You might also like

- AuditSampleForms Master Sept 27 2011Document92 pagesAuditSampleForms Master Sept 27 2011Marta OsorioNo ratings yet

- Income Statement: Khybey Tobacco Company LTDDocument15 pagesIncome Statement: Khybey Tobacco Company LTDMuzamil Ur rehmanNo ratings yet

- Dummy Financial ModelDocument17 pagesDummy Financial ModelarhawnnNo ratings yet

- Tax Audit Checklist for Form 3CDDocument36 pagesTax Audit Checklist for Form 3CDKoolmindNo ratings yet

- General Internal Audit ModelDocument5 pagesGeneral Internal Audit ModelSoko A. KamaraNo ratings yet

- ACCT212 WorkingPapers E3-31ADocument2 pagesACCT212 WorkingPapers E3-31Alowluder0% (1)

- Audit Planning Scenarios AnalysisDocument6 pagesAudit Planning Scenarios AnalysisUsman PirzadaNo ratings yet

- Audit Programe For Statutory AuditDocument20 pagesAudit Programe For Statutory AuditTekumani Naveen KumarNo ratings yet

- BiiiimplmoniwbDocument34 pagesBiiiimplmoniwbShruti DubeyNo ratings yet

- 8e Mini Case AnalyticsDocument6 pages8e Mini Case Analyticskyu77ryu0% (5)

- Test of Controls - Purchase Transactions Audit Objective Audit Procedure FindingsDocument9 pagesTest of Controls - Purchase Transactions Audit Objective Audit Procedure FindingscrystalroselleNo ratings yet

- Type Answers On This Side of The Page OnlyDocument40 pagesType Answers On This Side of The Page Only嘉慧No ratings yet

- Initiate and Complete A Journal Entry Document Via Park Document (Document Types SA or ZB)Document18 pagesInitiate and Complete A Journal Entry Document Via Park Document (Document Types SA or ZB)Padma NagaNo ratings yet

- Case 3Document19 pagesCase 3Mafel LabadanNo ratings yet

- ACCA AAA S18 Notes PDFDocument156 pagesACCA AAA S18 Notes PDFAhmer Ahmed100% (1)

- Inventory Excel UploadDocument36 pagesInventory Excel Uploadaadi1012No ratings yet

- CMA Part 1 - Budgeting ConceptDocument1 pageCMA Part 1 - Budgeting ConceptHoneyNo ratings yet

- Sap FiDocument4 pagesSap FiNicky AugustineNo ratings yet

- Sec 7060Document17 pagesSec 7060Fallon LoboNo ratings yet

- SAP - FICO Course ContentDocument10 pagesSAP - FICO Course Contentchaitanya vutukuriNo ratings yet

- IND AS-16 Property, Plant and Equipment: Measurement of PpeDocument3 pagesIND AS-16 Property, Plant and Equipment: Measurement of PpeHimank SinglaNo ratings yet

- SAP FICO Interview QuestionsDocument16 pagesSAP FICO Interview QuestionsHaribabu SunkaraNo ratings yet

- Questionnaire For Financial AuditDocument2 pagesQuestionnaire For Financial AuditChaNo ratings yet

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet

- Account Receivable NotesDocument28 pagesAccount Receivable Noteskeeru_bioNo ratings yet

- PFRS 15 Work ProgramDocument101 pagesPFRS 15 Work ProgramMichael ArciagaNo ratings yet

- Gen Ledger AccountsDocument15 pagesGen Ledger AccountsMoises CalastravoNo ratings yet

- CA Ravi Taori document clausesDocument2 pagesCA Ravi Taori document clausesTejNo ratings yet

- Balance Sheet AuditingDocument29 pagesBalance Sheet Auditingtanim duNo ratings yet

- CH 6 Model 14 Free Cash Flow CalculationDocument12 pagesCH 6 Model 14 Free Cash Flow CalculationrealitNo ratings yet

- TallyDocument77 pagesTallyPawan SinghNo ratings yet

- MA ACCA Sunway Tes Chapter AssessmentDocument434 pagesMA ACCA Sunway Tes Chapter AssessmentFarahAin Fain100% (2)

- Past Papers CSS Financial AccountingDocument5 pagesPast Papers CSS Financial AccountingMasood Ahmad AadamNo ratings yet

- Boa Tos Auditing.Document4 pagesBoa Tos Auditing.shalomNo ratings yet

- Sujit 1 PDFDocument380 pagesSujit 1 PDFŞâh Šůmiť100% (1)

- Month End and Year End ActivitiesDocument6 pagesMonth End and Year End ActivitiesAnonymous ldfiOk97uNo ratings yet

- Financial ModellingDocument22 pagesFinancial ModellingSyam MohanNo ratings yet

- CHAPTER 4 - AssociatesDocument11 pagesCHAPTER 4 - AssociatesSheikh Mass JahNo ratings yet

- SAP FICO Video Course Content & Materials Detials PDFDocument3 pagesSAP FICO Video Course Content & Materials Detials PDFManjunathreddy SeshadriNo ratings yet

- IFRSDocument103 pagesIFRSnoman.786100% (2)

- Tuition Mock D11 - F7 Questions FinalDocument11 pagesTuition Mock D11 - F7 Questions FinalRenato WilsonNo ratings yet

- Fico (Summarized) : Fiscal YearDocument53 pagesFico (Summarized) : Fiscal YearAbdul Basit SheikhNo ratings yet

- SAP FI Tables and Tcodes GuideDocument2 pagesSAP FI Tables and Tcodes GuidekarunaNo ratings yet

- Relevant Costing ChartDocument1 pageRelevant Costing Chartjonnajon92-1100% (1)

- ACCA F7 Study Material 2013 LSBF Lecture + Class NotesDocument2 pagesACCA F7 Study Material 2013 LSBF Lecture + Class NotesSamir Hasanov0% (1)

- Time: 3 Hours Total Marks: 100: Printed Pages: 03 Sub Code: KMB103 Paper Id: 270103 Roll NoDocument4 pagesTime: 3 Hours Total Marks: 100: Printed Pages: 03 Sub Code: KMB103 Paper Id: 270103 Roll NoAbhishek ChaubeyNo ratings yet

- Final Financials-Adam's Apple 2019Document26 pagesFinal Financials-Adam's Apple 2019tsere butsereNo ratings yet

- F7 Workbook Q PDFDocument124 pagesF7 Workbook Q PDFLêNgọcTùngNo ratings yet

- Rizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)Document3 pagesRizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)faheemNo ratings yet

- SAP FICO Transaction CodesDocument4 pagesSAP FICO Transaction CodesParesh VaghasiyaNo ratings yet

- ControllingDocument21 pagesControllingPallavi ChittiNo ratings yet

- Audit Test - ReceivablesDocument22 pagesAudit Test - ReceivablesRachael RuNo ratings yet

- SAP Withholding Tax Configuration StepsDocument1 pageSAP Withholding Tax Configuration StepsNic NgNo ratings yet

- Sap Accounting EntriesDocument5 pagesSap Accounting EntriesonionheadmonsterNo ratings yet

- New Audit Report Format Including Caro 2016 by AniketDocument10 pagesNew Audit Report Format Including Caro 2016 by AniketarjunmarwadiNo ratings yet

- ITC Report of AuditorsDocument3 pagesITC Report of AuditorsRajavati NadarNo ratings yet

- New Audit Report Format Including CARO 2016Document8 pagesNew Audit Report Format Including CARO 2016CA Shivang SoniNo ratings yet

- Jet Airways Audit Report PDFDocument12 pagesJet Airways Audit Report PDFsatish100% (1)

- TVS Audit ReportDocument5 pagesTVS Audit ReportYashasvi MohandasNo ratings yet

- Sale DeedDocument5 pagesSale DeedNitin GoyalNo ratings yet

- Income Declaration Scheme Rules, 2016: Form 1Document9 pagesIncome Declaration Scheme Rules, 2016: Form 1Nikhil KasatNo ratings yet

- Black Money BillDocument30 pagesBlack Money BillNikhil KasatNo ratings yet

- BLack Money RulesDocument23 pagesBLack Money RulesLive LawNo ratings yet

- Derivatives Markets in Interest Rate & Foreign Exchange RateDocument20 pagesDerivatives Markets in Interest Rate & Foreign Exchange RatehdjfhsjfhwjfNo ratings yet

- Hedging With Financial DerivativesDocument30 pagesHedging With Financial DerivativesNikhil KasatNo ratings yet

- DTL Sec 10Document14 pagesDTL Sec 10Nikhil KasatNo ratings yet

- Types of stamps and concepts of stamp dutyDocument5 pagesTypes of stamps and concepts of stamp dutyNikhil Kasat100% (2)

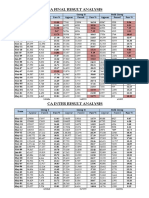

- CA Result AnalysisDocument1 pageCA Result AnalysisNikhil KasatNo ratings yet

- Banca SuranceDocument32 pagesBanca SuranceNikhil KasatNo ratings yet

- Some Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Document21 pagesSome Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Nikhil KasatNo ratings yet

- ApplicabiliTY of ProvisionsDocument3 pagesApplicabiliTY of ProvisionsNikhil KasatNo ratings yet

- Delhi Dvat Registration InformationDocument4 pagesDelhi Dvat Registration InformationNikhil KasatNo ratings yet

- Agricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheDocument9 pagesAgricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheNikhil KasatNo ratings yet

- How to score 12-14 marks on Professional Ethics exam questionsDocument2 pagesHow to score 12-14 marks on Professional Ethics exam questionsNikhil KasatNo ratings yet

- List of Indian As Convergence With IfrsDocument1 pageList of Indian As Convergence With IfrsNikhil KasatNo ratings yet

- Calculate Fees and Stamp Duty for Increase in Authorised Share CapitalDocument10 pagesCalculate Fees and Stamp Duty for Increase in Authorised Share CapitalNikhil KasatNo ratings yet

- Directors Report As Per StatusDocument5 pagesDirectors Report As Per StatusNikhil KasatNo ratings yet

- Web Base Timesheet ApplicationDocument4 pagesWeb Base Timesheet ApplicationNikhil KasatNo ratings yet

- Curriculum VitaeDocument13 pagesCurriculum VitaeNikhil KasatNo ratings yet

- Valuation of InventoriesDocument4 pagesValuation of InventoriesNikhil KasatNo ratings yet

- Importance of ArticleshipDocument6 pagesImportance of ArticleshipNikhil KasatNo ratings yet

- Anf 4dDocument3 pagesAnf 4dNikhil KasatNo ratings yet

- August Month CompliancesDocument1 pageAugust Month CompliancesNikhil KasatNo ratings yet

- C01Document23 pagesC01Silvery DoeNo ratings yet

- Tds On SalariesDocument55 pagesTds On SalariespunitNo ratings yet

- Privileges To Small CompaniesDocument2 pagesPrivileges To Small CompaniesNikhil KasatNo ratings yet

- Ind As 2015Document2 pagesInd As 2015Nikhil KasatNo ratings yet

- CUSTOMS VALUATION COMPUTATIONDocument8 pagesCUSTOMS VALUATION COMPUTATIONNikhil KasatNo ratings yet

- Nursing AuditDocument26 pagesNursing AuditJoe ShewaleNo ratings yet

- Cortez, Danica M. - IUEEU AssignmentDocument2 pagesCortez, Danica M. - IUEEU AssignmentDanica CortezNo ratings yet

- AGP Corporate Audit Plan 2020-21Document46 pagesAGP Corporate Audit Plan 2020-21The Learning Solutions Home TutorsNo ratings yet

- Low Interest Loan - Business Support For NYSC Graduates - BOIDocument5 pagesLow Interest Loan - Business Support For NYSC Graduates - BOIsamuel olasupoNo ratings yet

- Roots Industries Annual Report 2019Document84 pagesRoots Industries Annual Report 2019Mr. K.S. Raghul Asst Prof MECH0% (1)

- ICICI BANK AR 2019 Directors Report PDFDocument71 pagesICICI BANK AR 2019 Directors Report PDFSailendran MenattamaiNo ratings yet

- Environmental ManualDocument34 pagesEnvironmental Manualgs_humboldt100% (4)

- McKinnon - 2019Document395 pagesMcKinnon - 2019Pribac SorinNo ratings yet

- TR006 NQA Client Transition Gap Analysis Tool 9001 v6Document13 pagesTR006 NQA Client Transition Gap Analysis Tool 9001 v6HeltonNo ratings yet

- Maximizing Skills at BWSI Water CompanyDocument29 pagesMaximizing Skills at BWSI Water Companysecret secretNo ratings yet

- Quality Management in HealthcareDocument65 pagesQuality Management in HealthcareSunny Patel100% (1)

- Lesson 2 Quiz MaterialDocument4 pagesLesson 2 Quiz Materiallinkin soyNo ratings yet

- CMADDocument4 pagesCMADSridhanyas kitchenNo ratings yet

- Cross-Examination: Sharpstein/TabernackiDocument222 pagesCross-Examination: Sharpstein/TabernackiWashington Free BeaconNo ratings yet

- Krispy Kreme Case Assignment QuestionsDocument4 pagesKrispy Kreme Case Assignment QuestionsDinh TonNo ratings yet

- Telstra Cyber Security Report 2017 - WhitepaperDocument52 pagesTelstra Cyber Security Report 2017 - WhitepaperllNo ratings yet

- Franchise Agreement For PansolDocument19 pagesFranchise Agreement For PansolSUNCREST GAS CORPORATION COMPLIANCENo ratings yet

- Audit Evidence and ProceduresDocument62 pagesAudit Evidence and ProceduresQuynh AnhNo ratings yet

- Controls and ScotsDocument5 pagesControls and ScotsRacez GabonNo ratings yet

- 2006 Canada AG Report On NFTCDocument18 pages2006 Canada AG Report On NFTCnickb117No ratings yet

- Chapter 2 AISDocument3 pagesChapter 2 AISgailmissionNo ratings yet

- Feliciano Vs Coa DigestDocument17 pagesFeliciano Vs Coa DigestRandy LopezNo ratings yet

- Building Structures Audit, Repair and RehabilitationDocument2 pagesBuilding Structures Audit, Repair and Rehabilitationyedidi0% (1)

- Importance of StatisticsDocument12 pagesImportance of StatisticsMuhammad Zain100% (2)

- Ethical Decisions in AccountingDocument24 pagesEthical Decisions in AccountingNia MNo ratings yet

- An Overview of AuditingDocument38 pagesAn Overview of AuditingWita AnggarainiNo ratings yet

- GAAS GAADocument13 pagesGAAS GAAshudayeNo ratings yet

- Audit of Different Types of Entity Summary Notes by CA Kapil GoyalDocument24 pagesAudit of Different Types of Entity Summary Notes by CA Kapil GoyalDrake DDNo ratings yet

- I190378914 1Document6 pagesI190378914 1Appie KoekangeNo ratings yet

- Energy Efficiency in Europe: Country ReportDocument8 pagesEnergy Efficiency in Europe: Country ReportFlamandu MariusNo ratings yet