You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

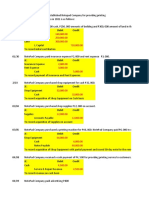

- Chapter-2 Solution For 27 and 28Document6 pagesChapter-2 Solution For 27 and 28Tarif IslamNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Worksheet Data For Savaglia Company Are Presented Below. The Owner Did Not Make Any Additional Investments in The Business in April.Document6 pagesWorksheet Data For Savaglia Company Are Presented Below. The Owner Did Not Make Any Additional Investments in The Business in April.Risky FernandoNo ratings yet

- SM Chapter 04Document135 pagesSM Chapter 04mas aziz100% (1)

- Polar Sports X Ls StudentDocument9 pagesPolar Sports X Ls StudentBilal Ahmed Shaikh0% (1)

- Unit 3 Key QuestionsDocument6 pagesUnit 3 Key QuestionsGabriel Kym Gichuhi100% (1)

- Unit 4 Key QuestionsDocument5 pagesUnit 4 Key QuestionsGabriel Kym GichuhiNo ratings yet

- Unit 2 Key QuestionsDocument4 pagesUnit 2 Key QuestionsGabriel Kym GichuhiNo ratings yet

- Unit 1 Key QuestionsDocument5 pagesUnit 1 Key QuestionsGabriel Kym GichuhiNo ratings yet

- Unit 4 Key QuestionsDocument7 pagesUnit 4 Key QuestionsGabriel Kym GichuhiNo ratings yet

- Unit 2 Key QuestionsDocument13 pagesUnit 2 Key QuestionsGabriel Kym GichuhiNo ratings yet

- Unit 1 Key QuestionsDocument5 pagesUnit 1 Key QuestionsGabriel Kym GichuhiNo ratings yet

- Unit 1 Key QuestionsDocument3 pagesUnit 1 Key QuestionsGabriel Kym GichuhiNo ratings yet

- Ultimate Financial ModelDocument33 pagesUltimate Financial ModelTulay Farra100% (1)

- IFRS6Document12 pagesIFRS6UEL Accounting & AuditingNo ratings yet

- Financial Reporting and Analysis: - Session 4-Professor Raluca Ratiu, PHDDocument54 pagesFinancial Reporting and Analysis: - Session 4-Professor Raluca Ratiu, PHDDaniel YebraNo ratings yet

- CH 3Document10 pagesCH 3Mohammed mostafaNo ratings yet

- 03 - Handout - Partnership DissolutionDocument4 pages03 - Handout - Partnership DissolutionJanysse CalderonNo ratings yet

- Baitap C1 HVDocument8 pagesBaitap C1 HVThanh ThảoNo ratings yet

- Standalone Financial Results For September 30, 2016 (Result)Document4 pagesStandalone Financial Results For September 30, 2016 (Result)Shyam SunderNo ratings yet

- Account Classification and PresentationDocument8 pagesAccount Classification and Presentationariane100% (1)

- Q1 WK 2 To 3 Las Fabm2 Kate DionisioDocument8 pagesQ1 WK 2 To 3 Las Fabm2 Kate DionisioFunji BuhatNo ratings yet

- 1 Daftar AkunDocument2 pages1 Daftar Akunnazwa utami27No ratings yet

- Practical Accounting 2.4Document13 pagesPractical Accounting 2.4rozele dNo ratings yet

- Wew PDFDocument9 pagesWew PDFLance L. OrlinoNo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument8 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionMary Grace Errabo FloridoNo ratings yet

- FA LQ 5. BonusDocument12 pagesFA LQ 5. BonusTrisha Valero FerolinoNo ratings yet

- Soal UTS SMT 1 AkP (12-10-21)Document22 pagesSoal UTS SMT 1 AkP (12-10-21)Bayu PrasetyoNo ratings yet

- Comprehensive Problem-Analysis of TransactionDocument43 pagesComprehensive Problem-Analysis of TransactionJoanna DandasanNo ratings yet

- Dates Transactions Balance Sheet, July 2014. AssetsDocument12 pagesDates Transactions Balance Sheet, July 2014. AssetsMille DcnyNo ratings yet

- IAS 38 Intangible For PresentDocument20 pagesIAS 38 Intangible For Presentnati100% (2)

- Oracle IFRS Solution ERP FinalDocument44 pagesOracle IFRS Solution ERP FinalJai SoniNo ratings yet

- L8. IFRS 7 - Financial InstrumentsDocument5 pagesL8. IFRS 7 - Financial InstrumentsAhmed HussainNo ratings yet

- Activity 2 - Transaction Analysis (FLORES)Document4 pagesActivity 2 - Transaction Analysis (FLORES)angela floresNo ratings yet

- Journal, Ledger, Trail Balance and Finnancial Statement MCQsDocument5 pagesJournal, Ledger, Trail Balance and Finnancial Statement MCQsNoshair Ali100% (4)

- IAS 1 - Presentation of Financial StatementsDocument17 pagesIAS 1 - Presentation of Financial StatementsMạnh hưng LêNo ratings yet

- Larsen Modern Advanced Accounting TenthDocument43 pagesLarsen Modern Advanced Accounting TenthNoura OmaarNo ratings yet

- Rothschild Annual Report 2007 - 08 - FinalDocument61 pagesRothschild Annual Report 2007 - 08 - FinalellokosNo ratings yet

- Isg Ifrs Us Gaap 2022Document593 pagesIsg Ifrs Us Gaap 2022Zain Naqvi50% (2)