You might also like

- Introduction To OR: Dr. Anupam SaxenaDocument20 pagesIntroduction To OR: Dr. Anupam Saxenakhushbu bhatiaNo ratings yet

- Birla Sun Life Insurance Product Portfolio PROJECT ReportDocument55 pagesBirla Sun Life Insurance Product Portfolio PROJECT Reportkhushbu bhatiaNo ratings yet

- Curriculum Vitae: Career ObjectiveDocument3 pagesCurriculum Vitae: Career Objectivekhushbu bhatiaNo ratings yet

- This Is A Sample JQ Report and Is Intended To Provide An Understanding OnlyDocument9 pagesThis Is A Sample JQ Report and Is Intended To Provide An Understanding Onlykhushbu bhatiaNo ratings yet

- PPM BaseDocument15 pagesPPM Basekhushbu bhatiaNo ratings yet

- Cover of The Training ReportDocument1 pageCover of The Training Reportkhushbu bhatiaNo ratings yet

- The Greatest Achievements: Nadallondon: Rohit Sharma'S Double-Ton Helps India Beat Australia by 57 Runs in 7Th OdiDocument1 pageThe Greatest Achievements: Nadallondon: Rohit Sharma'S Double-Ton Helps India Beat Australia by 57 Runs in 7Th Odikhushbu bhatiaNo ratings yet

- MahindraDocument9 pagesMahindrakhushbu bhatiaNo ratings yet

- 7 6 - M Ajor P Lans o F Bsli 3 0 7 - M AjorDocument9 pages7 6 - M Ajor P Lans o F Bsli 3 0 7 - M Ajorkhushbu bhatiaNo ratings yet

- Curriculum Vitae KhushDocument2 pagesCurriculum Vitae Khushkhushbu bhatiaNo ratings yet

- Mahindra Ppt. 1Document17 pagesMahindra Ppt. 1khushbu bhatia0% (1)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Guide Book - 2010 - Information On The Facilities Available For ESMDocument213 pagesGuide Book - 2010 - Information On The Facilities Available For ESMManoj Raghav100% (1)

- Sem-V - Principles of Taxation LawDocument2 pagesSem-V - Principles of Taxation LawNaveen SihareNo ratings yet

- Kyc Renewal Form PDFDocument2 pagesKyc Renewal Form PDFAnonymous nmQBgwNo ratings yet

- CSR1Document471 pagesCSR1Arshdeep SinghNo ratings yet

- Salary Saving/ Pension Plan: Yearly Contribution RS: 12,000/-Monthly Contribution RS: 1000Document8 pagesSalary Saving/ Pension Plan: Yearly Contribution RS: 12,000/-Monthly Contribution RS: 1000AasdNo ratings yet

- Employee Details: Old PPO NumberDocument2 pagesEmployee Details: Old PPO NumberDipankar ChakrabortyNo ratings yet

- UN Specialized Agencies PDFDocument2 pagesUN Specialized Agencies PDFhuma zaheerNo ratings yet

- Monthly Return For Unexempted Establishment Form 12ADocument1 pageMonthly Return For Unexempted Establishment Form 12AAnonymous wG3iH084No ratings yet

- Caterino v. Barry, 1st Cir. (1993)Document37 pagesCaterino v. Barry, 1st Cir. (1993)Scribd Government DocsNo ratings yet

- Stryker India PVT LTD: Payslip For The Month of April 2019Document4 pagesStryker India PVT LTD: Payslip For The Month of April 2019Anonymous scxyMokpNo ratings yet

- Resa p1 First PB 1015Document21 pagesResa p1 First PB 1015Din Rose GonzalesNo ratings yet

- Form UI2.4 - Application For Adoption Benefits01Document1 pageForm UI2.4 - Application For Adoption Benefits01senzo scholarNo ratings yet

- 2016 Individual (Brading, Anthony H. & Amy N.) GovernmentDocument49 pages2016 Individual (Brading, Anthony H. & Amy N.) GovernmentAnonymous 9coWUONo ratings yet

- BMAN23000A Exam Paper 2018-19Document7 pagesBMAN23000A Exam Paper 2018-19Munkbileg MunkhtsengelNo ratings yet

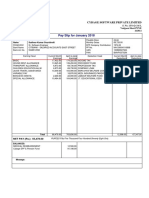

- Pay Slip For January 2018: Cybage Software Private LimitedDocument1 pagePay Slip For January 2018: Cybage Software Private LimitedSudheer0% (1)

- Instructions For Form 990-T: Internal Revenue ServiceDocument15 pagesInstructions For Form 990-T: Internal Revenue ServiceIRSNo ratings yet

- EOBI Pension/Grant Eligibility in PakistanDocument3 pagesEOBI Pension/Grant Eligibility in PakistanDanish NawazNo ratings yet

- SIN CanadaDocument6 pagesSIN CanadaMilanDivacNo ratings yet

- Form 16 FY 2018-19 PDFDocument9 pagesForm 16 FY 2018-19 PDFSujata ChoudharyNo ratings yet

- United States District Court District of Puerto RicoDocument8 pagesUnited States District Court District of Puerto RicoEmily RamosNo ratings yet

- BhartiAxa Annual ReportDocument81 pagesBhartiAxa Annual ReportAshish TiwariNo ratings yet

- Section 80 CDocument5 pagesSection 80 CAmit RoyNo ratings yet

- Brochure On Terminal Benefits For Army OfficersDocument124 pagesBrochure On Terminal Benefits For Army OfficersHarJap Singh100% (3)

- Income Tax Form 2020 IDocument1 pageIncome Tax Form 2020 ISuvashreePradhanNo ratings yet

- Nyambirai V National Social Security Authority and AnotherDocument15 pagesNyambirai V National Social Security Authority and Anotherian_ling_2100% (2)

- EPS Pension Calculator NewDocument7 pagesEPS Pension Calculator NewpswaminathanNo ratings yet

- CFReport13 16Document343 pagesCFReport13 16BernewsAdminNo ratings yet

- "Salary", "Perquisite" and "Profits in Lieu of Salary" Defined. 17Document5 pages"Salary", "Perquisite" and "Profits in Lieu of Salary" Defined. 17vineet_agrawal_ca2574No ratings yet

- South Eastern Railway South Eastern Railway Sini Workshop/ WSH Sini Workshop/ WSHDocument1 pageSouth Eastern Railway South Eastern Railway Sini Workshop/ WSH Sini Workshop/ WSHShyamal NandiNo ratings yet

- Financial Institutions Instruments and Markets 8th Edition Viney Solutions ManualDocument27 pagesFinancial Institutions Instruments and Markets 8th Edition Viney Solutions Manualdonnamargareta2g5100% (23)