You might also like

- RMC 42-99 17533-1999-Amending - Revenue - Memorandum - Circular - No.Document3 pagesRMC 42-99 17533-1999-Amending - Revenue - Memorandum - Circular - No.KC AtinonNo ratings yet

- Bir Ruling 044-10Document4 pagesBir Ruling 044-10Jason CertezaNo ratings yet

- Practice Test - Financial ManagementDocument6 pagesPractice Test - Financial Managementelongoria278100% (1)

- BIR Ruling No. 453-2018 Interest Income On Individual Loans Obtained From Banks That Are Not Securitized, Assigned or Participated OutDocument4 pagesBIR Ruling No. 453-2018 Interest Income On Individual Loans Obtained From Banks That Are Not Securitized, Assigned or Participated Outliz kawiNo ratings yet

- 1601EDocument7 pages1601EEnrique Membrere SupsupNo ratings yet

- Pbcom V CirDocument9 pagesPbcom V CirAbby ParwaniNo ratings yet

- Guidelines and Instruction For BIR Form No 1702 RTDocument2 pagesGuidelines and Instruction For BIR Form No 1702 RTRahrahrahn100% (2)

- RR 2-98 Section 2.57 (B) - CWTDocument3 pagesRR 2-98 Section 2.57 (B) - CWTZenaida LatorreNo ratings yet

- 62983rmo 5-2012Document14 pages62983rmo 5-2012Mark Dennis JovenNo ratings yet

- Refund of CWT and VAT Upon Dissolution of Company - ICN 9.11.14Document3 pagesRefund of CWT and VAT Upon Dissolution of Company - ICN 9.11.14JianSadakoNo ratings yet

- Tax Bulletin by SGV As of Oct 2014Document18 pagesTax Bulletin by SGV As of Oct 2014adobopinikpikanNo ratings yet

- Tax Update RR 18-2012Document32 pagesTax Update RR 18-2012johamarz6245No ratings yet

- 209890-2017-Opulent Landowners Inc. v. Commissioner of PDFDocument29 pages209890-2017-Opulent Landowners Inc. v. Commissioner of PDFJobar BuenaguaNo ratings yet

- BIR Ruling No. 242-18 (Gift Certs.)Document7 pagesBIR Ruling No. 242-18 (Gift Certs.)LizNo ratings yet

- BIR Ruling 456-2011Document5 pagesBIR Ruling 456-2011Mikz PolzzNo ratings yet

- Bir Ruling Da 086 08Document5 pagesBir Ruling Da 086 08Orlando O. CalundanNo ratings yet

- RMO No. 54-2016 PDFDocument3 pagesRMO No. 54-2016 PDFGabriel EdizaNo ratings yet

- Annex C-1 - Summary of System DescriptionDocument4 pagesAnnex C-1 - Summary of System DescriptionChristian Albert HerreraNo ratings yet

- Process For Application To Use LooseleafDocument1 pageProcess For Application To Use LooseleafFrancis MartinNo ratings yet

- Bcda IrrDocument28 pagesBcda IrrAlan TanNo ratings yet

- RR No. 03-98Document18 pagesRR No. 03-98fatmaaleahNo ratings yet

- WWHBQB Tawakkal 20191004162232Document1 pageWWHBQB Tawakkal 20191004162232Sherly ManoharaNo ratings yet

- BIR's New Invoicing Requirements Effective June 30, 2013Document2 pagesBIR's New Invoicing Requirements Effective June 30, 2013lito77No ratings yet

- BIR Form 2316 UndertakingDocument1 pageBIR Form 2316 UndertakingJan Paolo CruzNo ratings yet

- HGC 2015 - Notes To Financial StatementsDocument34 pagesHGC 2015 - Notes To Financial StatementsDeborah DelfinNo ratings yet

- BIR Ruling (DA - (TAR-001) 046-10)Document4 pagesBIR Ruling (DA - (TAR-001) 046-10)amadieu100% (1)

- Republic of The Philippines Application For: National Water Resources Board Renewal ofDocument2 pagesRepublic of The Philippines Application For: National Water Resources Board Renewal ofMark PesiganNo ratings yet

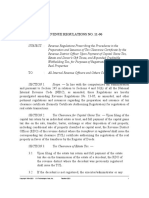

- BIR RegulationsDocument13 pagesBIR RegulationsDaphne Dione BelderolNo ratings yet

- Landlord Rental Increase LetterDocument2 pagesLandlord Rental Increase LetterNellie LennieNo ratings yet

- Proposal For Accounting Services PDFDocument2 pagesProposal For Accounting Services PDFJane Mara AquinoNo ratings yet

- Audit of Confidential Fund of LGUDocument16 pagesAudit of Confidential Fund of LGUBarwin Scott VillordonNo ratings yet

- CAR 2D Expanded Engagement Ltr-Compilation (5-17)Document8 pagesCAR 2D Expanded Engagement Ltr-Compilation (5-17)Andy RossNo ratings yet

- 267731702final PDFDocument5 pages267731702final PDFelmarcomonal100% (1)

- CSOC PawnshopDocument123 pagesCSOC Pawnshopaldred pera100% (1)

- Bir Ruling No. 108-93Document2 pagesBir Ruling No. 108-93saintkarriNo ratings yet

- COA12 Memo Jan2016Document3 pagesCOA12 Memo Jan2016aliahNo ratings yet

- Cta 2D CV 09224 M 2019feb12 AssDocument17 pagesCta 2D CV 09224 M 2019feb12 AssMelan YapNo ratings yet

- Unit 1F-4, 2F-4A & 2F-4B Philexcel Business Center 10, Philexcel Business Park, M. A. Roxas Highway, Clark Freeport Zone, PhilippinesDocument1 pageUnit 1F-4, 2F-4A & 2F-4B Philexcel Business Center 10, Philexcel Business Park, M. A. Roxas Highway, Clark Freeport Zone, PhilippinesElbert John BatarinaNo ratings yet

- Local Business TaxDocument2 pagesLocal Business TaxvenickeeNo ratings yet

- Checklist PcabDocument5 pagesChecklist PcabLyka Amascual ClaridadNo ratings yet

- Withholding Tax Remittance Return: Kawanihan NG Rentas InternasDocument4 pagesWithholding Tax Remittance Return: Kawanihan NG Rentas InternasArlyn De Las AlasNo ratings yet

- Revenue Regulations 9-98Document5 pagesRevenue Regulations 9-98Kayzer SabaNo ratings yet

- Guidelines and Conduct of TCVD RMO09-2006Document45 pagesGuidelines and Conduct of TCVD RMO09-2006Kris CalabiaNo ratings yet

- Journal Entry Voucher: Municipal Government of Lambunao Disbursement VoucherDocument12 pagesJournal Entry Voucher: Municipal Government of Lambunao Disbursement VoucherFrancisco Lubas Santillana IVNo ratings yet

- Buyer Registration Form: Procurement Service - PhilgepsDocument2 pagesBuyer Registration Form: Procurement Service - PhilgepsJefferson DayoNo ratings yet

- Application For Closure of BusinessDocument2 pagesApplication For Closure of BusinessallanNo ratings yet

- Citigroup Memo - Cut SpendingDocument4 pagesCitigroup Memo - Cut Spendingcutem100% (5)

- Ever Gotesco: Quarterly ReportDocument35 pagesEver Gotesco: Quarterly ReportBusinessWorld100% (1)

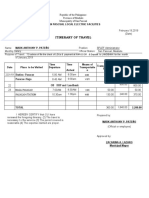

- Iterenary Travel FormDocument3 pagesIterenary Travel Formsplef lguNo ratings yet

- Spa September 2015 PDFDocument1 pageSpa September 2015 PDFsilverwind0% (3)

- PFF053 MembersContributionRemittanceForm V02-FillableDocument2 pagesPFF053 MembersContributionRemittanceForm V02-FillableCYvelle TorefielNo ratings yet

- RMC No. 28-2019Document2 pagesRMC No. 28-2019AmberlyNo ratings yet

- Revenue Audit Memorandum 1-98Document5 pagesRevenue Audit Memorandum 1-98Nikos CabreraNo ratings yet

- Sample On Professional Letter To ClientDocument4 pagesSample On Professional Letter To ClientcapslocktabNo ratings yet

- 038-16 Bir Ruling 191087-2016-Kyeryong - Construction - Industrial - Co. - Ltd.20190502-5466-1lm5il9Document4 pages038-16 Bir Ruling 191087-2016-Kyeryong - Construction - Industrial - Co. - Ltd.20190502-5466-1lm5il9KC AtinonNo ratings yet

- Bir Ruling (Da 146 04)Document4 pagesBir Ruling (Da 146 04)cool_peachNo ratings yet

- Tax Exemption For Nonprofit Schools: Artemio V. Panganiban @inquirerdotnetDocument3 pagesTax Exemption For Nonprofit Schools: Artemio V. Panganiban @inquirerdotnetKenneth Bryan Tegerero TegioNo ratings yet

- RMC 72-04Document9 pagesRMC 72-04ai0412No ratings yet

- RMC 72-2004 Issues On Withholding RatesDocument9 pagesRMC 72-2004 Issues On Withholding RatesEva HubadNo ratings yet

- Tax Brief - June 2012Document8 pagesTax Brief - June 2012Rheneir MoraNo ratings yet

- RR 11-96Document3 pagesRR 11-96Bobby LockNo ratings yet

- RMC No. 76-2020Document11 pagesRMC No. 76-2020Bobby LockNo ratings yet

- RR 12-18Document33 pagesRR 12-18Greg JalosNo ratings yet

- RR No. 23-2020Document1 pageRR No. 23-2020Bobby LockNo ratings yet

- RMC No. 76-2020Document11 pagesRMC No. 76-2020Bobby LockNo ratings yet

- RR No. 26 - 2020Document3 pagesRR No. 26 - 2020Bobby LockNo ratings yet

- 219258-2019-Commissioner of Internal Revenue v. La FlorDocument10 pages219258-2019-Commissioner of Internal Revenue v. La FlorJela KateNo ratings yet

- DOLE-department-order-no.-209 Series of 2020Document5 pagesDOLE-department-order-no.-209 Series of 2020attyjeckyNo ratings yet

- 2014 Sony Ericsson Mobile Communications20190404 5466 1t85ccrDocument13 pages2014 Sony Ericsson Mobile Communications20190404 5466 1t85ccrBobby LockNo ratings yet

- Ateneo vs. CIRDocument19 pagesAteneo vs. CIRBobby LockNo ratings yet

- Cta 1D CV 08405 D 2014nov07 RefDocument30 pagesCta 1D CV 08405 D 2014nov07 RefBobby LockNo ratings yet

- BIR Ruling On How To Compute Book Value If There Is Unpaid SubscriptionDocument3 pagesBIR Ruling On How To Compute Book Value If There Is Unpaid SubscriptionBobby LockNo ratings yet

- 32716-2013-Work-Around Guidelines and Procedures in The20190313-5466-17luyi PDFDocument20 pages32716-2013-Work-Around Guidelines and Procedures in The20190313-5466-17luyi PDFBobby LockNo ratings yet

- 203668-2016-Issue-Based Audit Under The VAT Audit Program20190424-5466-Gn0obh PDFDocument11 pages203668-2016-Issue-Based Audit Under The VAT Audit Program20190424-5466-Gn0obh PDFBobby LockNo ratings yet

- Cta 1D CV 08405 D 2014nov07 RefDocument30 pagesCta 1D CV 08405 D 2014nov07 RefBobby LockNo ratings yet

- RMC No. 35-2019Document1 pageRMC No. 35-2019Bobby LockNo ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon CityDocument53 pagesRepublic of The Philippines Court of Tax Appeals Quezon CityJanelle MupasNo ratings yet

- Rmo 20-2013Document7 pagesRmo 20-2013Carlos105No ratings yet

- Shirley Polotti, On Behalf of Herself and On Behalf of Her Infant Son, Charles F. Polotti v. Arthur S. Flemming, Secretary of Health, Education and Welfare, 277 F.2d 864, 2d Cir. (1960)Document5 pagesShirley Polotti, On Behalf of Herself and On Behalf of Her Infant Son, Charles F. Polotti v. Arthur S. Flemming, Secretary of Health, Education and Welfare, 277 F.2d 864, 2d Cir. (1960)Scribd Government DocsNo ratings yet

- Supreme Court of Sri Lanka Is Court of First InstanceDocument5 pagesSupreme Court of Sri Lanka Is Court of First Instancergsbandara4622No ratings yet

- RA 9165 PowerpointDocument34 pagesRA 9165 Powerpointaldin80% (5)

- Nazara Technologies LimitedDocument18 pagesNazara Technologies LimitedMk ChanduNo ratings yet

- Author Agent AgreementDocument3 pagesAuthor Agent Agreementapi-276184973100% (1)

- Supreme Court Graphic Designer First Amendment OpinionDocument70 pagesSupreme Court Graphic Designer First Amendment OpinionZerohedgeNo ratings yet

- Offences Against PropertyDocument4 pagesOffences Against PropertyMOUSOM ROYNo ratings yet

- Ebralinag vs. Division Superintendent of CebuDocument1 pageEbralinag vs. Division Superintendent of CebuVin LacsieNo ratings yet

- Donton Vs TansingcoDocument8 pagesDonton Vs Tansingcokristian datinguinooNo ratings yet

- Convention C081 - Labour Inspection Convention, 1947 (No. 81)Document8 pagesConvention C081 - Labour Inspection Convention, 1947 (No. 81)Elmir ƏzimovNo ratings yet

- David Earl Fore v. United States, 395 F.2d 548, 10th Cir. (1968)Document8 pagesDavid Earl Fore v. United States, 395 F.2d 548, 10th Cir. (1968)Scribd Government DocsNo ratings yet

- Notice: Culturally Significant Objects Imported For Exhibition: Aondo-Sanchez, Jesus, Et Al.Document1 pageNotice: Culturally Significant Objects Imported For Exhibition: Aondo-Sanchez, Jesus, Et Al.Justia.comNo ratings yet

- LLM SylDocument32 pagesLLM SylkshitijsaxenaNo ratings yet

- Balindong vs. CA, G.R. Nos. 177600 and 178684, 19 October 2015Document3 pagesBalindong vs. CA, G.R. Nos. 177600 and 178684, 19 October 2015Gwendelyn Peñamayor-MercadoNo ratings yet

- English Import Declarion JapanDocument1 pageEnglish Import Declarion JapanMainak MukherjeeNo ratings yet

- Gun ControlDocument7 pagesGun Controlapi-309774071No ratings yet

- Moot RK Yadav Issue 3Document5 pagesMoot RK Yadav Issue 3Ridam GangwarNo ratings yet

- Consultant For Development and Operation of National Data and Analytics Platform (NDAP)Document157 pagesConsultant For Development and Operation of National Data and Analytics Platform (NDAP)antara choudhury khannaNo ratings yet

- 118 Telengtan Brothers & Sons, Inc. v. Court of AppealsDocument4 pages118 Telengtan Brothers & Sons, Inc. v. Court of AppealsRem Serrano100% (1)

- United States Court of Appeals: For The First CircuitDocument22 pagesUnited States Court of Appeals: For The First CircuitScribd Government DocsNo ratings yet

- Escott v. BarChris ConstructionDocument4 pagesEscott v. BarChris ConstructionLynne SanchezNo ratings yet

- FIA McqsDocument2 pagesFIA McqszirfayNo ratings yet

- in Re Estate of JohnsonDocument8 pagesin Re Estate of JohnsonaudreyNo ratings yet

- Relevant Facts: Re: Definition of GamblingDocument3 pagesRelevant Facts: Re: Definition of GamblingMaria AnalynNo ratings yet

- Aircraft Dispatcher: Practical Test StandardsDocument27 pagesAircraft Dispatcher: Practical Test Standardshdy_kml100% (1)

- Air and Space LawDocument52 pagesAir and Space LawBharath SimhaReddyNaidu100% (1)

- G.R. No. 196329 Roman v. Sec Case DigestDocument4 pagesG.R. No. 196329 Roman v. Sec Case DigestPlandito ElizabethNo ratings yet

- The State Education Department / The University of The State of New York / Albany, Ny 12234Document6 pagesThe State Education Department / The University of The State of New York / Albany, Ny 12234jspectorNo ratings yet

- Notice U/s. 138 of N. I. Act by R.P.A.D.: Disha Enterprise Gujarati Galii, Hanuman Chwok, Ganj Golai, LaturDocument3 pagesNotice U/s. 138 of N. I. Act by R.P.A.D.: Disha Enterprise Gujarati Galii, Hanuman Chwok, Ganj Golai, LaturAdv Prashantb JadhavNo ratings yet

- UntitledDocument14 pagesUntitledoutdash2No ratings yet