You might also like

- Starcmpt CaseDocument28 pagesStarcmpt CaseKenneth SandersNo ratings yet

- Star CMP TDocument28 pagesStar CMP TKenneth SandersNo ratings yet

- OBLBoard LawsuitDocument114 pagesOBLBoard LawsuitNye Lavalle100% (1)

- The King Takes Your Castle: City Laws That Restrict Your Property RightsFrom EverandThe King Takes Your Castle: City Laws That Restrict Your Property RightsNo ratings yet

- Combined Final Amended Complaint Filed 04-13-2016 WithDocument215 pagesCombined Final Amended Complaint Filed 04-13-2016 WithSampallNo ratings yet

- What You Need To Know About The American Tax Trap, Loss of Privacy, and How You Can Join The Globalized EconomyFrom EverandWhat You Need To Know About The American Tax Trap, Loss of Privacy, and How You Can Join The Globalized EconomyNo ratings yet

- Supreme Court of The State of New York County of New York: Defendal TsDocument28 pagesSupreme Court of The State of New York County of New York: Defendal TscorruptioncurrentsNo ratings yet

- The Road Out of Debt + Website: Bankruptcy and Other Solutions to Your Financial ProblemsFrom EverandThe Road Out of Debt + Website: Bankruptcy and Other Solutions to Your Financial ProblemsNo ratings yet

- Aaron Greenspan LawsuitDocument146 pagesAaron Greenspan Lawsuitrobinwauters100% (2)

- Whistleblowers: Incentives, Disincentives, and Protection StrategiesFrom EverandWhistleblowers: Incentives, Disincentives, and Protection StrategiesNo ratings yet

- Watson V NCO Capital One FDCPA ComplaintDocument30 pagesWatson V NCO Capital One FDCPA ComplaintghostgripNo ratings yet

- Redacted JPM FilingDocument122 pagesRedacted JPM FilingZerohedge100% (1)

- Think Computer v. DwollaDocument37 pagesThink Computer v. Dwollaolga vosNo ratings yet

- Commercial Real Estate Restructuring Revolution: Strategies, Tranche Warfare, and Prospects for RecoveryFrom EverandCommercial Real Estate Restructuring Revolution: Strategies, Tranche Warfare, and Prospects for RecoveryNo ratings yet

- U.S. Virgin Island V JPMorgan Chase Bank N.A. Second Amended Complaint Filed April 12 2023Document42 pagesU.S. Virgin Island V JPMorgan Chase Bank N.A. Second Amended Complaint Filed April 12 2023Sarah WestallNo ratings yet

- U.S. v. Sun Myung Moon 532 F.Supp. 1360 (1982)From EverandU.S. v. Sun Myung Moon 532 F.Supp. 1360 (1982)No ratings yet

- U.S. Virgin Islands V JP MorganDocument30 pagesU.S. Virgin Islands V JP MorganZerohedge Janitor100% (1)

- Second Amended Complaint USVI JPMDocument119 pagesSecond Amended Complaint USVI JPMCNBC.comNo ratings yet

- Tom Lawler (Criminal)Document14 pagesTom Lawler (Criminal)Mike Farell100% (1)

- United States of America Ex Rei., Victor E. Bibby and Brian J. Donnelly, Vs Wells Fargo, Country Wide, Bank of America, Jpmorgan Chase, Et AlDocument67 pagesUnited States of America Ex Rei., Victor E. Bibby and Brian J. Donnelly, Vs Wells Fargo, Country Wide, Bank of America, Jpmorgan Chase, Et AlForeclosure FraudNo ratings yet

- Amended & Unredacted Lawsuit of The U.S. Virgin Islands v. JP MorganDocument35 pagesAmended & Unredacted Lawsuit of The U.S. Virgin Islands v. JP MorganChefs Best Statements - NewsNo ratings yet

- USDC FLA WPB Spring Intervene Response To Motion June22Document43 pagesUSDC FLA WPB Spring Intervene Response To Motion June22JaniceWolkGrenadierNo ratings yet

- Good True bill-Administrative-ClaimDocument9 pagesGood True bill-Administrative-Claimjoe100% (3)

- Operation Clean SweepDocument12 pagesOperation Clean SweepCreditScoreAide.com71% (7)

- St. Clair County IL V MERSDocument26 pagesSt. Clair County IL V MERSWonderland Explorer100% (1)

- OcwensuitDocument123 pagesOcwensuitpatamia100% (1)

- Ponzi Civil Rico ComplaintDocument109 pagesPonzi Civil Rico ComplaintRandy PotterNo ratings yet

- District Court II Back-Up 2Document12 pagesDistrict Court II Back-Up 2Samuel RichardsonNo ratings yet

- FTC Sues Acquinity INteractiveDocument17 pagesFTC Sues Acquinity INteractiveJennifer SelleckNo ratings yet

- Keven J. Wilcox, William Shepro Charged With Indirect Criminal Contempt, Fraud and ConspiracyDocument3 pagesKeven J. Wilcox, William Shepro Charged With Indirect Criminal Contempt, Fraud and ConspiracyChristopher Stoller EDNo ratings yet

- Dhid Et Al Civil Forfeiture ComplaintDocument54 pagesDhid Et Al Civil Forfeiture ComplaintIsrael VenkatNo ratings yet

- Tom Lawler Tries and Fails Again FCUSADocument10 pagesTom Lawler Tries and Fails Again FCUSAMike FarellNo ratings yet

- NY FCA Complaint - ProposedDocument14 pagesNY FCA Complaint - ProposedAvram100% (1)

- Bancoro Amended Complaint 00133192Document27 pagesBancoro Amended Complaint 00133192vpjNo ratings yet

- Fortune Hi Tec SentençaDocument24 pagesFortune Hi Tec SentençaMarco Aurélio Vogel Gomes de MelloNo ratings yet

- FTC Complaint - Savings Makes Money Complaint File Stamped 8-16-17Document44 pagesFTC Complaint - Savings Makes Money Complaint File Stamped 8-16-17Eric GreenNo ratings yet

- 8-20-2013 PHX Light SF LTD Et Al v. JPMCDocument503 pages8-20-2013 PHX Light SF LTD Et Al v. JPMCDiane SternNo ratings yet

- ComplaintDocument188 pagesComplaintjim168No ratings yet

- Case Against IndyMac and PaulsonDocument288 pagesCase Against IndyMac and PaulsonWho's in my Fund100% (1)

- LCCR Q & R 013188-13240 Aaran Money Wire Service, Inc Questionnaire and Response Dated 05/28/2002Document53 pagesLCCR Q & R 013188-13240 Aaran Money Wire Service, Inc Questionnaire and Response Dated 05/28/2002LCCR AdminNo ratings yet

- 2011-10-04 12pm ComplaintDocument52 pages2011-10-04 12pm ComplaintJon CampbellNo ratings yet

- Under Seal Pursuant To: Attorney For State of New YorkDocument9 pagesUnder Seal Pursuant To: Attorney For State of New Yorklarry-612445No ratings yet

- Tara Murphy Settlement AgreementDocument11 pagesTara Murphy Settlement Agreementjalt61No ratings yet

- WANTA - Mandamus PetitionDocument65 pagesWANTA - Mandamus PetitionBill STollerNo ratings yet

- Wikimedia v. NSA (Amicus Brief)Document35 pagesWikimedia v. NSA (Amicus Brief)The Brennan Center for JusticeNo ratings yet

- TRO Temporary Restraining Order Pleadings 39-2Document13 pagesTRO Temporary Restraining Order Pleadings 39-2DUTCH551400100% (3)

- YoungThug LawsuitDocument35 pagesYoungThug Lawsuitmitchell6northamNo ratings yet

- Go v. IACDocument7 pagesGo v. IACKathleen del RosarioNo ratings yet

- Federal Lawsuit Holly RidgeDocument20 pagesFederal Lawsuit Holly RidgeMichael PraatsNo ratings yet

- Student Loan IMFDocument18 pagesStudent Loan IMF:Ghana :Bonsu-Agyapon :Opa-Re©™®100% (2)

- UIF García LunaDocument131 pagesUIF García LunaAristegui Noticias100% (1)

- Federal Home Loan Bank of San Francisco v. Deutsche Bank Securities Inc. Et AlDocument26 pagesFederal Home Loan Bank of San Francisco v. Deutsche Bank Securities Inc. Et AlIsaac GradmanNo ratings yet

- As Amended (Hereinafter The "Uniform Securities Act"), Solely As ToDocument24 pagesAs Amended (Hereinafter The "Uniform Securities Act"), Solely As Totriguy_2010No ratings yet

- R. Kelly v. Burrowes - First Amended Complaint PDFDocument23 pagesR. Kelly v. Burrowes - First Amended Complaint PDFMark JaffeNo ratings yet

- RomeFin ComplaintDocument13 pagesRomeFin ComplaintRandy PotterNo ratings yet

- Joseph Ruggiero Employment AgreementDocument6 pagesJoseph Ruggiero Employment AgreementjspectorNo ratings yet

- Pennies For Charity 2018Document12 pagesPennies For Charity 2018ZacharyEJWilliamsNo ratings yet

- Film Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFDocument8 pagesFilm Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFjspectorNo ratings yet

- Federal Budget Fiscal Year 2017 Web VersionDocument36 pagesFederal Budget Fiscal Year 2017 Web VersionjspectorNo ratings yet

- State Health CoverageDocument26 pagesState Health CoveragejspectorNo ratings yet

- IG LetterDocument3 pagesIG Letterjspector100% (1)

- Cornell ComplaintDocument41 pagesCornell Complaintjspector100% (1)

- 2017 08 18 Constitution OrderDocument27 pages2017 08 18 Constitution OrderjspectorNo ratings yet

- Abo 2017 Annual ReportDocument65 pagesAbo 2017 Annual ReportrkarlinNo ratings yet

- Teacher Shortage Report 05232017 PDFDocument16 pagesTeacher Shortage Report 05232017 PDFjspectorNo ratings yet

- NYSCrimeReport2016 PrelimDocument14 pagesNYSCrimeReport2016 PrelimjspectorNo ratings yet

- SNY0517 Crosstabs 052417Document4 pagesSNY0517 Crosstabs 052417Nick ReismanNo ratings yet

- Inflation AllowablegrowthfactorsDocument1 pageInflation AllowablegrowthfactorsjspectorNo ratings yet

- Class of 2022Document1 pageClass of 2022jspectorNo ratings yet

- Oag Sed Letter Ice 2-27-17Document3 pagesOag Sed Letter Ice 2-27-17BethanyNo ratings yet

- Opiods 2017-04-20-By Numbers Brief No8Document17 pagesOpiods 2017-04-20-By Numbers Brief No8rkarlinNo ratings yet

- Hiffa Settlement Agreement ExecutedDocument5 pagesHiffa Settlement Agreement ExecutedNick Reisman0% (1)

- Youth Cigarette and E-Cigs UseDocument1 pageYouth Cigarette and E-Cigs UsejspectorNo ratings yet

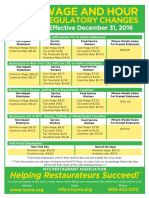

- Wage and Hour Regulatory Changes 2016Document2 pagesWage and Hour Regulatory Changes 2016jspectorNo ratings yet

- Siena Poll March 27, 2017Document7 pagesSiena Poll March 27, 2017jspectorNo ratings yet

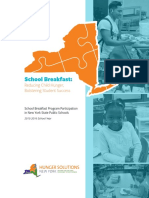

- 2017 School Bfast Report Online Version 3-7-17 0Document29 pages2017 School Bfast Report Online Version 3-7-17 0jspectorNo ratings yet

- Schneiderman Voter Fraud Letter 022217Document2 pagesSchneiderman Voter Fraud Letter 022217Matthew HamiltonNo ratings yet

- 16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsDocument55 pages16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsjspectorNo ratings yet

- Activity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017Document4 pagesActivity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017jspectorNo ratings yet

- Review of Executive Budget 2017Document102 pagesReview of Executive Budget 2017Nick ReismanNo ratings yet

- Voting Report CardDocument1 pageVoting Report CardjspectorNo ratings yet

- p12 Budget Testimony 2-14-17Document31 pagesp12 Budget Testimony 2-14-17jspectorNo ratings yet

- Darweesh Cities AmicusDocument32 pagesDarweesh Cities AmicusjspectorNo ratings yet

- 2016 Local Sales Tax CollectionsDocument4 pages2016 Local Sales Tax CollectionsjspectorNo ratings yet

- Pub Auth Num 2017Document54 pagesPub Auth Num 2017jspectorNo ratings yet

- Vinay - A S - 374996044 PDFDocument4 pagesVinay - A S - 374996044 PDFAnkita AgarwalNo ratings yet

- Republic Act No 9211Document9 pagesRepublic Act No 9211Marton Emile DesalesNo ratings yet

- Mark Up Mark DownDocument22 pagesMark Up Mark DownAnonymous rWn3ZVARLgNo ratings yet

- Sabastina EllingsworthDocument2 pagesSabastina Ellingsworthapi-381843241No ratings yet

- Analyze Walmart and AmazonDocument3 pagesAnalyze Walmart and AmazonVikram Kumar50% (2)

- Ikea IndiaDocument11 pagesIkea IndiaVico Ling100% (6)

- Chapter 9 - Test BankDocument52 pagesChapter 9 - Test Bankjdiaz_64624767% (3)

- Credit Access Grameen Limited IPO Note-201808071226511901045Document16 pagesCredit Access Grameen Limited IPO Note-201808071226511901045Arvind KumarNo ratings yet

- Retail Management - Test 1 PDFDocument2 pagesRetail Management - Test 1 PDFSivagnana SelvakumarNo ratings yet

- Fashioning LondonDocument224 pagesFashioning LondonBetuel0% (1)

- Early Development of Marketing ThoughtDocument14 pagesEarly Development of Marketing ThoughtCarlos RodriguezNo ratings yet

- Mojari Craft 0Document42 pagesMojari Craft 0bharti khannaNo ratings yet

- Antonella Cappiello PDFDocument123 pagesAntonella Cappiello PDFCarlos Andrés HerreraNo ratings yet

- Chapter 5 Retail Market StrategyDocument38 pagesChapter 5 Retail Market StrategyJean Leonor100% (1)

- Southern Health, Prairie Mountain Health & Interlake-Eastern RestrictionsDocument3 pagesSouthern Health, Prairie Mountain Health & Interlake-Eastern RestrictionsChrisDca100% (1)

- MARINE SERRE-Roshni DhandabaniDocument63 pagesMARINE SERRE-Roshni DhandabaniRoshniNo ratings yet

- Increase Store Foot Traffic Using Digital MarketingDocument16 pagesIncrease Store Foot Traffic Using Digital MarketingShoutout Digital - SEO AgencyNo ratings yet

- Jewellery Management System Project inDocument36 pagesJewellery Management System Project inRoy AmitNo ratings yet

- L7 Does Shopping Behavior Impact SustainabilityDocument7 pagesL7 Does Shopping Behavior Impact SustainabilityYi ZhangNo ratings yet

- Unit 2 Explore QuestionsDocument2 pagesUnit 2 Explore QuestionsViacel GamboaNo ratings yet

- Types of Loyalty ProgramDocument4 pagesTypes of Loyalty ProgramdianNo ratings yet

- CL Smartec Build SystemDocument24 pagesCL Smartec Build SystemSmartec Build System Pvt. Ltd.No ratings yet

- Walmart and Anti-TrustDocument24 pagesWalmart and Anti-Trustchiragmangalick100% (1)

- Research ProposalDocument75 pagesResearch ProposalFatimah Fitri Rahmah 1802113657No ratings yet

- Brand Audit - CottononDocument17 pagesBrand Audit - Cottononapi-337554075100% (1)

- A Toolkit For Performance Measures of Public Space PDFDocument9 pagesA Toolkit For Performance Measures of Public Space PDFParamitha agustinNo ratings yet

- King V HernaezDocument2 pagesKing V HernaezCarissa CruzNo ratings yet

- Running Head: Porter'S Five Forces of Target Corp. 1Document10 pagesRunning Head: Porter'S Five Forces of Target Corp. 1debjyoti77No ratings yet

- D.light ChannelDocument4 pagesD.light ChannelKshitijNo ratings yet

- Stiff Them!: Your Guide to Paying Zero Dollars to the IRS, Student Loans, Credit Cards, Medical Bills, and MoreFrom EverandStiff Them!: Your Guide to Paying Zero Dollars to the IRS, Student Loans, Credit Cards, Medical Bills, and MoreNo ratings yet

- The Everything Kids' Money Book: Earn it, save it, and watch it grow!From EverandThe Everything Kids' Money Book: Earn it, save it, and watch it grow!No ratings yet

- The Best Credit Repair Manual Ever WrittenFrom EverandThe Best Credit Repair Manual Ever WrittenRating: 5 out of 5 stars5/5 (32)

- Free & Clear, Standing & Quiet Title: 11 Possible Ways to Get Rid of Your MortgageFrom EverandFree & Clear, Standing & Quiet Title: 11 Possible Ways to Get Rid of Your MortgageRating: 2 out of 5 stars2/5 (3)

- Legal Words You Should Know: Over 1,000 Essential Terms to Understand Contracts, Wills, and the Legal SystemFrom EverandLegal Words You Should Know: Over 1,000 Essential Terms to Understand Contracts, Wills, and the Legal SystemRating: 4 out of 5 stars4/5 (16)

- The Everything Guide to Buying Foreclosures: Learn how to make money by buying and selling foreclosed propertiesFrom EverandThe Everything Guide to Buying Foreclosures: Learn how to make money by buying and selling foreclosed propertiesRating: 5 out of 5 stars5/5 (2)

- All You Need to Know About Payday LoansFrom EverandAll You Need to Know About Payday LoansRating: 5 out of 5 stars5/5 (1)

- 101 Things Everyone Should Know About Economics: A Down and Dirty Guide to Everything from Securities and Derivatives to Interest Rates and Hedge Funds - And What They Mean For YouFrom Everand101 Things Everyone Should Know About Economics: A Down and Dirty Guide to Everything from Securities and Derivatives to Interest Rates and Hedge Funds - And What They Mean For YouRating: 4.5 out of 5 stars4.5/5 (13)

- The Inside Guide to Funding Real Estate Investments: How to Get the Money You Need for the Property You WantFrom EverandThe Inside Guide to Funding Real Estate Investments: How to Get the Money You Need for the Property You WantRating: 4 out of 5 stars4/5 (1)

- Credit Repair Guide: How to Fix Credit Score and Remove Negatives From Credit ReportFrom EverandCredit Repair Guide: How to Fix Credit Score and Remove Negatives From Credit ReportRating: 5 out of 5 stars5/5 (5)

- The Making of a Market: Credit, Henequen, and Notaries in Yucatán, 1850–1900From EverandThe Making of a Market: Credit, Henequen, and Notaries in Yucatán, 1850–1900No ratings yet

- Debt 101: From Interest Rates and Credit Scores to Student Loans and Debt Payoff Strategies, an Essential Primer on Managing DebtFrom EverandDebt 101: From Interest Rates and Credit Scores to Student Loans and Debt Payoff Strategies, an Essential Primer on Managing DebtRating: 4 out of 5 stars4/5 (3)

- One-Month Money: Why money ruins our economy - and how reinventing it could end unemployment and inflation foreverFrom EverandOne-Month Money: Why money ruins our economy - and how reinventing it could end unemployment and inflation foreverNo ratings yet

- The Dividend Investor: A practical guide to building a share portfolio designed to maximise incomeFrom EverandThe Dividend Investor: A practical guide to building a share portfolio designed to maximise incomeNo ratings yet

- How to Get Rid of Your Unwanted Debt: A Litigation Attorney Representing Homeowners, Credit Card Holders & OthersFrom EverandHow to Get Rid of Your Unwanted Debt: A Litigation Attorney Representing Homeowners, Credit Card Holders & OthersRating: 3 out of 5 stars3/5 (1)

- How to Use the Equity in Your Home or Business Today to Invest for TomorrowFrom EverandHow to Use the Equity in Your Home or Business Today to Invest for TomorrowRating: 4.5 out of 5 stars4.5/5 (4)

- Understanding Credit Derivatives and Related InstrumentsFrom EverandUnderstanding Credit Derivatives and Related InstrumentsRating: 4.5 out of 5 stars4.5/5 (2)

- The Guide to Getting Paid: Weed Out Bad Paying Customers, Collect on Past Due Balances, and Avoid Bad DebtFrom EverandThe Guide to Getting Paid: Weed Out Bad Paying Customers, Collect on Past Due Balances, and Avoid Bad DebtNo ratings yet