You might also like

- 1992 Mannino Sindaco Gemellaggio Isola Delle Femmine Pittsburg Stefano Bologna Giucastro Bruno Pietro Ingegnere Rappa Rocco PDFDocument1 page1992 Mannino Sindaco Gemellaggio Isola Delle Femmine Pittsburg Stefano Bologna Giucastro Bruno Pietro Ingegnere Rappa Rocco PDFPino CiampolilloNo ratings yet

- Bertolino Giuseppe 04 02 1902 Fu Gaspare 323 194 Falcone Borsellino Guarotta Caponnetto Di Lello Mandati Di Cattura Tribunale Di Palermo Bruno Francesco Di Antonino 27 05 51 LatitanteDocument20 pagesBertolino Giuseppe 04 02 1902 Fu Gaspare 323 194 Falcone Borsellino Guarotta Caponnetto Di Lello Mandati Di Cattura Tribunale Di Palermo Bruno Francesco Di Antonino 27 05 51 LatitantePino CiampolilloNo ratings yet

- Bertolino Giuseppe 04 02 1902 Fu Gaspare 323 194 Falcone Borsellino Guarotta Caponnetto Di Lello Mandati Di Cattura Tribunale Di Palermo Bruno Francesco Di Antonino 27 05 51 LatitanteDocument20 pagesBertolino Giuseppe 04 02 1902 Fu Gaspare 323 194 Falcone Borsellino Guarotta Caponnetto Di Lello Mandati Di Cattura Tribunale Di Palermo Bruno Francesco Di Antonino 27 05 51 LatitantePino CiampolilloNo ratings yet

- Bertolino Giuseppe 04 02 1902 Fu Gaspare 323 194 Falcone Borsellino Guarotta Caponnetto Di Lello Mandati Di Cattura Tribunale Di Palermo Bruno Francesco Di Antonino 27 05 51 LatitanteDocument20 pagesBertolino Giuseppe 04 02 1902 Fu Gaspare 323 194 Falcone Borsellino Guarotta Caponnetto Di Lello Mandati Di Cattura Tribunale Di Palermo Bruno Francesco Di Antonino 27 05 51 LatitantePino CiampolilloNo ratings yet

- Festival Uniti Annullamento Manifestazione Estiva A Isola Delle FemmineDocument1 pageFestival Uniti Annullamento Manifestazione Estiva A Isola Delle FemminePino CiampolilloNo ratings yet

- BERTOLINO GIUSEPPE 04 02 1902 FU GASPARE 323 194 FALCONE BORSELLINO GUAROTTA CAPONNETTO DI LELLO MANDATI DI CATTURA TRIBUNALE DI PALERMO BRUNO FRANCESCO DI ANTONINO 27 05 51 LATITANTE FICARRA GIUSEPPE FU NICOLO' 24 07 21 VIA MATTEOTTI 8 ISOLA DELLE FEMMINE LO IACONO PIETRO 19 08 27 LOTTIZZAZIONE LO BIANCO: http://isoladellefemminepulita.blogspot.it/2011/10/isola-delle-femmine-lottizzazione-lo.htmlDocument20 pagesBERTOLINO GIUSEPPE 04 02 1902 FU GASPARE 323 194 FALCONE BORSELLINO GUAROTTA CAPONNETTO DI LELLO MANDATI DI CATTURA TRIBUNALE DI PALERMO BRUNO FRANCESCO DI ANTONINO 27 05 51 LATITANTE FICARRA GIUSEPPE FU NICOLO' 24 07 21 VIA MATTEOTTI 8 ISOLA DELLE FEMMINE LO IACONO PIETRO 19 08 27 LOTTIZZAZIONE LO BIANCO: http://isoladellefemminepulita.blogspot.it/2011/10/isola-delle-femmine-lottizzazione-lo.htmlPino CiampolilloNo ratings yet

- BERTOLINO GIUSEPPE 04 02 1902 FU GASPARE 323 194 FALCONE BORSELLINO GUAROTTA CAPONNETTO DI LELLO MANDATI DI CATTURA TRIBUNALE DI PALERMO BRUNO FRANCESCO DI ANTONINO 27 05 51 LATITANTE FICARRA GIUSEPPE FU NICOLO' 24 07 21 VIA MATTEOTTI 8 ISOLA DELLE FEMMINE LO IACONO PIETRO 19 08 27 LOTTIZZAZIONE LO BIANCO: http://isoladellefemminepulita.blogspot.it/2011/10/isola-delle-femmine-lottizzazione-lo.htmlDocument20 pagesBERTOLINO GIUSEPPE 04 02 1902 FU GASPARE 323 194 FALCONE BORSELLINO GUAROTTA CAPONNETTO DI LELLO MANDATI DI CATTURA TRIBUNALE DI PALERMO BRUNO FRANCESCO DI ANTONINO 27 05 51 LATITANTE FICARRA GIUSEPPE FU NICOLO' 24 07 21 VIA MATTEOTTI 8 ISOLA DELLE FEMMINE LO IACONO PIETRO 19 08 27 LOTTIZZAZIONE LO BIANCO: http://isoladellefemminepulita.blogspot.it/2011/10/isola-delle-femmine-lottizzazione-lo.htmlPino CiampolilloNo ratings yet

- Bertolino Giuseppe 04 02 1902 Fu Gaspare 323 194 Falcone Borsellino Guarotta Caponnetto Di Lello Mandati Di Cattura Tribunale Di Palermo Bruno Francesco Di Antonino 27 05 51 LatitanteDocument20 pagesBertolino Giuseppe 04 02 1902 Fu Gaspare 323 194 Falcone Borsellino Guarotta Caponnetto Di Lello Mandati Di Cattura Tribunale Di Palermo Bruno Francesco Di Antonino 27 05 51 LatitantePino CiampolilloNo ratings yet

- BERTOLINO GIUSEPPE 04 02 1902 FU GASPARE 323 194 FALCONE BORSELLINO GUAROTTA CAPONNETTO DI LELLO MANDATI DI CATTURA TRIBUNALE DI PALERMO BRUNO FRANCESCO DI ANTONINO 27 05 51 LATITANTE FICARRA GIUSEPPE FU NICOLO' 24 07 21 VIA MATTEOTTI 8 ISOLA DELLE FEMMINE LO IACONO PIETRO 19 08 27 LOTTIZZAZIONE LO BIANCO: http://isoladellefemminepulita.blogspot.it/2011/10/isola-delle-femmine-lottizzazione-lo.htmlDocument20 pagesBERTOLINO GIUSEPPE 04 02 1902 FU GASPARE 323 194 FALCONE BORSELLINO GUAROTTA CAPONNETTO DI LELLO MANDATI DI CATTURA TRIBUNALE DI PALERMO BRUNO FRANCESCO DI ANTONINO 27 05 51 LATITANTE FICARRA GIUSEPPE FU NICOLO' 24 07 21 VIA MATTEOTTI 8 ISOLA DELLE FEMMINE LO IACONO PIETRO 19 08 27 LOTTIZZAZIONE LO BIANCO: http://isoladellefemminepulita.blogspot.it/2011/10/isola-delle-femmine-lottizzazione-lo.htmlPino CiampolilloNo ratings yet

- Bertolino Giuseppe 04 02 1902 Fu Gaspare 323 194 Falcone Borsellino Guarotta Caponnetto Di Lello Mandati Di Cattura Tribunale Di Palermo Bruno Francesco Di Antonino 27 05 51 LatitanteDocument20 pagesBertolino Giuseppe 04 02 1902 Fu Gaspare 323 194 Falcone Borsellino Guarotta Caponnetto Di Lello Mandati Di Cattura Tribunale Di Palermo Bruno Francesco Di Antonino 27 05 51 LatitantePino CiampolilloNo ratings yet

- FESTIVAL UNITI PROTOCOLLO INTESA MANIFESTAZIONI ESTIVE ISOLA DELLE FEMMINE Documento-97150Document2 pagesFESTIVAL UNITI PROTOCOLLO INTESA MANIFESTAZIONI ESTIVE ISOLA DELLE FEMMINE Documento-97150Pino CiampolilloNo ratings yet

- ITALCEMENTI 2015 10 NOVEMBRE RISPOSTA ALLA DIFIDA 1 SERVIZIO VERACE PROT 47711 19 10 2015 ISO002 - 50032 - 2 VDG Amb-A0+Document1 pageITALCEMENTI 2015 10 NOVEMBRE RISPOSTA ALLA DIFIDA 1 SERVIZIO VERACE PROT 47711 19 10 2015 ISO002 - 50032 - 2 VDG Amb-A0+Pino CiampolilloNo ratings yet

- BERTOLINO GIUSEPPE 04 02 1902 FU GASPARE 323 194 FALCONE BORSELLINO GUAROTTA CAPONNETTO DI LELLO MANDATI DI CATTURA TRIBUNALE DI PALERMO BRUNO FRANCESCO DI ANTONINO 27 05 51 LATITANTE FICARRA GIUSEPPE FU NICOLO' 24 07 21 VIA MATTEOTTI 8 ISOLA DELLE FEMMINE LO IACONO PIETRO 19 08 27 LOTTIZZAZIONE LO BIANCO: http://isoladellefemminepulita.blogspot.it/2011/10/isola-delle-femmine-lottizzazione-lo.htmlDocument20 pagesBERTOLINO GIUSEPPE 04 02 1902 FU GASPARE 323 194 FALCONE BORSELLINO GUAROTTA CAPONNETTO DI LELLO MANDATI DI CATTURA TRIBUNALE DI PALERMO BRUNO FRANCESCO DI ANTONINO 27 05 51 LATITANTE FICARRA GIUSEPPE FU NICOLO' 24 07 21 VIA MATTEOTTI 8 ISOLA DELLE FEMMINE LO IACONO PIETRO 19 08 27 LOTTIZZAZIONE LO BIANCO: http://isoladellefemminepulita.blogspot.it/2011/10/isola-delle-femmine-lottizzazione-lo.htmlPino CiampolilloNo ratings yet

- 2013 29 LUGLIO 10163 PROT INGEGNERE RAPPA ROCCO CIMITERO ISOLA DELLE FEMMINE ROCCO RAPPA ING RELAZIONE TECNICA ASSEVERATA RICHIESTA DI BADALAMENTI SALVATORE EREDE GRILLI ELISA TOMBA GENTILIZIA BRUNO GIUSEPPE FRATELLO DI GIOVANNI STAMPA N 55 CDocument4 pages2013 29 LUGLIO 10163 PROT INGEGNERE RAPPA ROCCO CIMITERO ISOLA DELLE FEMMINE ROCCO RAPPA ING RELAZIONE TECNICA ASSEVERATA RICHIESTA DI BADALAMENTI SALVATORE EREDE GRILLI ELISA TOMBA GENTILIZIA BRUNO GIUSEPPE FRATELLO DI GIOVANNI STAMPA N 55 CPino CiampolilloNo ratings yet

- BERTOLINO GIUSEPPE 04 02 1902 FU GASPARE 323 194 FALCONE BORSELLINO GUAROTTA CAPONNETTO DI LELLO MANDATI DI CATTURA TRIBUNALE DI PALERMO BRUNO FRANCESCO DI ANTONINO 27 05 51 LATITANTE FICARRA GIUSEPPE FU NICOLO' 24 07 21 VIA MATTEOTTI 8 ISOLA DELLE FEMMINE LO IACONO PIETRO 19 08 27 LOTTIZZAZIONE LO BIANCO: http://isoladellefemminepulita.blogspot.it/2011/10/isola-delle-femmine-lottizzazione-lo.htmlDocument20 pagesBERTOLINO GIUSEPPE 04 02 1902 FU GASPARE 323 194 FALCONE BORSELLINO GUAROTTA CAPONNETTO DI LELLO MANDATI DI CATTURA TRIBUNALE DI PALERMO BRUNO FRANCESCO DI ANTONINO 27 05 51 LATITANTE FICARRA GIUSEPPE FU NICOLO' 24 07 21 VIA MATTEOTTI 8 ISOLA DELLE FEMMINE LO IACONO PIETRO 19 08 27 LOTTIZZAZIONE LO BIANCO: http://isoladellefemminepulita.blogspot.it/2011/10/isola-delle-femmine-lottizzazione-lo.htmlPino CiampolilloNo ratings yet

- ITALCEMENTI 2015 10 NOVEMBRE RISPOSTA ALLA DIFIDA 1 SERVIZIO VERACE PROT 47711 19 10 2015 ISO002 - 50034 - 2 VDG Amb-A2Document1 pageITALCEMENTI 2015 10 NOVEMBRE RISPOSTA ALLA DIFIDA 1 SERVIZIO VERACE PROT 47711 19 10 2015 ISO002 - 50034 - 2 VDG Amb-A2Pino CiampolilloNo ratings yet

- ITALCEMENTI 2015 10 NOVEMBRE RISPOSTA ALLA DIFIDA 1 SERVIZIO VERACE PROT 47711 19 10 2015 ISO002 - 50017 - 2C VDG AmbDocument1 pageITALCEMENTI 2015 10 NOVEMBRE RISPOSTA ALLA DIFIDA 1 SERVIZIO VERACE PROT 47711 19 10 2015 ISO002 - 50017 - 2C VDG AmbPino CiampolilloNo ratings yet

- STEFANINI Abusivismo Via RomaDocument2 pagesSTEFANINI Abusivismo Via RomaPino CiampolilloNo ratings yet

- ITALCEMENTI 2015 10 NOVEMBRE RISPOSTA ALLA DIFIDA 1 SERVIZIO VERACE PROT 47711 19 10 2015 ISO002 - 50032 - 2 VDG Amb-A0+Document1 pageITALCEMENTI 2015 10 NOVEMBRE RISPOSTA ALLA DIFIDA 1 SERVIZIO VERACE PROT 47711 19 10 2015 ISO002 - 50032 - 2 VDG Amb-A0+Pino CiampolilloNo ratings yet

- ITALCEMENTI 2015 24 NOVEMBRE CONFERENZA PARIGI 15 - 11 - 24 - NatixisConference - Final PDFDocument60 pagesITALCEMENTI 2015 24 NOVEMBRE CONFERENZA PARIGI 15 - 11 - 24 - NatixisConference - Final PDFPino CiampolilloNo ratings yet

- Italcementi 2015 Novembre Terzo Trimestre 2015 Itc - 3 - Trimestrale - 2015uk.Document48 pagesItalcementi 2015 Novembre Terzo Trimestre 2015 Itc - 3 - Trimestrale - 2015uk.Pino CiampolilloNo ratings yet

- Amap 2016 Budget Piano IndustrialeDocument78 pagesAmap 2016 Budget Piano IndustrialePino CiampolilloNo ratings yet

- Italcementi 2014 Ourworld 31 12 2014Document49 pagesItalcementi 2014 Ourworld 31 12 2014Pino CiampolilloNo ratings yet

- ITALCEMENTI 2015 24 NOVEMBRE CONFERENZA PARIGI 15 - 11 - 24 - NatixisConference - Final PDFDocument60 pagesITALCEMENTI 2015 24 NOVEMBRE CONFERENZA PARIGI 15 - 11 - 24 - NatixisConference - Final PDFPino CiampolilloNo ratings yet

- Italcementi 2014 Ourworld 31 12 2014Document49 pagesItalcementi 2014 Ourworld 31 12 2014Pino CiampolilloNo ratings yet

- ITALCEMENTI 2015 24 NOVEMBRE CONFERENZA PARIGI 15 - 11 - 24 - NatixisConference - Final PDFDocument60 pagesITALCEMENTI 2015 24 NOVEMBRE CONFERENZA PARIGI 15 - 11 - 24 - NatixisConference - Final PDFPino CiampolilloNo ratings yet

- Italcementi 2015 Novembre Terzo Trimestre 2015 Itc - 3 - Trimestrale - 2015uk.Document48 pagesItalcementi 2015 Novembre Terzo Trimestre 2015 Itc - 3 - Trimestrale - 2015uk.Pino CiampolilloNo ratings yet

- ITALCEMENTI 2015 24 NOVEMBRE CONFERENZA PARIGI 15 - 11 - 24 - NatixisConference - Final PDFDocument60 pagesITALCEMENTI 2015 24 NOVEMBRE CONFERENZA PARIGI 15 - 11 - 24 - NatixisConference - Final PDFPino CiampolilloNo ratings yet

- ITALCEMENTI 2015 24 NOVEMBRE CONFERENZA PARIGI 15 - 11 - 24 - NatixisConference - Final PDFDocument60 pagesITALCEMENTI 2015 24 NOVEMBRE CONFERENZA PARIGI 15 - 11 - 24 - NatixisConference - Final PDFPino CiampolilloNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Maximizing Profits from Water Refill StationsDocument4 pagesMaximizing Profits from Water Refill Stationsclaire nagaNo ratings yet

- Chapter 1: Fundamental Principles TaxationDocument2 pagesChapter 1: Fundamental Principles TaxationRogelio Olasos BernobaNo ratings yet

- CPA Review School of The Philippines Manila General Principles of Taxation Dela Cruz/De Vera/LlamadoDocument12 pagesCPA Review School of The Philippines Manila General Principles of Taxation Dela Cruz/De Vera/LlamadoEdma Glory MacadaagNo ratings yet

- Agreement Vehicle LoanDocument22 pagesAgreement Vehicle LoanSJ Geronimo0% (1)

- Maceda vs. MacaraigDocument2 pagesMaceda vs. MacaraigJoseph DimalantaNo ratings yet

- BUSTAX-REVIEWER (2)Document7 pagesBUSTAX-REVIEWER (2)Jeremy JimenezNo ratings yet

- Invoice Capture Center 7 5 Customizing Guide PDFDocument209 pagesInvoice Capture Center 7 5 Customizing Guide PDFifrahimNo ratings yet

- Everything You Need To Know About GST Goods and Services TaxDocument2 pagesEverything You Need To Know About GST Goods and Services TaxNagendra SinghNo ratings yet

- Pgp12038 A Chandana Landa DaDocument7 pagesPgp12038 A Chandana Landa DaChandana LandaNo ratings yet

- Samara University AssignmentDocument9 pagesSamara University AssignmentyaregalNo ratings yet

- 17 - Findings Conclusion and SuggestionDocument20 pages17 - Findings Conclusion and SuggestionAnkitha KavyaNo ratings yet

- MDDCore Lock FileDocument3 pagesMDDCore Lock FileShin LimNo ratings yet

- SPS-Avelino-v.-Celedonio 2Document7 pagesSPS-Avelino-v.-Celedonio 2Jorge M. GarciaNo ratings yet

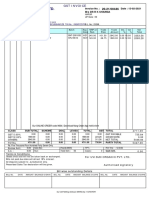

- PayslipsDocument63 pagesPayslipsPrem AahvaNo ratings yet

- Renewable Energy Act of 2008Document21 pagesRenewable Energy Act of 2008Shanielle Qim CañedaNo ratings yet

- Employment AgreementDocument4 pagesEmployment AgreementFreeza Masculino FabrigasNo ratings yet

- CIR vs. Avon, Inc., GR Nos. 201418-19, Oct. 3, 2018Document3 pagesCIR vs. Avon, Inc., GR Nos. 201418-19, Oct. 3, 2018Amity Rose RiveroNo ratings yet

- Social Security Cola Facts 2019Document2 pagesSocial Security Cola Facts 2019Jim KinneyNo ratings yet

- Ra 9049Document4 pagesRa 9049Nina L. Dela CruzNo ratings yet

- GST Invoice Organic PharmaDocument1 pageGST Invoice Organic PharmaVinay SharmaNo ratings yet

- Globalization's impact on Indian economyDocument9 pagesGlobalization's impact on Indian economySURAJ RAIKARNo ratings yet

- NESPAK Letter 12-14-2020-MergedDocument3 pagesNESPAK Letter 12-14-2020-MergedShakir MuhammadNo ratings yet

- Parliamentarians Tax Directory For Year Ended 30 June 2018Document22 pagesParliamentarians Tax Directory For Year Ended 30 June 2018Manzar Elahi Turk100% (1)

- Kazakhstan: National Fund of The Republic of KazakhstanDocument13 pagesKazakhstan: National Fund of The Republic of KazakhstanMirali HeydariNo ratings yet

- Mercantile Law and TaxationDocument9 pagesMercantile Law and TaxationJoe SolimanNo ratings yet

- BUSEGA DISTRICT COUNCIL FORM FOUR OPENING EXAMINATION MARKING SCHEME FOR HISTORYDocument4 pagesBUSEGA DISTRICT COUNCIL FORM FOUR OPENING EXAMINATION MARKING SCHEME FOR HISTORYwanga, issah omaryNo ratings yet

- Business Valuation GuideDocument13 pagesBusiness Valuation GuideSODDEYNo ratings yet

- Break Even Analysis For Investment PropertyDocument2 pagesBreak Even Analysis For Investment PropertyDebbieNo ratings yet

- FC BG SBLC Loi 41+2%Document28 pagesFC BG SBLC Loi 41+2%Lee Si HuiNo ratings yet

- C. Dekker, H. Soly, J. H. Van Stuijvenberg, A. Th. Van Deursen, M. Müller, E. Witte, P. W. Klein, Alice C. Carter (Auth.) Acta Historiae Neerlandicae 8 - Studies On The History of The NetherlandsDocument207 pagesC. Dekker, H. Soly, J. H. Van Stuijvenberg, A. Th. Van Deursen, M. Müller, E. Witte, P. W. Klein, Alice C. Carter (Auth.) Acta Historiae Neerlandicae 8 - Studies On The History of The NetherlandsKoen van den BosNo ratings yet