You might also like

- Exercises Budgeting ACCT2105 3s2010Document7 pagesExercises Budgeting ACCT2105 3s2010Hanh Bui0% (1)

- Prepare A Cash Budget - by Quarter and in Total ... - GlobalExperts4UDocument31 pagesPrepare A Cash Budget - by Quarter and in Total ... - GlobalExperts4USaiful IslamNo ratings yet

- Cash BudgetingDocument14 pagesCash BudgetingJo Ryl100% (1)

- Capital Budgeting NPV Case Study: Retail Fashion StoreDocument2 pagesCapital Budgeting NPV Case Study: Retail Fashion StoreAnand Prakash Sharma100% (1)

- Arias, Kyla Kim B. - Midterm Project Sept 30Document9 pagesArias, Kyla Kim B. - Midterm Project Sept 30Kyla Kim AriasNo ratings yet

- Forecasting Probs Solns s07Document4 pagesForecasting Probs Solns s07nsrmurthy63No ratings yet

- Cash Budget Sums Mcom Sem 4Document14 pagesCash Budget Sums Mcom Sem 4Prachi BhosaleNo ratings yet

- Managerial Economics - A Decision Science andDocument5 pagesManagerial Economics - A Decision Science andSam NietNo ratings yet

- Cost of CapitalDocument30 pagesCost of CapitalNirmal ShresthaNo ratings yet

- Cost Accounting de Leon Chapter 3 SolutionsDocument9 pagesCost Accounting de Leon Chapter 3 SolutionsRichelle SangatananNo ratings yet

- Chapter Three CVP AnalysisDocument65 pagesChapter Three CVP AnalysisBettyNo ratings yet

- Review Myron Corporation's seasonal product sales budget and production requirementsDocument8 pagesReview Myron Corporation's seasonal product sales budget and production requirementsmohammad bilalNo ratings yet

- Review of AccountingDocument31 pagesReview of AccountingDylan LoweNo ratings yet

- Workshop F2 May 2011Document18 pagesWorkshop F2 May 2011roukaiya_peerkhanNo ratings yet

- Cash Budgets Practice QuestionDocument1 pageCash Budgets Practice QuestionDenisa M. Todea50% (2)

- CH 13#6Document13 pagesCH 13#6jjmaducdoc100% (1)

- Multiple Choice: Chapter 16 - SolvingDocument19 pagesMultiple Choice: Chapter 16 - SolvingElla LopezNo ratings yet

- Sommer Graphics Company Was Organized On January 1 2015 byDocument1 pageSommer Graphics Company Was Organized On January 1 2015 byAmit PandeyNo ratings yet

- Chapter 3Document30 pagesChapter 3Varun ChauhanNo ratings yet

- Module 3 Introduction To AnnuitiesDocument17 pagesModule 3 Introduction To AnnuitiesJenny AltazarNo ratings yet

- MasterDocument10 pagesMasterNour Sawafta0% (1)

- Final Requirment (Case Study)Document2 pagesFinal Requirment (Case Study)Gerry SajolNo ratings yet

- Brief Exercises For EPSDocument4 pagesBrief Exercises For EPSanon_225460591No ratings yet

- McDowell Industries Receivables AnalysisDocument8 pagesMcDowell Industries Receivables AnalysisTABUADA, Jenny Rose V.No ratings yet

- Chapter 5 - Cost EstimationDocument36 pagesChapter 5 - Cost Estimationalleyezonmii0% (2)

- ACCT-312:: Exercises For Home Study (From Chapter 6)Document5 pagesACCT-312:: Exercises For Home Study (From Chapter 6)Amir ContrerasNo ratings yet

- Ratio AnalysisDocument4 pagesRatio AnalysisPrecious Vercaza Del Rosario100% (1)

- Preparation of Financial StatementsDocument3 pagesPreparation of Financial StatementsMarc Eric Redondo0% (1)

- Financial Reporting and Analysis Case Study-2Document3 pagesFinancial Reporting and Analysis Case Study-2bourne0% (2)

- Cost AccountingDocument14 pagesCost AccountingAdv Kamran Liaqat50% (2)

- LKAS 02 & LKAS 16 DiscussionDocument2 pagesLKAS 02 & LKAS 16 DiscussionKogularamanan NithiananthanNo ratings yet

- 4299259Document7 pages4299259mohitgaba19No ratings yet

- Bell ComputersDocument3 pagesBell ComputersShameem Khaled0% (1)

- Case 8-31: April May June QuarterDocument2 pagesCase 8-31: April May June QuarterileviejoieNo ratings yet

- Intermediate Accounting Exam 2 ReviewDocument1 pageIntermediate Accounting Exam 2 ReviewBLACKPINKLisaRoseJisooJennieNo ratings yet

- Activity No 1Document2 pagesActivity No 1Makeyc Stis100% (1)

- Economic Systems and Their Impact on International BusinessDocument8 pagesEconomic Systems and Their Impact on International BusinessKhalid AminNo ratings yet

- Week 13 SolutionsDocument7 pagesWeek 13 SolutionsStanley RobertNo ratings yet

- Assignment-2 CmaDocument8 pagesAssignment-2 CmaAYESHA BOITAINo ratings yet

- Financial Management Test 2: Answer ALL QuestionsDocument3 pagesFinancial Management Test 2: Answer ALL Questionshemavathy50% (2)

- Cash Flows, Financial Planning and BudgetingDocument34 pagesCash Flows, Financial Planning and BudgetingKarl LuzungNo ratings yet

- PDFDocument114 pagesPDFMusa A. Hassan100% (1)

- Chapter 2-Multi-Product CVP AnalysisDocument53 pagesChapter 2-Multi-Product CVP AnalysisAyeNo ratings yet

- FULL DISCLOSURE Test BankDocument11 pagesFULL DISCLOSURE Test Bankzee abadillaNo ratings yet

- Statement of Cost of Goods SoldDocument3 pagesStatement of Cost of Goods SoldMARIA67% (3)

- Module 3 - Capital BudgetingDocument1 pageModule 3 - Capital BudgetingPrincess Frean VillegasNo ratings yet

- Management Accounting (Workbook) PDFDocument85 pagesManagement Accounting (Workbook) PDFRizza azilia kNo ratings yet

- Practice Problems For Managing InventoryDocument7 pagesPractice Problems For Managing InventoryKholoudBenSaidNo ratings yet

- Great Zimbabwe University Faculty of CommerceDocument6 pagesGreat Zimbabwe University Faculty of CommerceTawanda Tatenda HerbertNo ratings yet

- 6 BudgetingDocument2 pages6 BudgetingClyette Anne Flores BorjaNo ratings yet

- Budgets Exercises StudentDocument5 pagesBudgets Exercises Studentديـنـا عادل0% (1)

- Cash Budget Problem 1. Mercury Shoes IncDocument7 pagesCash Budget Problem 1. Mercury Shoes IncMaritess Munoz100% (1)

- Cash BudgetDocument4 pagesCash BudgetSANDEEP SINGH0% (1)

- Cash Budgeting QuestionsDocument5 pagesCash Budgeting QuestionsAnissa GeddesNo ratings yet

- AccountingDocument14 pagesAccountingDavid DavidNo ratings yet

- Cash Budgeting TutorialDocument4 pagesCash Budgeting Tutorialmichellebaileylindsa100% (1)

- BudgetingDocument9 pagesBudgetingshobi_300033% (3)

- Master Budget for Intermediate, IncDocument12 pagesMaster Budget for Intermediate, IncBekama Abdii Koo TesfayeNo ratings yet

- As A Preliminary To Requesting Budget Estimates of SalesDocument4 pagesAs A Preliminary To Requesting Budget Estimates of SalesChiodos OliverNo ratings yet

- Asignación 4 LSFPDocument3 pagesAsignación 4 LSFPElia SantanaNo ratings yet

- The Bullwhip Effect in HPs Supply ChainDocument9 pagesThe Bullwhip Effect in HPs Supply Chainsoulhudson100% (1)

- 10 AxiomsDocument6 pages10 AxiomsJann KerkyNo ratings yet

- Guidelines of Martial LawDocument16 pagesGuidelines of Martial LawJann KerkyNo ratings yet

- Food Safety and Hygiene LayoutDocument9 pagesFood Safety and Hygiene LayoutJann Kerky100% (1)

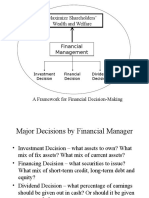

- Maximize Shareholders' Wealth and Welfare: Investment Decision Financial Decision Dividend DecisionDocument6 pagesMaximize Shareholders' Wealth and Welfare: Investment Decision Financial Decision Dividend DecisionJann KerkyNo ratings yet

- Analyze Capital Structure Using EBIT-EPS AnalysisDocument3 pagesAnalyze Capital Structure Using EBIT-EPS AnalysisJann KerkyNo ratings yet

- KFC Philippines Shaw Branch delivery service process case studyDocument2 pagesKFC Philippines Shaw Branch delivery service process case studyJann KerkyNo ratings yet

- Define premium peanuts with SFPC instructionsDocument2 pagesDefine premium peanuts with SFPC instructionsJann KerkyNo ratings yet

- Precision Delivery Inc. Case StudyDocument2 pagesPrecision Delivery Inc. Case StudyJann Kerky0% (1)

- Analysis of Financial StatementsDocument20 pagesAnalysis of Financial StatementsJann KerkyNo ratings yet

- Chapter 2: Atomic Structure & Interatomic Bonding: Issues To Address..Document36 pagesChapter 2: Atomic Structure & Interatomic Bonding: Issues To Address..putriyusairah_91No ratings yet

- Unsecured Short-Term Financing OptionsDocument5 pagesUnsecured Short-Term Financing OptionsJann KerkyNo ratings yet

- Horizontal and Vertical Analysis DetailsDocument9 pagesHorizontal and Vertical Analysis DetailsJann KerkyNo ratings yet

- Chapter 2: Atomic Structure & Interatomic Bonding: Issues To Address..Document36 pagesChapter 2: Atomic Structure & Interatomic Bonding: Issues To Address..putriyusairah_91No ratings yet

- The GoalDocument3 pagesThe GoalJann KerkyNo ratings yet

- The Tragic MythDocument4 pagesThe Tragic MythJann KerkyNo ratings yet

- Analysis of Financial Statements: Answers To End-Of-Chapter QuestionsDocument15 pagesAnalysis of Financial Statements: Answers To End-Of-Chapter QuestionsAditya R HimawanNo ratings yet

- Problems and SolutionsDocument31 pagesProblems and SolutionsJann KerkyNo ratings yet

- Telfer - Food As ArtDocument10 pagesTelfer - Food As ArtJann Kerky100% (1)

- Energy TransformationDocument6 pagesEnergy TransformationJann KerkyNo ratings yet

- Sample FinalDocument9 pagesSample FinalJann KerkyNo ratings yet

- All-New Accord Luxury SedanDocument25 pagesAll-New Accord Luxury SedanJann KerkyNo ratings yet

- Conplast SP430 0407Document4 pagesConplast SP430 0407Harz IndNo ratings yet

- BRD TemplateDocument4 pagesBRD TemplateTrang Nguyen0% (1)

- Group 4 HR201 Last Case StudyDocument3 pagesGroup 4 HR201 Last Case StudyMatt Tejada100% (2)

- CadLink Flyer 369044 937 Rev 00Document2 pagesCadLink Flyer 369044 937 Rev 00ShanaHNo ratings yet

- International Convention Center, BanesworDocument18 pagesInternational Convention Center, BanesworSreeniketh ChikuNo ratings yet

- Gerhard Budin PublicationsDocument11 pagesGerhard Budin Publicationshnbc010No ratings yet

- KSRTC BokingDocument2 pagesKSRTC BokingyogeshNo ratings yet

- Server LogDocument5 pagesServer LogVlad CiubotariuNo ratings yet

- Weibull Statistic and Growth Analysis in Failure PredictionsDocument9 pagesWeibull Statistic and Growth Analysis in Failure PredictionsgmitsutaNo ratings yet

- Aci 207.1Document38 pagesAci 207.1safak kahraman100% (7)

- Make a Battery Level Indicator using LM339 ICDocument13 pagesMake a Battery Level Indicator using LM339 ICnelson100% (1)

- Tech Letter-NFPA 54 To Include Bonding 8-08Document2 pagesTech Letter-NFPA 54 To Include Bonding 8-08gl lugaNo ratings yet

- EPS Lab ManualDocument7 pagesEPS Lab ManualJeremy Hensley100% (1)

- Unit 1 2marksDocument5 pagesUnit 1 2marksLokesh SrmNo ratings yet

- Chapter 6: Structured Query Language (SQL) : Customer Custid Custname OccupationDocument16 pagesChapter 6: Structured Query Language (SQL) : Customer Custid Custname OccupationSarmila MahendranNo ratings yet

- SD Electrolux LT 4 Partisi 21082023Document3 pagesSD Electrolux LT 4 Partisi 21082023hanifahNo ratings yet

- Single Wall Fuel Tank: FP 2.7 A-C Fire Pump SystemsDocument1 pageSingle Wall Fuel Tank: FP 2.7 A-C Fire Pump Systemsricardo cardosoNo ratings yet

- GS Ep Cor 356Document7 pagesGS Ep Cor 356SangaranNo ratings yet

- ASME Y14.6-2001 (R2007), Screw Thread RepresentationDocument27 pagesASME Y14.6-2001 (R2007), Screw Thread RepresentationDerekNo ratings yet

- Distribution of Laptop (Ha-Meem Textiles Zone)Document3 pagesDistribution of Laptop (Ha-Meem Textiles Zone)Begum Nazmun Nahar Juthi MozumderNo ratings yet

- 7th Kannada Science 01Document160 pages7th Kannada Science 01Edit O Pics StatusNo ratings yet

- Account STMT XX0226 19122023Document13 pagesAccount STMT XX0226 19122023rdineshyNo ratings yet

- As 1769-1975 Welded Stainless Steel Tubes For Plumbing ApplicationsDocument6 pagesAs 1769-1975 Welded Stainless Steel Tubes For Plumbing ApplicationsSAI Global - APACNo ratings yet

- Gattu Madhuri's Resume for ECE GraduateDocument4 pagesGattu Madhuri's Resume for ECE Graduatedeepakk_alpineNo ratings yet

- Case Study 2 F3005Document12 pagesCase Study 2 F3005Iqmal DaniealNo ratings yet

- Proposed Delivery For PAU/AHU Method Statement SEC/MS/3-25Document4 pagesProposed Delivery For PAU/AHU Method Statement SEC/MS/3-25Zin Ko NaingNo ratings yet

- Banas Dairy ETP Training ReportDocument38 pagesBanas Dairy ETP Training ReportEagle eye0% (2)

- 3838 Chandra Dev Gurung BSBADM502 Assessment 2 ProjectDocument13 pages3838 Chandra Dev Gurung BSBADM502 Assessment 2 Projectxadow sahNo ratings yet

- Death Without A SuccessorDocument2 pagesDeath Without A Successorilmanman16No ratings yet

- Question Paper Code: 31364Document3 pagesQuestion Paper Code: 31364vinovictory8571No ratings yet