You might also like

- What is the Philippine Deposit Insurance Corporation (PDICDocument3 pagesWhat is the Philippine Deposit Insurance Corporation (PDICColleen Rose GuanteroNo ratings yet

- Salient Features of Philippine Deposit Insurance Corporation (PDIC) - Republic Act 3591Document6 pagesSalient Features of Philippine Deposit Insurance Corporation (PDIC) - Republic Act 3591Mycah AliahNo ratings yet

- Important Provisions under RA 9139 on Alien Spouses and ChildrenDocument2 pagesImportant Provisions under RA 9139 on Alien Spouses and ChildrenMyn Mirafuentes Sta Ana0% (1)

- China Banking Corporation vs. Lichauco Interest RatesDocument5 pagesChina Banking Corporation vs. Lichauco Interest RatesElaine CepedaNo ratings yet

- Banks Liable for Negligence in Client DepositsDocument2 pagesBanks Liable for Negligence in Client DepositsLuke VerdaderoNo ratings yet

- Commercial and Specialty Laws SyllabusDocument5 pagesCommercial and Specialty Laws SyllabusgianelleNo ratings yet

- When, What and How of Insurance Contract (Perfection) When Is It Perfected?Document9 pagesWhen, What and How of Insurance Contract (Perfection) When Is It Perfected?Jexelle Marteen Tumibay PestañoNo ratings yet

- Retainer AgreementsampleDocument2 pagesRetainer AgreementsampleJomik Lim EscarrillaNo ratings yet

- BBL 114 - Case Digests - Recto and Maceda LawDocument3 pagesBBL 114 - Case Digests - Recto and Maceda LawJaymert SamsonNo ratings yet

- Reviewer Nego Acceptance To ChecksDocument4 pagesReviewer Nego Acceptance To ChecksJohn MaquilingNo ratings yet

- From Atty. Deanabeth C. Gonzales, Professor Rizal Technological University, CBETDocument7 pagesFrom Atty. Deanabeth C. Gonzales, Professor Rizal Technological University, CBETAndrew Miguel SantosNo ratings yet

- Case DigestDocument24 pagesCase DigestVanessa May GaNo ratings yet

- 1984 Bar QsDocument14 pages1984 Bar QsSabritoNo ratings yet

- Acceleration Clause Effect on Note MaturityDocument1 pageAcceleration Clause Effect on Note Maturitykmand_lustregNo ratings yet

- 1990 Commercial Bar Exam - CatindigDocument6 pages1990 Commercial Bar Exam - CatindigmailguzmanNo ratings yet

- Ceniza Vs CaDocument6 pagesCeniza Vs Caseisuke_kanou100% (1)

- Insurance Syllabus With Laws RA 10607Document7 pagesInsurance Syllabus With Laws RA 10607Pring SumNo ratings yet

- Taguig City expands anti-smoking ordinanceDocument12 pagesTaguig City expands anti-smoking ordinanceJovelan V. EscañoNo ratings yet

- Bir V. Ca: GR. No. 197590, Nov. 24, 2014Document2 pagesBir V. Ca: GR. No. 197590, Nov. 24, 2014Jezreel Y. ChanNo ratings yet

- Tax Case Digest: People V. Mallari, G.R. No. 197164, December 4, 2019Document2 pagesTax Case Digest: People V. Mallari, G.R. No. 197164, December 4, 2019Dennis Vidad DupitasNo ratings yet

- Remedies of An Unpaid SellerDocument3 pagesRemedies of An Unpaid SellerSarah Hoddinott75% (4)

- Jacob vs. CA - 224 S 189Document2 pagesJacob vs. CA - 224 S 189Zesyl Avigail FranciscoNo ratings yet

- Frank V Kosuyama59 Phil 206Document2 pagesFrank V Kosuyama59 Phil 206Anonymous oDPxEkdNo ratings yet

- Defend RMC 12-2018Document4 pagesDefend RMC 12-2018John Evan Raymund BesidNo ratings yet

- MercmercDocument3 pagesMercmercFely DesembranaNo ratings yet

- Remedies of A Defending Party Declared in DefaultDocument1 pageRemedies of A Defending Party Declared in DefaultJan LorenzoNo ratings yet

- Taxation and Due Process Under the Philippine ConstitutionDocument15 pagesTaxation and Due Process Under the Philippine Constitutionkimberly milagNo ratings yet

- Implied Warranties and Eviction in Philippine Contract LawDocument3 pagesImplied Warranties and Eviction in Philippine Contract LawMarkNo ratings yet

- Credtrans Rem CDocument8 pagesCredtrans Rem CKarina Bette Ruiz100% (1)

- Spouses Manas V NicolasoraDocument9 pagesSpouses Manas V NicolasoraJaysonNo ratings yet

- Zenaida D. Mendoza vs. HMS Credit Corporation, Et AlDocument11 pagesZenaida D. Mendoza vs. HMS Credit Corporation, Et AljafernandNo ratings yet

- MWSS vs. Maynilad Water Contract DisputeDocument6 pagesMWSS vs. Maynilad Water Contract DisputejoNo ratings yet

- NATRESDocument6 pagesNATRESJude Ayochok MarquezNo ratings yet

- Development Bank of The Philippines v. Felipe ArcillaDocument17 pagesDevelopment Bank of The Philippines v. Felipe Arcillacyhaaangelaaa100% (1)

- Commissioner Vs Magsaysay LinesDocument2 pagesCommissioner Vs Magsaysay LinesVerlynMayThereseCaroNo ratings yet

- Allied Bank disputes unpaid loansDocument5 pagesAllied Bank disputes unpaid loansMarjorie FloresNo ratings yet

- Bar Exam Questions in Banking LawsDocument54 pagesBar Exam Questions in Banking LawsKayzer SabaNo ratings yet

- Incitti v. FerranteDocument1 pageIncitti v. FerranteJullianne Micaell CarlayNo ratings yet

- Rev Rem Case Digests Set 2 Cases 3 and 4Document3 pagesRev Rem Case Digests Set 2 Cases 3 and 4HNo ratings yet

- RCBCDocument2 pagesRCBCfradz08No ratings yet

- Interim Rules of Procedure On Corporate RehabilitationDocument11 pagesInterim Rules of Procedure On Corporate RehabilitationChrissy SabellaNo ratings yet

- 1-29 DigestDocument23 pages1-29 DigesttimothymaderazoNo ratings yet

- GR No. 176438Document2 pagesGR No. 176438Angelicka Jane Resurreccion50% (2)

- Rights and Duties of Partners NotesDocument3 pagesRights and Duties of Partners NotesLoveLyzaNo ratings yet

- Philippine Supreme Court upholds local restaurant's ownership of "Shangri-LaDocument16 pagesPhilippine Supreme Court upholds local restaurant's ownership of "Shangri-LaKarl Vhe Jhay ClaroNo ratings yet

- General Banking Act PDFDocument69 pagesGeneral Banking Act PDFJerwin TiamsonNo ratings yet

- Deed of SaleDocument9 pagesDeed of SaleAling KinaiNo ratings yet

- Trust Art. 1451-11457Document2 pagesTrust Art. 1451-11457Roji Belizar HernandezNo ratings yet

- Tax RemediesDocument7 pagesTax RemediesKyla Ellen CalelaoNo ratings yet

- GalvezDocument1 pageGalvezellaNo ratings yet

- Philippine Competition ActDocument31 pagesPhilippine Competition ActJam RxNo ratings yet

- G.R. No. 37467 Case DigestDocument3 pagesG.R. No. 37467 Case DigestsheilaNo ratings yet

- Philippine Collection CaseDocument3 pagesPhilippine Collection CaseLaika HernandezNo ratings yet

- Difference Commodatum v. MutuumDocument3 pagesDifference Commodatum v. MutuumAnjung Manuel CasibangNo ratings yet

- Multiple choice questions on negotiable instruments, contracts, corporations and partnershipsDocument11 pagesMultiple choice questions on negotiable instruments, contracts, corporations and partnershipsJinx Cyrus RodilloNo ratings yet

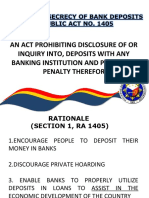

- The Law On Secrecy of Bank DepositsDocument17 pagesThe Law On Secrecy of Bank DepositsMakoy BixenmanNo ratings yet

- Ejercito vs. Sandiganbayan and People of The Philippines, 509 SCRA 190Document12 pagesEjercito vs. Sandiganbayan and People of The Philippines, 509 SCRA 190samantha oxfordNo ratings yet

- Speccom-Exam - (Pilacan, Karyl Vic) PDFDocument8 pagesSpeccom-Exam - (Pilacan, Karyl Vic) PDFPilacan KarylNo ratings yet

- What Is The Philippine Deposit Insurance Corporation (PDIC) ?Document7 pagesWhat Is The Philippine Deposit Insurance Corporation (PDIC) ?Jo Vic Cata BonaNo ratings yet

- What is the Philippine Deposit Insurance Corporation (PDICDocument5 pagesWhat is the Philippine Deposit Insurance Corporation (PDICMarlon EspedillonNo ratings yet

- Program TArpaulinDocument1 pageProgram TArpaulinChristianHarveyWongNo ratings yet

- Farmers Coop List of Requirement For AcefDocument1 pageFarmers Coop List of Requirement For AcefChristianHarveyWongNo ratings yet

- Landbank of The Philippines: Documentary Stamp TaxDocument1 pageLandbank of The Philippines: Documentary Stamp TaxChristianHarveyWongNo ratings yet

- Sure Aid Cash Card Distribution: ProgrammeDocument1 pageSure Aid Cash Card Distribution: ProgrammeChristianHarveyWongNo ratings yet

- Case Digest - June 17Document14 pagesCase Digest - June 17ChristianHarveyWong100% (1)

- Lending Center No. of Attendees Provinces Covered Provinces Covered2 No. of Farmers' Forum (July - Sept 2019) No. of Farmers' Forum (Oct-Dec 2019)Document2 pagesLending Center No. of Attendees Provinces Covered Provinces Covered2 No. of Farmers' Forum (July - Sept 2019) No. of Farmers' Forum (Oct-Dec 2019)ChristianHarveyWongNo ratings yet

- Waer & QuitclaimDocument1 pageWaer & QuitclaimChristianHarveyWongNo ratings yet

- Plan and BudgetDocument1 pagePlan and BudgetChristianHarveyWongNo ratings yet

- Municipality & Province: Matanao SURE Aid Form #2: Validated List Landbank Lending CenterDocument2 pagesMunicipality & Province: Matanao SURE Aid Form #2: Validated List Landbank Lending CenterChristianHarveyWongNo ratings yet

- Gift Tag-Excel 2019Document19 pagesGift Tag-Excel 2019ChristianHarveyWongNo ratings yet

- Total Loans As To Security As of June 30, 2019Document4 pagesTotal Loans As To Security As of June 30, 2019ChristianHarveyWongNo ratings yet

- Forward: (Sec. 5, Rule 7, 1997 Rules of Civil Procedure)Document2 pagesForward: (Sec. 5, Rule 7, 1997 Rules of Civil Procedure)ChristianHarveyWongNo ratings yet

- List of Growers Name of Lender: Name of Group: AddressDocument2 pagesList of Growers Name of Lender: Name of Group: AddressChristianHarveyWongNo ratings yet

- Leases 20Document184 pagesLeases 20ChristianHarveyWongNo ratings yet

- Appeal From LBP MindanaoansDocument1 pageAppeal From LBP MindanaoansChristianHarveyWongNo ratings yet

- CS Form No. 212 Attachment - Work Experience SheetDocument1 pageCS Form No. 212 Attachment - Work Experience SheetChristianHarveyWongNo ratings yet

- Jurisdiction Evidence: (Sec. 3 (E), Rule 9) (Sec. 16 of Rule 3)Document2 pagesJurisdiction Evidence: (Sec. 3 (E), Rule 9) (Sec. 16 of Rule 3)ChristianHarveyWongNo ratings yet

- Annex B For Bir RequirementDocument1 pageAnnex B For Bir RequirementAnonymous iScW9lNo ratings yet

- Civpotr 206aDocument17 pagesCivpotr 206aChristianHarveyWongNo ratings yet

- CIV PRO BAR 206aDocument19 pagesCIV PRO BAR 206aChristianHarveyWongNo ratings yet

- Suggested Answers 19 342342432432Document2 pagesSuggested Answers 19 342342432432ChristianHarveyWongNo ratings yet

- General Principles: (Sec. 3 (E), Rule 9)Document2 pagesGeneral Principles: (Sec. 3 (E), Rule 9)ChristianHarveyWongNo ratings yet

- General Principles: (Sec. 3 (E), Rule 9) (Sec. 16 of Rule 3)Document2 pagesGeneral Principles: (Sec. 3 (E), Rule 9) (Sec. 16 of Rule 3)ChristianHarveyWongNo ratings yet

- No PDF File AvailableDocument1 pageNo PDF File AvailableChristianHarveyWongNo ratings yet

- Case Assign SC 2016 2020Document5 pagesCase Assign SC 2016 2020ChristianHarveyWongNo ratings yet

- Cryllic Barrier 2Document1 pageCryllic Barrier 2ChristianHarveyWongNo ratings yet

- Emergency Genset Repair Approval RequestDocument2 pagesEmergency Genset Repair Approval RequestChristianHarveyWongNo ratings yet

- Motorcade Registration & Blessing Opening ThanksgivingDocument2 pagesMotorcade Registration & Blessing Opening ThanksgivingChristianHarveyWongNo ratings yet

- LBP Kidapawan Branch Installs Protective BarriersDocument5 pagesLBP Kidapawan Branch Installs Protective BarriersChristianHarveyWongNo ratings yet

- CIVIL SERVICE COMMISSION 2005 Amended RulesDocument25 pagesCIVIL SERVICE COMMISSION 2005 Amended RulesKim Roque-Aquino100% (1)

- Income Tax CalculatorDocument5 pagesIncome Tax CalculatorTanmay DeshpandeNo ratings yet

- Multinational Capital BudgetingDocument20 pagesMultinational Capital BudgetingBibiNo ratings yet

- Risk Identification and Mitigation StrategiesDocument5 pagesRisk Identification and Mitigation StrategiesnishthaNo ratings yet

- New Income Tax Law 2018.1 NewDocument87 pagesNew Income Tax Law 2018.1 NewDamascene100% (1)

- Financial Times Europe - 25.11.2020Document20 pagesFinancial Times Europe - 25.11.2020Muhammad AroojNo ratings yet

- SECP Form 6Document4 pagesSECP Form 6mirza faisalNo ratings yet

- A Project Report On TaxationDocument71 pagesA Project Report On TaxationHveeeeNo ratings yet

- Ch25 Insurance OperationsDocument42 pagesCh25 Insurance OperationsTHIVIYATHINI PERUMALNo ratings yet

- Activities FXDocument5 pagesActivities FXWaqar KhalidNo ratings yet

- Chapter - 9: General Financial Rules 2017Document40 pagesChapter - 9: General Financial Rules 2017PatrickNo ratings yet

- Dissolution and Incorporation of a PartnershipDocument26 pagesDissolution and Incorporation of a PartnershipJohn LouiseNo ratings yet

- Total Compensation Framework Template (Annex A)Document2 pagesTotal Compensation Framework Template (Annex A)Noreen Boots Gocon-GragasinNo ratings yet

- Articles of IncorporationDocument4 pagesArticles of IncorporationRuel FernandezNo ratings yet

- Solved Copy The Mike Owjai Manufacturing Financial Statements From Problem 1Document1 pageSolved Copy The Mike Owjai Manufacturing Financial Statements From Problem 1DoreenNo ratings yet

- C11 Principles and Practice of InsuranceDocument9 pagesC11 Principles and Practice of InsuranceAnonymous y3E7ia100% (2)

- Audit Module 3 - Financial Statements TemplateDocument11 pagesAudit Module 3 - Financial Statements TemplateSiddhant AggarwalNo ratings yet

- FM by Sir KarimDocument2 pagesFM by Sir KarimWeng CagapeNo ratings yet

- 4th Quarter Entrepreneurship FinalsDocument3 pages4th Quarter Entrepreneurship FinalsShen EugenioNo ratings yet

- ZF-02 Posting Credit Note SPPLDocument10 pagesZF-02 Posting Credit Note SPPLGhosh2No ratings yet

- Retail IndustryDocument3 pagesRetail IndustryakavinashkillerNo ratings yet

- Form 2106Document2 pagesForm 2106Weiming LinNo ratings yet

- Preqin Latin America Report 2021Document35 pagesPreqin Latin America Report 2021Carlos ArangoNo ratings yet

- Chapter 13 In-Class Exercise Set SolutionsDocument10 pagesChapter 13 In-Class Exercise Set SolutionsJudith Garcia0% (1)

- COMPARISON OF TAKAFUL AND INSURANCEDocument9 pagesCOMPARISON OF TAKAFUL AND INSURANCEHusna FadzilNo ratings yet

- Anand RathiDocument3 pagesAnand RathiShilpa EdarNo ratings yet

- IVALIFE - IVApension Policy BookletDocument12 pagesIVALIFE - IVApension Policy BookletJosef BaldacchinoNo ratings yet

- Sap Central Finance in Sap S4hanaDocument5 pagesSap Central Finance in Sap S4hanaHoNo ratings yet

- Advanced Accounting Chapter 5Document21 pagesAdvanced Accounting Chapter 5leelee030275% (4)

- A Case For Economic Democracy by Gary Dorrien - Tikkun Magazine PDFDocument7 pagesA Case For Economic Democracy by Gary Dorrien - Tikkun Magazine PDFMegan Jane JohnsonNo ratings yet

- Renewal Premium Receipt - 00755988Document1 pageRenewal Premium Receipt - 00755988Tarun KushwahaNo ratings yet

- Angel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000From EverandAngel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000Rating: 4.5 out of 5 stars4.5/5 (86)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingFrom EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingRating: 4.5 out of 5 stars4.5/5 (97)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorFrom EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorRating: 4.5 out of 5 stars4.5/5 (63)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorFrom EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorRating: 4.5 out of 5 stars4.5/5 (132)

- Add Then Multiply: How small businesses can think like big businesses and achieve exponential growthFrom EverandAdd Then Multiply: How small businesses can think like big businesses and achieve exponential growthNo ratings yet

- Disloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpFrom EverandDisloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpRating: 4 out of 5 stars4/5 (214)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- The Business Legal Lifecycle US Edition: How To Successfully Navigate Your Way From Start Up To SuccessFrom EverandThe Business Legal Lifecycle US Edition: How To Successfully Navigate Your Way From Start Up To SuccessNo ratings yet

- The Complete Book of Wills, Estates & Trusts (4th Edition): Advice That Can Save You Thousands of Dollars in Legal Fees and TaxesFrom EverandThe Complete Book of Wills, Estates & Trusts (4th Edition): Advice That Can Save You Thousands of Dollars in Legal Fees and TaxesRating: 4 out of 5 stars4/5 (1)