You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Sunace International MGT Services Inc. vs. NLRCDocument4 pagesSunace International MGT Services Inc. vs. NLRCcharmssatellNo ratings yet

- (Consti) Umali Vs GuingonaDocument1 page(Consti) Umali Vs GuingonaAquino, JPNo ratings yet

- Complaint For Sum of MoneyDocument3 pagesComplaint For Sum of MoneyLudica Oja0% (1)

- Paera Vs People of The Philippines G.R. No. 181626 May 30, 2011Document2 pagesPaera Vs People of The Philippines G.R. No. 181626 May 30, 2011Marlouis U. Planas100% (1)

- Ocampo V PeopleDocument1 pageOcampo V PeopleRabelais MedinaNo ratings yet

- Miranda, Jr. vs. Alvarez, Sr. DigestDocument4 pagesMiranda, Jr. vs. Alvarez, Sr. DigestEmir MendozaNo ratings yet

- 29 Dela Cruz V People (Flores)Document3 pages29 Dela Cruz V People (Flores)Erielle Robyn Tan OngchanNo ratings yet

- LAW 116 - Francisco v. Boiser (G.R. No. 137677)Document2 pagesLAW 116 - Francisco v. Boiser (G.R. No. 137677)Aaron Cade Carino0% (1)

- McCulloch v. MarylandDocument2 pagesMcCulloch v. MarylandRichy2643No ratings yet

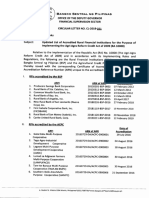

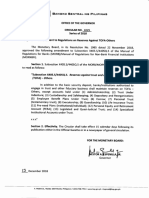

- Bangko NG: Sentral NODocument5 pagesBangko NG: Sentral NOGilbertGalopeNo ratings yet

- Barueko Serurnal Pn-Tptnas: of ofDocument1 pageBarueko Serurnal Pn-Tptnas: of ofGilbertGalopeNo ratings yet

- Bangko NG: Sentral PilipinasDocument10 pagesBangko NG: Sentral PilipinasGilbertGalopeNo ratings yet

- Bangko NG: Sentral Pilipinas Circular Series 2O2Document3 pagesBangko NG: Sentral Pilipinas Circular Series 2O2GilbertGalopeNo ratings yet

- Sentnal Pilipinas: EianokoDocument3 pagesSentnal Pilipinas: EianokoGilbertGalopeNo ratings yet

- CL 033Document1 pageCL 033GilbertGalopeNo ratings yet

- CL 041Document1 pageCL 041GilbertGalopeNo ratings yet

- M 016Document1 pageM 016GilbertGalopeNo ratings yet

- Survivorship Agreement PDFDocument1 pageSurvivorship Agreement PDFGilbertGalopeNo ratings yet

- Philippine Financial Reporting Standards 9 Financial InstrumentsDocument15 pagesPhilippine Financial Reporting Standards 9 Financial InstrumentsGilbertGalopeNo ratings yet

- CL 031Document3 pagesCL 031GilbertGalopeNo ratings yet

- In Its: Bangko PilipinasDocument3 pagesIn Its: Bangko PilipinasGilbertGalopeNo ratings yet

- Sentral Pilipinas: LLL TiquidityDocument10 pagesSentral Pilipinas: LLL TiquidityGilbertGalopeNo ratings yet

- Bexero: Serurnal No PlulptnnsDocument6 pagesBexero: Serurnal No PlulptnnsGilbertGalopeNo ratings yet

- Senrnal: P!L!PinasDocument4 pagesSenrnal: P!L!PinasGilbertGalopeNo ratings yet

- Senrnll: SubjectDocument1 pageSenrnll: SubjectGilbertGalopeNo ratings yet

- CL 019Document1 pageCL 019GilbertGalopeNo ratings yet

- Legal Counseling-Final GiboDocument29 pagesLegal Counseling-Final GiboGilbertGalopeNo ratings yet

- To Of: SenrnalDocument17 pagesTo Of: SenrnalGilbertGalopeNo ratings yet

- cl058 PDFDocument1 pagecl058 PDFGilbertGalopeNo ratings yet

- C 1011Document32 pagesC 1011GilbertGalopeNo ratings yet

- Eianeko Sentral No: SubjectDocument1 pageEianeko Sentral No: SubjectGilbertGalopeNo ratings yet

- Senrnnl: BeruoxoDocument3 pagesSenrnnl: BeruoxoGilbertGalopeNo ratings yet

- Soc LAWDocument1 pageSoc LAWGilbertGalopeNo ratings yet

- CL 058Document1 pageCL 058GilbertGalopeNo ratings yet

- Remedial Law ReviewDocument1 pageRemedial Law ReviewGilbertGalopeNo ratings yet

- CL 058Document1 pageCL 058GilbertGalopeNo ratings yet

- Soc LAWDocument1 pageSoc LAWGilbertGalopeNo ratings yet

- BSP Memorandum 2018-21Document8 pagesBSP Memorandum 2018-21Maya Julieta Catacutan-EstabilloNo ratings yet

- Krivenko v. Register of DeedDocument6 pagesKrivenko v. Register of DeedSecret BookNo ratings yet

- Benjamin Abraham Indictment Press ReleaseDocument2 pagesBenjamin Abraham Indictment Press ReleasestprepsNo ratings yet

- Course Outline Ateneo Public Corporations 2019Document2 pagesCourse Outline Ateneo Public Corporations 2019Malcolm Cruz100% (1)

- ISLAWDocument4 pagesISLAWJay RoqueNo ratings yet

- Article One of The United States ConstitutionDocument39 pagesArticle One of The United States ConstitutionnelsonNo ratings yet

- Bibliography On Pardoning Powers of President in India: Constitutional ApectsDocument6 pagesBibliography On Pardoning Powers of President in India: Constitutional ApectsGowind TulsheNo ratings yet

- Family Courts Rules 1988Document15 pagesFamily Courts Rules 1988ashok203No ratings yet

- Service Law ProjectDocument3 pagesService Law ProjectPavitra ShivhareNo ratings yet

- RA-043534 - PROFESSIONAL TEACHER - Secondary (TLE) - Catarman, Northern Samar - 9-2019 PDFDocument24 pagesRA-043534 - PROFESSIONAL TEACHER - Secondary (TLE) - Catarman, Northern Samar - 9-2019 PDFPhilBoardResultsNo ratings yet

- Features of Indian ConstiDocument7 pagesFeatures of Indian ConstiMankeert NarangNo ratings yet

- AWOL, SC DecisionsDocument55 pagesAWOL, SC DecisionsMelencio Silverio FaustinoNo ratings yet

- 01 Vinzons-Chato V NatividadDocument7 pages01 Vinzons-Chato V NatividadanneNo ratings yet

- F. Recording SettlementDocument4 pagesF. Recording SettlementCharlene ChawNo ratings yet

- India Delhi High Court Grants Injunction To Gillette India Ltd. Against Reckitt Benckiser in A Suit For DisparagementDocument4 pagesIndia Delhi High Court Grants Injunction To Gillette India Ltd. Against Reckitt Benckiser in A Suit For Disparagementdiksha chandraNo ratings yet

- Legal Profession Group Assignment September 3 2019Document6 pagesLegal Profession Group Assignment September 3 2019Marco RenaciaNo ratings yet

- Vda. de Manalo vs. Court of AppealsDocument2 pagesVda. de Manalo vs. Court of AppealsMarc VirtucioNo ratings yet

- (No. 5480. March 21, 1910.) Ricardo Lopez Et Al.Document8 pages(No. 5480. March 21, 1910.) Ricardo Lopez Et Al.Jenny ButacanNo ratings yet

- Cawad Vs Abad PDFDocument4 pagesCawad Vs Abad PDFMarj BaquialNo ratings yet

- F I R - Vague AllegationsDocument3 pagesF I R - Vague AllegationsPrasad100% (1)

- Koleksi Kes-Kes Mahkamah AzmanDocument160 pagesKoleksi Kes-Kes Mahkamah AzmanAZMAN100% (20)

- Integrity in Administration: Ombudsman in Sweden, Lokayukta in States in IndiaDocument10 pagesIntegrity in Administration: Ombudsman in Sweden, Lokayukta in States in IndiaYamini BishtNo ratings yet