You might also like

- Afsgrshsgihg RFH JKNRGJKSRH Rhi KNJHRDocument1 pageAfsgrshsgihg RFH JKNRGJKSRH Rhi KNJHRArvin Glen BeltranNo ratings yet

- Toa 34a-3Document1 pageToa 34a-3Arvin Glen BeltranNo ratings yet

- Journal Entries and Financial StatementsDocument5 pagesJournal Entries and Financial StatementsArvin Glen BeltranNo ratings yet

- Sec 30-50 (Negotiation)Document10 pagesSec 30-50 (Negotiation)Arvin Glen BeltranNo ratings yet

- Juan Clyne A. Pray Jcba Company Corrales Avenue, Cagayan de Oro City Misamis Oriental, 9000Document6 pagesJuan Clyne A. Pray Jcba Company Corrales Avenue, Cagayan de Oro City Misamis Oriental, 9000Arvin Glen BeltranNo ratings yet

- Gov Acc Assignment JuanDocument5 pagesGov Acc Assignment JuanArvin Glen BeltranNo ratings yet

- Literature Matrix Math AptitudeDocument3 pagesLiterature Matrix Math AptitudeArvin Glen BeltranNo ratings yet

- Section 1Document3 pagesSection 1Arvin Glen BeltranNo ratings yet

- Background InfoDocument1 pageBackground InfoArvin Glen BeltranNo ratings yet

- Sec 7, 8, 9Document2 pagesSec 7, 8, 9Arvin Glen BeltranNo ratings yet

- Sec 5,6, 11-13Document3 pagesSec 5,6, 11-13Arvin Glen BeltranNo ratings yet

- Sec 14 - 23Document5 pagesSec 14 - 23Arvin Glen BeltranNo ratings yet

- Actg 9 WAFI 1Document2 pagesActg 9 WAFI 1Arvin Glen BeltranNo ratings yet

- Marketing Strategy PartialDocument3 pagesMarketing Strategy PartialArvin Glen BeltranNo ratings yet

- Acc 5 Course OutlineDocument7 pagesAcc 5 Course OutlineArvin Glen BeltranNo ratings yet

- PASDocument1 pagePASArvin Glen BeltranNo ratings yet

- 1 Biodata TemplateDocument1 page1 Biodata TemplateIanusGwapitusNo ratings yet

- 3rd Year ScheduleDocument2 pages3rd Year ScheduleArvin Glen BeltranNo ratings yet

- Questioning BeingDocument2 pagesQuestioning BeingArvin Glen BeltranNo ratings yet

- De Los Santos vs. de La Cruz (Beltran & Mauna)Document2 pagesDe Los Santos vs. de La Cruz (Beltran & Mauna)Arvin Glen BeltranNo ratings yet

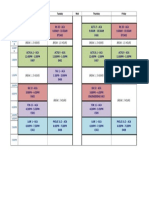

- Time Monday/Thurs DAY Tuesday/Frida Y Actg 8 BA 13.1: Break: 1.5 HoursDocument3 pagesTime Monday/Thurs DAY Tuesday/Frida Y Actg 8 BA 13.1: Break: 1.5 HoursArvin Glen BeltranNo ratings yet

- Break: 1.5 Hours Break: 1.5 Hours Break: 1.5 Hours Break: 1.5 HoursDocument1 pageBreak: 1.5 Hours Break: 1.5 Hours Break: 1.5 Hours Break: 1.5 HoursArvin Glen BeltranNo ratings yet

- Fola ExercisesDocument1 pageFola ExercisesArvin Glen BeltranNo ratings yet

- Income Tax Exercises IaDocument3 pagesIncome Tax Exercises IaArvin Glen BeltranNo ratings yet

- Law OutlineDocument11 pagesLaw OutlineArvin Glen BeltranNo ratings yet

- RaspunsuriDocument1 pageRaspunsuriRaluca RainNo ratings yet

- Architecture ComplationDocument9 pagesArchitecture ComplationArvin Glen BeltranNo ratings yet

- NBA 2K16 Keyboard MappingDocument1 pageNBA 2K16 Keyboard MappingArvin Glen BeltranNo ratings yet

- English Motivation OutlineDocument2 pagesEnglish Motivation OutlineArvin Glen BeltranNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Internal Revenue Code of 1939Document507 pagesInternal Revenue Code of 1939fredlox100% (16)

- The Kenya Gazette Vol. 42 6th April 2018Document32 pagesThe Kenya Gazette Vol. 42 6th April 2018State House Kenya88% (16)

- OligopolyDocument4 pagesOligopolyKye GarciaNo ratings yet

- Pefindo Beta Saham: Edition: 03-April-2014Document11 pagesPefindo Beta Saham: Edition: 03-April-2014Riska Ayu SetiawatiNo ratings yet

- PAC DocumentDocument554 pagesPAC DocumentOlakachuna AdonijaNo ratings yet

- Lesson 14: International Business: NATIONAL DIFFERENCES IN Political EconomyDocument4 pagesLesson 14: International Business: NATIONAL DIFFERENCES IN Political EconomyFahad AsgharNo ratings yet

- Setlawke International TaxationDocument37 pagesSetlawke International TaxationAhmad ObaidatNo ratings yet

- Strategies For Repatriating Profit From ChinaDocument12 pagesStrategies For Repatriating Profit From ChinaRazni Abd RazakNo ratings yet

- Organizational PlanDocument1 pageOrganizational PlanCarla Jamina IbeNo ratings yet

- FICO Interview AnswersDocument160 pagesFICO Interview Answersy janardhanreddy100% (1)

- Team Company ListDocument16 pagesTeam Company ListAkanksha VermaNo ratings yet

- Vishay Library Components List PDFDocument55 pagesVishay Library Components List PDFG_naharNo ratings yet

- Case AnalysisDocument3 pagesCase AnalysisCharlotte EllenNo ratings yet

- 007.litonjua Vs Eternit CorpDocument2 pages007.litonjua Vs Eternit CorpKikoy IlaganNo ratings yet

- Porter Five Force Mba IVDocument140 pagesPorter Five Force Mba IVPradeepNo ratings yet

- Alaska Milk Corporation - Leading Dairy Brand in the PhilippinesDocument11 pagesAlaska Milk Corporation - Leading Dairy Brand in the PhilippinesHerlyn YraNo ratings yet

- Michael Saul DellDocument4 pagesMichael Saul DellKartik BhatiaNo ratings yet

- Chapter 2 PDFDocument25 pagesChapter 2 PDFZi VillarNo ratings yet

- FCI Tender RepairDocument3 pagesFCI Tender RepairchengadNo ratings yet

- Presentation1 On MNCDocument18 pagesPresentation1 On MNCsunny singhNo ratings yet

- GT Capital: Up To P12B Bond IssueDocument457 pagesGT Capital: Up To P12B Bond IssueBusinessWorldNo ratings yet

- Entrepreneurship Starting and Managing Your Own BusinessDocument14 pagesEntrepreneurship Starting and Managing Your Own BusinessAbdul Halil AbdullahNo ratings yet

- VW Group PresentationDocument15 pagesVW Group PresentationShreya gourNo ratings yet

- Southwest AirlinesDocument40 pagesSouthwest AirlinesDoddi Pavan Kumar100% (2)

- Income Tax Practice Questions 1Document8 pagesIncome Tax Practice Questions 1bamberoNo ratings yet

- 004A - Supplier Qualification Questionnaire 2Document6 pages004A - Supplier Qualification Questionnaire 2Jephthah BalogunNo ratings yet

- Delpher Trades Corporation vs. IACDocument1 pageDelpher Trades Corporation vs. IACGeoanne Battad Beringuela100% (1)

- Warning Letter To Uninsured DriversDocument2 pagesWarning Letter To Uninsured DriversThe Dallas Morning NewsNo ratings yet

- Project Report of Research Methodology OnDocument44 pagesProject Report of Research Methodology OnMohit Sugandh100% (1)