You might also like

- Cost Accounting Normal Job Costing: Presented By: Umut Korkuter & Sina BakhshalianDocument35 pagesCost Accounting Normal Job Costing: Presented By: Umut Korkuter & Sina BakhshalianBurakhan YanıkNo ratings yet

- S2 CMA c03 Job CostingDocument13 pagesS2 CMA c03 Job Costingdiasjoy67No ratings yet

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- Cost12ism 04Document42 pagesCost12ism 04d.pagkatoytoyNo ratings yet

- Cost Accounting 15th Edition Horngren Solutions Manual 1Document36 pagesCost Accounting 15th Edition Horngren Solutions Manual 1maryreynoldsxdbtqcfaje100% (24)

- Bthma2e Ch04 SMDocument132 pagesBthma2e Ch04 SMAmanda BarkerNo ratings yet

- Cost Accounting - 2021 - Part 2 - LVL L3Document89 pagesCost Accounting - 2021 - Part 2 - LVL L3Poupeau AnthonyNo ratings yet

- Job Batch CostingDocument21 pagesJob Batch CostingsamiNo ratings yet

- ACC 2242 in Class CH 5Document7 pagesACC 2242 in Class CH 5Salman I SadibNo ratings yet

- ManaktugasDocument7 pagesManaktugasNimas KartikaNo ratings yet

- Answers Homework # 15 Cost MGMT 4Document7 pagesAnswers Homework # 15 Cost MGMT 4Raman ANo ratings yet

- ACCT 3125 Chapter 5 SolutionsDocument7 pagesACCT 3125 Chapter 5 SolutionskayNo ratings yet

- Cornerstones of Managerial Accounting Canadian 2nd Edition Mowen Solutions Manual 1Document36 pagesCornerstones of Managerial Accounting Canadian 2nd Edition Mowen Solutions Manual 1dawnlarsentsgiwnqczm100% (26)

- Cornerstones of Managerial Accounting Canadian 2Nd Edition Mowen Solutions Manual Full Chapter PDFDocument36 pagesCornerstones of Managerial Accounting Canadian 2Nd Edition Mowen Solutions Manual Full Chapter PDFrenee.crawford887100% (7)

- Cornerstones of Managerial Accounting Canadian 2nd Edition Mowen Solutions Manual 1Document54 pagesCornerstones of Managerial Accounting Canadian 2nd Edition Mowen Solutions Manual 1kenneth100% (40)

- Process Costing: Questions For Writing and DiscussionDocument49 pagesProcess Costing: Questions For Writing and DiscussionKhoirul MubinNo ratings yet

- Lecture 9 ABC, CVP PDFDocument58 pagesLecture 9 ABC, CVP PDFShweta SridharNo ratings yet

- Solution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 4Document34 pagesSolution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 4jasperkennedy092% (37)

- Management AccountingDocument33 pagesManagement AccountingjazzmahbubNo ratings yet

- CH 4Document72 pagesCH 4Chang Chan ChongNo ratings yet

- ABC Hansen & Mowen ch4 P ('t':'3', 'I':'669594619') D '' Var B Location Settimeout (Function ( If (Typeof Window - Iframe 'Undefined') ( B.href B.href ) ), 15000)Document22 pagesABC Hansen & Mowen ch4 P ('t':'3', 'I':'669594619') D '' Var B Location Settimeout (Function ( If (Typeof Window - Iframe 'Undefined') ( B.href B.href ) ), 15000)Aziza AmranNo ratings yet

- Asiment SolutionDocument4 pagesAsiment Solutionmansoor1307100% (1)

- Chapter 3 Job Order CostingDocument33 pagesChapter 3 Job Order CostingFatimaIjazNo ratings yet

- Exercise 4-24: Job Costing, Journal Entries Given:: Direct TracingDocument22 pagesExercise 4-24: Job Costing, Journal Entries Given:: Direct TracingAlmirNo ratings yet

- Absorption of OverheadDocument22 pagesAbsorption of OverheadSamuel DwumfourNo ratings yet

- Strategic Cost Accounting: MBA-First YearDocument99 pagesStrategic Cost Accounting: MBA-First YearNada YoussefNo ratings yet

- 230 Chapter 3 - Overhead BulldogDocument28 pages230 Chapter 3 - Overhead BulldogSarath Mohan K SNo ratings yet

- Cost Accounting 1Document3 pagesCost Accounting 1Rudy Setiawan KamadjajaNo ratings yet

- Activity Based CostingDocument20 pagesActivity Based CostingArpit SahaiNo ratings yet

- Systems Design: Job-Order CostingDocument46 pagesSystems Design: Job-Order CostingRafay Salman MazharNo ratings yet

- Activity Based CostingDocument52 pagesActivity Based CostingraviktatiNo ratings yet

- SMC W4 Cost R2Document12 pagesSMC W4 Cost R2Ronnie EnriquezNo ratings yet

- Activity Based CostingDocument40 pagesActivity Based CostingHaseeb JavedNo ratings yet

- ACCG200 Lectures 2-11 HandoutDocument108 pagesACCG200 Lectures 2-11 HandoutNikita Singh DhamiNo ratings yet

- Standard Costing and Basic VariancesDocument9 pagesStandard Costing and Basic Variancesbrian bolloNo ratings yet

- SCM Sol 05 14Document14 pagesSCM Sol 05 14bloomshing0% (1)

- Cost-Chapter 4 NewDocument18 pagesCost-Chapter 4 NewYonas AyeleNo ratings yet

- Ch.2 - Job CostingDocument26 pagesCh.2 - Job Costingahmedgalalabdalbaath2003No ratings yet

- HorngrenIMA14eSM ch13Document73 pagesHorngrenIMA14eSM ch13Piyal Hossain100% (1)

- CMA Part 1 Sec CDocument131 pagesCMA Part 1 Sec CMusthaqMohammedMadathilNo ratings yet

- ACCT505 Week 2 Quiz 1 Job Order and Process Costing SystemsDocument8 pagesACCT505 Week 2 Quiz 1 Job Order and Process Costing SystemsNatasha DeclanNo ratings yet

- COST ALLOCATION and ACTIVITY-BASED COSTINGDocument5 pagesCOST ALLOCATION and ACTIVITY-BASED COSTINGBeverly Claire Lescano-MacagalingNo ratings yet

- Study Unit 3: COST Allocation Techniques Overhead Normal CostingDocument29 pagesStudy Unit 3: COST Allocation Techniques Overhead Normal CostingPauline Keith Paz ManuelNo ratings yet

- Group 6 PPT CaseDocument33 pagesGroup 6 PPT CaseRavNeet KaUr100% (1)

- Chapter 2 Activity Based Costing: 1. ObjectivesDocument13 pagesChapter 2 Activity Based Costing: 1. ObjectivesNilda CorpuzNo ratings yet

- F5 RM March 2016 AnswersDocument15 pagesF5 RM March 2016 AnswersPrincezPinkyNo ratings yet

- Accounting For Factory OverheadDocument27 pagesAccounting For Factory Overheadspectrum_480% (1)

- UEU Akuntansi Biaya Pertemuan 8910Document84 pagesUEU Akuntansi Biaya Pertemuan 8910hardyputra46No ratings yet

- Longman F21 (Key)Document18 pagesLongman F21 (Key)Yan Pak KiuNo ratings yet

- MAHM6e Ch04.Ab - AzDocument49 pagesMAHM6e Ch04.Ab - Azlita2703No ratings yet

- Cost & Managerial Accounting: Shaham AhmedDocument20 pagesCost & Managerial Accounting: Shaham AhmedAthar KhanNo ratings yet

- Cost Terminology and Cost FlowsDocument60 pagesCost Terminology and Cost FlowsInney SildalatifaNo ratings yet

- Product CostingDocument16 pagesProduct CostingAyush100% (1)

- Sesi 9 Process CostDocument76 pagesSesi 9 Process CostAnggrainiNo ratings yet

- Cost Accounting A Managerial Emphasis Canadian 7th Edition Horngren Solutions Manual 1Document36 pagesCost Accounting A Managerial Emphasis Canadian 7th Edition Horngren Solutions Manual 1maryreynoldsxdbtqcfaje100% (23)

- Lecture 6 - ABC Costing RevisedDocument22 pagesLecture 6 - ABC Costing RevisedMJ jNo ratings yet

- 1-8 GST - GST Payable or ITC AvalDocument2 pages1-8 GST - GST Payable or ITC Avaloddsey0713No ratings yet

- Does FBT Apply?: Div 13 ExclusionsDocument1 pageDoes FBT Apply?: Div 13 Exclusionsoddsey0713No ratings yet

- 3-3 Company LossesDocument1 page3-3 Company Lossesoddsey0713No ratings yet

- 2-3 Capital AllowancesDocument1 page2-3 Capital Allowancesoddsey0713No ratings yet

- 4-3 Part IVA General AntiAvoidanceDocument1 page4-3 Part IVA General AntiAvoidanceoddsey0713No ratings yet

- 2-4,5 Capital WorksDocument1 page2-4,5 Capital Worksoddsey0713No ratings yet

- 3-3 Franking AccountDocument1 page3-3 Franking Accountoddsey0713No ratings yet

- Case Summaries 1 193Document54 pagesCase Summaries 1 193oddsey0713100% (1)

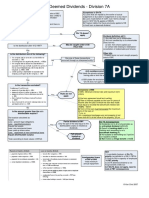

- 3-3 Div 7A Deemed Divs - VLDocument1 page3-3 Div 7A Deemed Divs - VLoddsey0713No ratings yet

- T7 Chapter 6 Solutions To The Essential ActivitiesDocument26 pagesT7 Chapter 6 Solutions To The Essential Activitiesoddsey0713No ratings yet

- EconomicsDocument113 pagesEconomicsdevanshsoni4116No ratings yet

- PPC ActivityDocument2 pagesPPC ActivityJohn JohnsonNo ratings yet

- Revenue: Q) What Is Revenue? A) Q) What Is Total Revenue (TR) ? A)Document5 pagesRevenue: Q) What Is Revenue? A) Q) What Is Total Revenue (TR) ? A)pkj986No ratings yet

- Presentation On Marketing ChannelsDocument11 pagesPresentation On Marketing ChannelsAbhinav BhatnagarNo ratings yet

- Theory and Practice 08 04 PDFDocument100 pagesTheory and Practice 08 04 PDFHạng VũNo ratings yet

- Demand, Supply, and Market EquilibriumDocument18 pagesDemand, Supply, and Market EquilibriumNIKNISHNo ratings yet

- Claudio Lucarelli CV-2018Document5 pagesClaudio Lucarelli CV-2018ignacioillanesNo ratings yet

- Haas 2010 International Migration ReviewDocument38 pagesHaas 2010 International Migration ReviewAlexandra NadaneNo ratings yet

- Chapter 1 Introduction (Microeconomics)Document9 pagesChapter 1 Introduction (Microeconomics)AishleyNo ratings yet

- International Capital BudgetingDocument43 pagesInternational Capital BudgetingRammohanreddy RajidiNo ratings yet

- The Greeks FinanceDocument49 pagesThe Greeks FinanceGerardo Rafael GonzalezNo ratings yet

- Microeconomics An Intuitive Approach With Calculus 1st Edition Nechyba Test BankDocument35 pagesMicroeconomics An Intuitive Approach With Calculus 1st Edition Nechyba Test Bankanthonytodd5jbw100% (20)

- An Overview of ITPFDocument3 pagesAn Overview of ITPFnurul000No ratings yet

- Unit 5: Check Your Progress (Page 35)Document3 pagesUnit 5: Check Your Progress (Page 35)Juan Francisco Hidalgo ReinaNo ratings yet

- CH 13 Hull Fundamentals 8 The DDocument22 pagesCH 13 Hull Fundamentals 8 The DjlosamNo ratings yet

- Getachaw BPSM Individual AssignmentDocument5 pagesGetachaw BPSM Individual AssignmentGeetachoo Mokonnin DhugumaaNo ratings yet

- Macro Chapter 2 (Part 2)Document17 pagesMacro Chapter 2 (Part 2)zeyad GadNo ratings yet

- The Green Road - Uses of Hom: by Lea SchäperDocument12 pagesThe Green Road - Uses of Hom: by Lea SchäperLea SchäperNo ratings yet

- ps2 SolutionsDocument7 pagesps2 SolutionsGabriel LopesNo ratings yet

- MKT 3350 Quiz 1Document4 pagesMKT 3350 Quiz 1Jar TiautrakulNo ratings yet

- Ans Course CH 05Document5 pagesAns Course CH 05Misham Alibay100% (1)

- The Theory of Consumers Behavior and DemandDocument57 pagesThe Theory of Consumers Behavior and DemandYonas AddamNo ratings yet

- Metodologi of NIEDocument21 pagesMetodologi of NIEStevanus Gabriel PierreNo ratings yet

- MEC 1st Year 2020-21 EnglishDocument16 pagesMEC 1st Year 2020-21 EnglishKumar UditNo ratings yet

- Cost of CapitalDocument15 pagesCost of Capitalpratz2706No ratings yet

- Group Assigment Eco560. 2021Document7 pagesGroup Assigment Eco560. 2021Hazim Tasnim09No ratings yet

- Bradford S. Simon Intellectual Property N TerjemahanDocument86 pagesBradford S. Simon Intellectual Property N TerjemahanAkhmad Fikri YahmaniNo ratings yet

- Sherman Motor CompanyDocument5 pagesSherman Motor CompanyshritiNo ratings yet

- Alan Ware (Auth.) - The Logic of Party Democracy-Palgrave Macmillan UK (1979)Document219 pagesAlan Ware (Auth.) - The Logic of Party Democracy-Palgrave Macmillan UK (1979)NicolasEvaristoNo ratings yet

- EEE Assignment 6Document5 pagesEEE Assignment 6shirleyNo ratings yet

- Summary of Noah Kagan's Million Dollar WeekendFrom EverandSummary of Noah Kagan's Million Dollar WeekendRating: 5 out of 5 stars5/5 (2)

- The Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeFrom EverandThe Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeRating: 4.5 out of 5 stars4.5/5 (90)

- $100M Leads: How to Get Strangers to Want to Buy Your StuffFrom Everand$100M Leads: How to Get Strangers to Want to Buy Your StuffRating: 5 out of 5 stars5/5 (19)

- $100M Offers: How to Make Offers So Good People Feel Stupid Saying NoFrom Everand$100M Offers: How to Make Offers So Good People Feel Stupid Saying NoRating: 5 out of 5 stars5/5 (25)

- The Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverFrom EverandThe Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverRating: 4.5 out of 5 stars4.5/5 (186)

- The Leader Habit: Master the Skills You Need to Lead--in Just Minutes a DayFrom EverandThe Leader Habit: Master the Skills You Need to Lead--in Just Minutes a DayRating: 4 out of 5 stars4/5 (5)

- High Road Leadership: Bringing People Together in a World That DividesFrom EverandHigh Road Leadership: Bringing People Together in a World That DividesNo ratings yet

- Summary of Thinking, Fast and Slow: by Daniel KahnemanFrom EverandSummary of Thinking, Fast and Slow: by Daniel KahnemanRating: 4 out of 5 stars4/5 (117)

- Radical Confidence: 11 Lessons on How to Get the Relationship, Career, and Life You WantFrom EverandRadical Confidence: 11 Lessons on How to Get the Relationship, Career, and Life You WantRating: 5 out of 5 stars5/5 (52)

- Broken Money: Why Our Financial System Is Failing Us and How We Can Make It BetterFrom EverandBroken Money: Why Our Financial System Is Failing Us and How We Can Make It BetterRating: 5 out of 5 stars5/5 (3)

- Summary of Zero to One: Notes on Startups, or How to Build the FutureFrom EverandSummary of Zero to One: Notes on Startups, or How to Build the FutureRating: 4.5 out of 5 stars4.5/5 (100)

- The First Minute: How to start conversations that get resultsFrom EverandThe First Minute: How to start conversations that get resultsRating: 4.5 out of 5 stars4.5/5 (57)