You might also like

- How To Apply For A Homestead ExemptionDocument6 pagesHow To Apply For A Homestead ExemptionO'Connor AssociateNo ratings yet

- Why O'Connor For Property Tax Reduction?Document7 pagesWhy O'Connor For Property Tax Reduction?O'Connor AssociateNo ratings yet

- PRESENTATION - ERE - Tactics For Investors To Drive ROIDocument7 pagesPRESENTATION - ERE - Tactics For Investors To Drive ROIO'Connor AssociateNo ratings yet

- 3 Ways To Reduce Your Commercial Property Taxes With Cost SegregationDocument7 pages3 Ways To Reduce Your Commercial Property Taxes With Cost SegregationO'Connor AssociateNo ratings yet

- Wisconsin Municipal AssessorsDocument48 pagesWisconsin Municipal AssessorsO'Connor AssociateNo ratings yet

- House Flipping - A New Way of IncomeDocument6 pagesHouse Flipping - A New Way of IncomeO'Connor AssociateNo ratings yet

- Steps To Protest in Harris CountyDocument7 pagesSteps To Protest in Harris CountyO'Connor AssociateNo ratings yet

- PRESENTATION - OCA - The Thinning Line of Rental Collection in April - 2020Document6 pagesPRESENTATION - OCA - The Thinning Line of Rental Collection in April - 2020O'Connor AssociateNo ratings yet

- The IRS Guidelines For Non-Load Bearing WallsDocument5 pagesThe IRS Guidelines For Non-Load Bearing WallsO'Connor AssociateNo ratings yet

- How Can Cost Segregation Help Minimize Your Tax BurdenDocument6 pagesHow Can Cost Segregation Help Minimize Your Tax BurdenO'Connor AssociateNo ratings yet

- Top 3 Methods of Valuing Personal PropertyDocument7 pagesTop 3 Methods of Valuing Personal PropertyO'Connor AssociateNo ratings yet

- Tax Benefits For Home OwnersDocument7 pagesTax Benefits For Home OwnersO'Connor AssociateNo ratings yet

- Texas Real Estate InspectorDocument25 pagesTexas Real Estate InspectorO'Connor AssociateNo ratings yet

- Hcad Business Personal Property FaqDocument2 pagesHcad Business Personal Property FaqO'Connor AssociateNo ratings yet

- 25+ Reasons You SHOULD Protest Your HIGH PROPERTY TAXESDocument8 pages25+ Reasons You SHOULD Protest Your HIGH PROPERTY TAXESO'Connor AssociateNo ratings yet

- Williamson Cad 2017 Rendition General InformationDocument2 pagesWilliamson Cad 2017 Rendition General InformationO'Connor AssociateNo ratings yet

- Hcad Business Personal Property FaqDocument2 pagesHcad Business Personal Property FaqO'Connor AssociateNo ratings yet

- Cap Rate Rate ReportDocument207 pagesCap Rate Rate ReportO'Connor Associate0% (1)

- Dallascad - Propertytaxoverview2017Document30 pagesDallascad - Propertytaxoverview2017O'Connor AssociateNo ratings yet

- Tax DeferralDocument1 pageTax DeferralO'Connor AssociateNo ratings yet

- Commercial Real Estate International Business TrendsDocument21 pagesCommercial Real Estate International Business TrendsNational Association of REALTORS®100% (2)

- Property Assessment Appeal To The County Board of EqualizationDocument4 pagesProperty Assessment Appeal To The County Board of EqualizationO'Connor AssociateNo ratings yet

- GeorgiaCertificationProgram2017 2018Document2 pagesGeorgiaCertificationProgram2017 2018O'Connor AssociateNo ratings yet

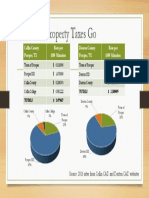

- Where The Property Taxes GoDocument1 pageWhere The Property Taxes GoO'Connor AssociateNo ratings yet

- Lincoln Institute of Land Policy's Comparison of 2016 Property TaxesDocument108 pagesLincoln Institute of Land Policy's Comparison of 2016 Property TaxescrainsnewyorkNo ratings yet

- 2016 Annual Report TravisCADDocument41 pages2016 Annual Report TravisCADO'Connor AssociateNo ratings yet

- Austin Property Taxpayer Remedies 2017Document1 pageAustin Property Taxpayer Remedies 2017O'Connor AssociateNo ratings yet

- W C A D: Ise Ounty Ppraisal IstrictDocument43 pagesW C A D: Ise Ounty Ppraisal IstrictO'Connor AssociateNo ratings yet

- Dallas Central Appraisal District 2017 2018Document30 pagesDallas Central Appraisal District 2017 2018O'Connor AssociateNo ratings yet

- Montgomery County Exemption AnalysisDocument19 pagesMontgomery County Exemption AnalysisO'Connor AssociateNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- M I Ngày M T Trò Chơi PDFDocument354 pagesM I Ngày M T Trò Chơi PDFkaka_02468100% (1)

- An Approach to Defining the Basic Premises of Public AdministrationDocument15 pagesAn Approach to Defining the Basic Premises of Public AdministrationAlvaro CamargoNo ratings yet

- HPLC Method for Simultaneous Determination of DrugsDocument7 pagesHPLC Method for Simultaneous Determination of DrugsWidya Dwi Arini100% (1)

- IFIC Bank Share Price FluctuationDocument7 pagesIFIC Bank Share Price FluctuationMakid HasanNo ratings yet

- The Philosophy of EmoDocument2 pagesThe Philosophy of EmoTed RichardsNo ratings yet

- Georgethirdearlo 00 WilluoftDocument396 pagesGeorgethirdearlo 00 WilluoftEric ThierryNo ratings yet

- Zapffe, Peter Wessel - The Last Messiah PDFDocument13 pagesZapffe, Peter Wessel - The Last Messiah PDFMatias MoulinNo ratings yet

- The Experiences and Challenges Faced of The Public School Teachers Amidst The COVID-19 Pandemic: A Phenomenological Study in The PhilippinesDocument21 pagesThe Experiences and Challenges Faced of The Public School Teachers Amidst The COVID-19 Pandemic: A Phenomenological Study in The PhilippinesDE LOS REYES MARY ZEALANo ratings yet

- Schools of PsychologyDocument30 pagesSchools of PsychologyMdl C DayritNo ratings yet

- MWSS v. CADocument15 pagesMWSS v. CAAlexander AbonadoNo ratings yet

- Clinical Psychopathology PDFDocument5 pagesClinical Psychopathology PDFelvinegunawan50% (2)

- Pulp Fiction DeconstructionDocument3 pagesPulp Fiction Deconstructiondomatthews09No ratings yet

- Informative Speech 2010 (Speaking Outline) 2Document5 pagesInformative Speech 2010 (Speaking Outline) 2FaranzaSynsNo ratings yet

- Genealogy On June 09-2003Document25 pagesGenealogy On June 09-2003syedyusufsam92100% (3)

- Why Men Are The Submissive SexDocument8 pagesWhy Men Are The Submissive SexWilliam Bond89% (9)

- Elliot WaveDocument8 pagesElliot WaveGateshNdegwahNo ratings yet

- Code of Ethics in 40 CharactersDocument8 pagesCode of Ethics in 40 Charactersvasu bansalNo ratings yet

- Literature Review 2.1. Shodhana A. Ayurvedic System of ShodhanaDocument93 pagesLiterature Review 2.1. Shodhana A. Ayurvedic System of ShodhanasiesmannNo ratings yet

- Olanzapine Drug StudyDocument1 pageOlanzapine Drug StudyJeyser T. Gamutia100% (1)

- Sector:: Automotive/Land Transport SectorDocument20 pagesSector:: Automotive/Land Transport SectorVedin Padilla Pedroso92% (12)

- Group Project Assignment Imc407Document4 pagesGroup Project Assignment Imc407Anonymous nyN7IVBMNo ratings yet

- Ssees DissertationDocument5 pagesSsees DissertationBuyAcademicPapersCanada100% (1)

- Semester I Listening Comprehension Test A Good Finder One Day Two Friends Went For A Walk. One of Them Had A Dog. "See HereDocument13 pagesSemester I Listening Comprehension Test A Good Finder One Day Two Friends Went For A Walk. One of Them Had A Dog. "See HereRichard AndersonNo ratings yet

- Briar B. Crain: EducationDocument2 pagesBriar B. Crain: Educationapi-541610137No ratings yet

- Introduction To ErgonomicsDocument16 pagesIntroduction To Ergonomicsnatrix029No ratings yet

- Scan To Folder Easy Setup GuideDocument20 pagesScan To Folder Easy Setup GuideJuliana PachecoNo ratings yet

- Electronics Engineering Technician: Semiconductor ComponentsDocument253 pagesElectronics Engineering Technician: Semiconductor Componentsnagsanthosh3No ratings yet

- Ass. 2 English Revision WsDocument3 pagesAss. 2 English Revision WsRishab ManochaNo ratings yet

- DMBS Asgnmt 3Document2 pagesDMBS Asgnmt 3abhi404171No ratings yet

- Sound of SundayDocument3 pagesSound of SundayJean PaladanNo ratings yet