

- Online Quiz 7 SIM Q&ADocument4 pagesOnline Quiz 7 SIM Q&AjonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.4Document1 pageWeek 9 Portfolio Performance Evaluation - Color.4jonNo ratings yet

- Online Quiz 3 Duration Q&ADocument3 pagesOnline Quiz 3 Duration Q&AjonNo ratings yet

- The Term Structure of Interest RatesDocument37 pagesThe Term Structure of Interest RatesjonNo ratings yet

- Week 9 Portfolio Performance Evaluation - Color.2Document1 pageWeek 9 Portfolio Performance Evaluation - Color.2jonNo ratings yet

- Sraj (Q4 - 2015)Document108 pagesSraj (Q4 - 2015)Wihelmina DeaNo ratings yet

- Adms 2510 Winter 2007 Final ExaminationDocument11 pagesAdms 2510 Winter 2007 Final ExaminationMohsin Rehman0% (1)

- Signal Cable Company: Cash Flow AnalysisDocument4 pagesSignal Cable Company: Cash Flow AnalysisRauf JaferiNo ratings yet

- Final ProjectDocument59 pagesFinal ProjectshelarnamdevNo ratings yet

- A Study On The Financial Analysis of Reliance Industries LimitedDocument13 pagesA Study On The Financial Analysis of Reliance Industries LimitedIJAR JOURNAL100% (1)

- 8e Ch3 Mini Case Planning MemoDocument8 pages8e Ch3 Mini Case Planning Memotom0% (3)

- Manager Selection - CFADocument148 pagesManager Selection - CFAJuliano VieiraNo ratings yet

- 67-1-2 (Accountancy)Document24 pages67-1-2 (Accountancy)tejNo ratings yet

- Declining Balance Depreciation Alpha 0.15 N 10Document2 pagesDeclining Balance Depreciation Alpha 0.15 N 10Ysabela Angela FloresNo ratings yet

- Governance Policies Procedures ManualDocument34 pagesGovernance Policies Procedures ManualmojiamaraNo ratings yet

- QP Accountancy XIIDocument9 pagesQP Accountancy XIITûshar ThakúrNo ratings yet

- Akl Kelompok 4Document15 pagesAkl Kelompok 4Sry WahyuniNo ratings yet

- Session 3 - Valuation Model - AirportsDocument105 pagesSession 3 - Valuation Model - AirportsPrathamesh GoreNo ratings yet

- Recitation Quiz 2Document5 pagesRecitation Quiz 2BlairEmrallafNo ratings yet

- Adobe Scan Jan 30, 2023Document6 pagesAdobe Scan Jan 30, 2023Karan RajakNo ratings yet

- Agriculture (Ias 41) : OpentuitionDocument15 pagesAgriculture (Ias 41) : OpentuitionHamza AliNo ratings yet

- Vertical Analysis - FordDocument4 pagesVertical Analysis - Fordayana atisNo ratings yet

- Gen 010 Q1 Sy2223Document5 pagesGen 010 Q1 Sy2223CLAIRE PAJONo ratings yet

- Chapter 32 - PFRS 5 Non Current Assets Held For SalesDocument2 pagesChapter 32 - PFRS 5 Non Current Assets Held For SalesLovely AbadianoNo ratings yet

- 1.1.1partnership FormationDocument12 pages1.1.1partnership FormationCundangan, Denzel Erick S.No ratings yet

- UT Dallas Syllabus For Aim2301.003 06s Taught by Xiaohui Liu (xxl046000)Document5 pagesUT Dallas Syllabus For Aim2301.003 06s Taught by Xiaohui Liu (xxl046000)UT Dallas Provost's Technology GroupNo ratings yet

- DK Goel Solutions Chapter 3 Changing in Profit Sharing Ratio Among The Existing PartnersDocument75 pagesDK Goel Solutions Chapter 3 Changing in Profit Sharing Ratio Among The Existing PartnersgunnNo ratings yet

- BSC Quiz On Chapters 1&2-2Document4 pagesBSC Quiz On Chapters 1&2-2Sachin KripalaniNo ratings yet

- Chapter 4Document73 pagesChapter 4Queenie RanqueNo ratings yet

- Mock BoardsDocument11 pagesMock BoardsRaenessa FranciscoNo ratings yet

- FAR270 JULY 2022 SolutionDocument8 pagesFAR270 JULY 2022 SolutionNur Fatin Amirah100% (1)

- Consolidated Financials Q4FY24Document10 pagesConsolidated Financials Q4FY24Akash KushwahaNo ratings yet

- Michael Guichon Sohn Conference Presentation - Fiat Chrysler AutomobilesDocument49 pagesMichael Guichon Sohn Conference Presentation - Fiat Chrysler AutomobilesCanadianValueNo ratings yet

- CR - MA-2023 - Suggested - AnswersDocument15 pagesCR - MA-2023 - Suggested - AnswersfahadsarkerNo ratings yet