You might also like

- Controlling Payroll Cost - Critical Disciplines for Club ProfitabilityFrom EverandControlling Payroll Cost - Critical Disciplines for Club ProfitabilityNo ratings yet

- The Financial Accounting Cycle PDFDocument219 pagesThe Financial Accounting Cycle PDFQuadjo Opoku Sarkodie100% (1)

- Introduction To Cost and Management AccountingDocument3 pagesIntroduction To Cost and Management AccountingTheaNo ratings yet

- Accounting Financial: General LedgerDocument8 pagesAccounting Financial: General LedgerSumeet KaurNo ratings yet

- Assignment 04 Cash Flow StatementDocument6 pagesAssignment 04 Cash Flow Statementumair iqbalNo ratings yet

- Framework of Accounting2Document103 pagesFramework of Accounting2Harold B. Lacaba100% (1)

- Accounting BasicsDocument13 pagesAccounting BasicskameshpatilNo ratings yet

- Basic BookkeepingDocument80 pagesBasic BookkeepingCharity CotejoNo ratings yet

- Financial Accounting Chapter 3Document5 pagesFinancial Accounting Chapter 3NiraniyaNo ratings yet

- Lesson 1Document9 pagesLesson 1Bervette HansNo ratings yet

- Accounting Adjustments and Constructing The Financial StatementsDocument12 pagesAccounting Adjustments and Constructing The Financial StatementsKwaku DanielNo ratings yet

- ACCOUNTING FOR CORPORATES (BBBH233) - 001 Module 1 - 1573561029351Document66 pagesACCOUNTING FOR CORPORATES (BBBH233) - 001 Module 1 - 1573561029351Harshit Kumar GuptaNo ratings yet

- QuickBooks Online No MC COA Sample FileDocument2 pagesQuickBooks Online No MC COA Sample FilecardiacanesthesiaNo ratings yet

- Final Exam - 2020Document10 pagesFinal Exam - 2020mshan lee100% (1)

- Accounting Journal Entries With Business Transactions PDFDocument7 pagesAccounting Journal Entries With Business Transactions PDFBackchodi OverLoadedNo ratings yet

- Recording of Business TransactionsDocument30 pagesRecording of Business TransactionsAnthony John BrionesNo ratings yet

- Business Plan TemplateDocument7 pagesBusiness Plan TemplateRohan LabdeNo ratings yet

- Adjusting Entries Chapter $Document56 pagesAdjusting Entries Chapter $Arzan AliNo ratings yet

- Capital Vs Revenue Exp..... Point PresentationDocument16 pagesCapital Vs Revenue Exp..... Point PresentationVinay Kumar100% (1)

- XL JournalSHEET - Accounting System V3.43 - Merchandise - Lite V3Document686 pagesXL JournalSHEET - Accounting System V3.43 - Merchandise - Lite V3Satria ArliandiNo ratings yet

- Trial BalanceDocument12 pagesTrial BalanceAshish ToppoNo ratings yet

- My Presentation About PayRoll SystemDocument3 pagesMy Presentation About PayRoll SystemAzeem Asim MughalNo ratings yet

- Final Accounts: Manufacturing, Trading and P&L A/cDocument51 pagesFinal Accounts: Manufacturing, Trading and P&L A/cAnit Jacob Philip100% (1)

- Accounting Equation (Abm)Document43 pagesAccounting Equation (Abm)EasyGaming100% (1)

- Chart of Accounts PolicyDocument13 pagesChart of Accounts PolicyMazhar Ali JoyoNo ratings yet

- Acct TutorDocument22 pagesAcct TutorKthln Mntlla100% (1)

- DAWN Editorials - November 2016Document92 pagesDAWN Editorials - November 2016SurvivorFsdNo ratings yet

- Finance Chart of AccountsDocument1 pageFinance Chart of AccountscahyoNo ratings yet

- Introduction To AccountingDocument51 pagesIntroduction To Accountingmonkey bean100% (1)

- Double Entry SystemDocument19 pagesDouble Entry SystemanitikaNo ratings yet

- Trading AccountDocument3 pagesTrading AccountRirin GhariniNo ratings yet

- Ch-5 Cash Flow AnalysisDocument9 pagesCh-5 Cash Flow AnalysisQiqi GenshinNo ratings yet

- Accounting CycleDocument7 pagesAccounting CycleJenny BernardinoNo ratings yet

- Adjusting EntryDocument48 pagesAdjusting EntryKentoy Serezo Villanura100% (1)

- Revenue Cycle ReportDocument15 pagesRevenue Cycle ReportKevin Lloyd GallardoNo ratings yet

- The Role of Accounting in BusinessDocument18 pagesThe Role of Accounting in BusinessJawad AzizNo ratings yet

- Topic 4 - Adjusting Accounts and Preparing Financial StatementsDocument18 pagesTopic 4 - Adjusting Accounts and Preparing Financial Statementsapi-388504348100% (1)

- Fundamentals of Accounting, Business & Management 2: Name: Date: Grade/Yr.: Score: General JournalDocument10 pagesFundamentals of Accounting, Business & Management 2: Name: Date: Grade/Yr.: Score: General JournalDindin Oromedlav LoricaNo ratings yet

- Journalizing, Posting and BalancingDocument21 pagesJournalizing, Posting and Balancinganuradha100% (1)

- Accounting Terms A Quick Reference GuideDocument9 pagesAccounting Terms A Quick Reference GuideShreekumarNo ratings yet

- Accounting CycleDocument9 pagesAccounting CycleRosethel Grace GallardoNo ratings yet

- Abm1 PPTDocument161 pagesAbm1 PPTPavi Antoni Villaceran100% (1)

- Chapter 3 AccountingDocument11 pagesChapter 3 AccountingĐỗ ĐăngNo ratings yet

- Problems Journal EntryDocument5 pagesProblems Journal EntryColleen GuimbalNo ratings yet

- Source Document of AccountancyDocument7 pagesSource Document of AccountancyVinod GandhiNo ratings yet

- Taxation of Income of Individuals IDocument61 pagesTaxation of Income of Individuals ICaroline Muthoni Mwangi100% (1)

- BRS, IASB FRMWKDocument4 pagesBRS, IASB FRMWKNadir MuhammadNo ratings yet

- Accounting Level 3 Assessment - Cluster 8Document8 pagesAccounting Level 3 Assessment - Cluster 8Stephen PommellsNo ratings yet

- Lecture 4 Lecture Notes 2011Document27 pagesLecture 4 Lecture Notes 2011Misu NguyenNo ratings yet

- List of Business Transactions (Edited) : The Rose and Flower Owned by Rose GreenDocument2 pagesList of Business Transactions (Edited) : The Rose and Flower Owned by Rose GreenJon DonNo ratings yet

- Chqpte 1 7 Practice TestsDocument6 pagesChqpte 1 7 Practice TestsI IvaNo ratings yet

- Chapter 2 Payroll Accounting 2018Document53 pagesChapter 2 Payroll Accounting 2018Gabi Mihalek100% (1)

- Leonardo Wagster Decided To Open Wagster's Window Washing On September 1, 2020. in September, The Following Transactions Took PlaceDocument12 pagesLeonardo Wagster Decided To Open Wagster's Window Washing On September 1, 2020. in September, The Following Transactions Took PlaceJohnMurray111100% (1)

- How To Create A WorksheetDocument3 pagesHow To Create A WorksheetMary100% (2)

- PartnershipDocument41 pagesPartnershipBinex67% (3)

- Management Accounting Chapter 1Document4 pagesManagement Accounting Chapter 1Ieda ShaharNo ratings yet

- Ch13. Flexible BudgetDocument36 pagesCh13. Flexible Budgetnicero555No ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Chapter 02 Job Order CostingDocument52 pagesChapter 02 Job Order Costingbaloojan100% (1)

- Assistant Accountant CV TemplateDocument2 pagesAssistant Accountant CV TemplateShifan IshakNo ratings yet

- A Step Locla Network GuideDocument7 pagesA Step Locla Network GuideKashif KhanNo ratings yet

- Step by Step Guide For Connecting PC To Wired LAN at Dormitories of University of PardubiceDocument19 pagesStep by Step Guide For Connecting PC To Wired LAN at Dormitories of University of Pardubicehumayun.sabirNo ratings yet

- Quickbooks Lessons OutlinesDocument3 pagesQuickbooks Lessons OutlinesKashif KhanNo ratings yet

- A Quickbooks Accounting PrimerDocument40 pagesA Quickbooks Accounting PrimerShailesh Patel100% (3)

- Peachtree InstructionsDocument5 pagesPeachtree InstructionsKashif KhanNo ratings yet

- Adjusting EntryDocument17 pagesAdjusting EntryKashif KhanNo ratings yet

- Waqas CVDocument1 pageWaqas CVKashif KhanNo ratings yet

- Adjusting EntriesDocument11 pagesAdjusting EntriesShruti SinghNo ratings yet

- Quick Books For Real EstateDocument34 pagesQuick Books For Real EstateKashif KhanNo ratings yet

- Tally - ERP 9: Settle Multiple Bills Through Bill Settlement in Tally - ERP 9Document5 pagesTally - ERP 9: Settle Multiple Bills Through Bill Settlement in Tally - ERP 9Kashif KhanNo ratings yet

- QuickBooks Job CostingDocument100 pagesQuickBooks Job CostingKashif Khan100% (1)

- Fund Transfer Request Letter To BankDocument1 pageFund Transfer Request Letter To BankKashif KhanNo ratings yet

- Revenue RecognitionDocument4 pagesRevenue RecognitionKashif KhanNo ratings yet

- Common QB MistakesDocument117 pagesCommon QB Mistakesca_cp1No ratings yet

- Quickbooks Online 2013 Recording TransDocument75 pagesQuickbooks Online 2013 Recording TransKashif KhanNo ratings yet

- Kashif Riaz: Retail AssistantDocument1 pageKashif Riaz: Retail AssistantKashif KhanNo ratings yet

- Kashif Riaz: Retail AssistantDocument1 pageKashif Riaz: Retail AssistantKashif KhanNo ratings yet

- Order Booking Form New Formate 02.09.2013Document2 pagesOrder Booking Form New Formate 02.09.2013Kashif KhanNo ratings yet

- Chapter No 02 9th Class Notes PDFDocument4 pagesChapter No 02 9th Class Notes PDFKashif KhanNo ratings yet

- AccountantDocument3 pagesAccountantKashif KhanNo ratings yet

- 2010 Auditors ReportDocument1 page2010 Auditors ReportKashif KhanNo ratings yet

- SalesOrd 173 From Venus Carpets 2676 PDFDocument1 pageSalesOrd 173 From Venus Carpets 2676 PDFKashif KhanNo ratings yet

- Computation of Depreciation On Extra Shift WorkingsDocument3 pagesComputation of Depreciation On Extra Shift WorkingsKashif KhanNo ratings yet

- Computation of Depreciation On Extra Shift WorkingsDocument3 pagesComputation of Depreciation On Extra Shift WorkingsKashif KhanNo ratings yet

- Capital and RevenueDocument23 pagesCapital and RevenueDhwani PanditNo ratings yet

- TeacherResume11 12Document2 pagesTeacherResume11 12Shilpa AshokNo ratings yet

- Median For Grouped DataDocument4 pagesMedian For Grouped DataKashif KhanNo ratings yet

- 1 1meaningDocument21 pages1 1meaningadtyshkhrNo ratings yet

- B40Document7 pagesB40ambujg0% (1)

- Request-Flagstar Bancorp - Special Meeting Notice and Proxy StatementDocument32 pagesRequest-Flagstar Bancorp - Special Meeting Notice and Proxy StatementDvNetNo ratings yet

- International Storytelling Center - Chapter 11 Bankruptcy Filings - Amended Creditor MatrixDocument4 pagesInternational Storytelling Center - Chapter 11 Bankruptcy Filings - Amended Creditor MatrixTennesseeTuxedoNo ratings yet

- Recall Notice SHPLDocument5 pagesRecall Notice SHPLShriya Vikram ShahNo ratings yet

- Arundal Case Study Answer FinalDocument7 pagesArundal Case Study Answer FinalEmma Keane100% (1)

- EY LBO ModellingDocument8 pagesEY LBO ModellingPrashantKNo ratings yet

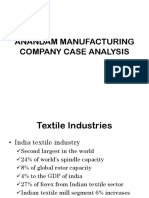

- Anandham CaseDocument17 pagesAnandham Casekarthick raj100% (1)

- 1Document56 pages1Renee WilliamsNo ratings yet

- CIV 2 - 2013 - Case Digests - SY 2014-2015Document193 pagesCIV 2 - 2013 - Case Digests - SY 2014-2015Marife Tubilag ManejaNo ratings yet

- Punjab Apartment and Property Regulation ActDocument21 pagesPunjab Apartment and Property Regulation ActHemantSharmaNo ratings yet

- Extra Payment CalculatorDocument12 pagesExtra Payment CalculatorZafar AhmedNo ratings yet

- Howey Test For Ayin Token Securities Assessment Rev. 1Document10 pagesHowey Test For Ayin Token Securities Assessment Rev. 1AYIN International, Inc.No ratings yet

- CH 5 - Mathematics of FinanceDocument29 pagesCH 5 - Mathematics of FinanceSherie LynneNo ratings yet

- Cvs Mail Service Invoice/ReceiptDocument1 pageCvs Mail Service Invoice/Receipthbryant587No ratings yet

- EF3e Int Filetest 2aDocument6 pagesEF3e Int Filetest 2aJhony EspinozaNo ratings yet

- Some Aspects of The Rights and Liabilities of Mortgagee, MortgagoRDocument32 pagesSome Aspects of The Rights and Liabilities of Mortgagee, MortgagoRSejal LahotiNo ratings yet

- Electronics BBA MBA Project ReportDocument50 pagesElectronics BBA MBA Project ReportpRiNcE DuDhAtRaNo ratings yet

- Mid Term Exam MCQs For 5530Document6 pagesMid Term Exam MCQs For 5530Amy WangNo ratings yet

- Notes Banking For 2nd Year (Commerce)Document72 pagesNotes Banking For 2nd Year (Commerce)pariworld65100% (4)

- Copyright NoticeDocument3 pagesCopyright NoticeJohn Wallace100% (13)

- The Most Dangerous Organization in America ExposedDocument37 pagesThe Most Dangerous Organization in America ExposedDomenico Bevilacqua100% (1)

- CHAPTER 2 Review of Financial Statement Preparation, Analysis, and InterpretationDocument6 pagesCHAPTER 2 Review of Financial Statement Preparation, Analysis, and InterpretationCatherine Rivera100% (3)

- City Limits Magazine, March 1985 IssueDocument24 pagesCity Limits Magazine, March 1985 IssueCity Limits (New York)No ratings yet

- Cost Accounting Level 3/series 3-2009Document19 pagesCost Accounting Level 3/series 3-2009Hein Linn Kyaw100% (2)

- Gomez-Jimenez v. NYLS: Motion For Leave To AppealDocument51 pagesGomez-Jimenez v. NYLS: Motion For Leave To AppealStaci ZaretskyNo ratings yet

- Chapter 20 - Audit of NBFC PDFDocument4 pagesChapter 20 - Audit of NBFC PDFRakhi SinghalNo ratings yet

- Philsec Investment Corp., V. CADocument2 pagesPhilsec Investment Corp., V. CARalph Deric EspirituNo ratings yet

- Invoice 120289103981Document1 pageInvoice 120289103981Nuhu Ibrahim MaigariNo ratings yet

- Audit Procedure For LIABILITIESDocument2 pagesAudit Procedure For LIABILITIESDana67% (3)