You might also like

- Indiareit Apartment FundDocument18 pagesIndiareit Apartment FundSandeep BorseNo ratings yet

- Indiareit Domestic Fund IV PresentationDocument28 pagesIndiareit Domestic Fund IV PresentationChetan Mukhija100% (1)

- ATHAMUS Venture - Picthbook-DealsDocument45 pagesATHAMUS Venture - Picthbook-DealsAravind SankaranNo ratings yet

- Fund of FundsDocument4 pagesFund of FundsparveenbariNo ratings yet

- Fund Formation Attracting Global InvestorsDocument82 pagesFund Formation Attracting Global InvestorssandipktNo ratings yet

- HWVP Fund VII LP MemoDocument26 pagesHWVP Fund VII LP MemobytemealNo ratings yet

- Sequoia Capital India FinalDocument14 pagesSequoia Capital India FinalPallavi TirlotkarNo ratings yet

- Private Debt Presentation - Edl - June 2019Document23 pagesPrivate Debt Presentation - Edl - June 2019api-276349208No ratings yet

- Top Performing Venture Capital FundsDocument4 pagesTop Performing Venture Capital FundsLeon P.No ratings yet

- NBFCDocument24 pagesNBFCmanishNo ratings yet

- Benchmark Report For India AIFs 2022Document7 pagesBenchmark Report For India AIFs 2022Apurva ChamariaNo ratings yet

- Guide-to-Venture-Capital IVA PDFDocument90 pagesGuide-to-Venture-Capital IVA PDFNaveen AwasthiNo ratings yet

- ASKWA Corporate Presentation - Version 9 - April 2019Document25 pagesASKWA Corporate Presentation - Version 9 - April 2019Anonymous bdUhUNm7J100% (1)

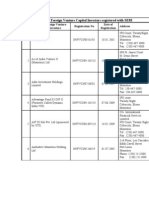

- A-List of Foreign Venture Capital Investors Registered With SEBIDocument24 pagesA-List of Foreign Venture Capital Investors Registered With SEBIVipul ParekhNo ratings yet

- Venture Investing - Rules of SuccessDocument100 pagesVenture Investing - Rules of SuccessSrikrishna Sharma KashyapNo ratings yet

- Rohan Termsheet Kotak FinalDocument4 pagesRohan Termsheet Kotak FinalVidya AdsuleNo ratings yet

- Ey Evolution of Private Credit in IndiaDocument44 pagesEy Evolution of Private Credit in IndiaHimanshu MehtaNo ratings yet

- Ebook Top 58 Venture Capital Firms PDFDocument61 pagesEbook Top 58 Venture Capital Firms PDFPratyutpanna DasNo ratings yet

- Wealth Creation 2008 - 13Document52 pagesWealth Creation 2008 - 13Pratik JoshteNo ratings yet

- Pantera IGS Fund PresentationDocument16 pagesPantera IGS Fund PresentationIrakli NinuaNo ratings yet

- Investment Proposal (Project) Application Form: C Ompany ProfileDocument3 pagesInvestment Proposal (Project) Application Form: C Ompany ProfilenabawiNo ratings yet

- List of VCFsDocument3 pagesList of VCFspoddar_ruchitaNo ratings yet

- TechStars Bridge Term Sheet1Document3 pagesTechStars Bridge Term Sheet1Marius AngaraNo ratings yet

- Blume - VCDocument38 pagesBlume - VCArjun VaradrajNo ratings yet

- LABF - Fund of FundsDocument6 pagesLABF - Fund of FundsdavidsirotaNo ratings yet

- Neo Special Credit Fund Talking Points 2pg RevDocument2 pagesNeo Special Credit Fund Talking Points 2pg RevDrupad N DivyaNo ratings yet

- Zodius Capital II Fund Launch 070414Document2 pagesZodius Capital II Fund Launch 070414avendusNo ratings yet

- YC Seed Deck TemplateDocument11 pagesYC Seed Deck TemplateRoaldDahlNo ratings yet

- Demystifying Venture Capital Economics - Part 1Document9 pagesDemystifying Venture Capital Economics - Part 1KarnYoNo ratings yet

- A Guide To Venture Capital in The Middle East and North Africa1Document40 pagesA Guide To Venture Capital in The Middle East and North Africa1moemikatiNo ratings yet

- CB Insights The Future InvestingDocument26 pagesCB Insights The Future InvestingAlisaNo ratings yet

- AIF DataDocument32 pagesAIF DataYASH CHAUDHARYNo ratings yet

- KKR-Tearsheet KIO 20171231 PDFDocument3 pagesKKR-Tearsheet KIO 20171231 PDFBrianNo ratings yet

- Private Equity Funds Performance EvaluationDocument5 pagesPrivate Equity Funds Performance Evaluationgnachev_4100% (1)

- Kotak International REIT PresentationDocument27 pagesKotak International REIT PresentationMarwan AbuzayanNo ratings yet

- GKC Projects Limited: Enterprise Valuation ReportDocument31 pagesGKC Projects Limited: Enterprise Valuation Reportcrmc999No ratings yet

- Introduction To Venture CapitalDocument5 pagesIntroduction To Venture CapitalKanya RetnoNo ratings yet

- Capital Today FINAL PPMDocument77 pagesCapital Today FINAL PPMAshish AgrawalNo ratings yet

- List OF HEDGE FUNDS FROM ODPDocument14 pagesList OF HEDGE FUNDS FROM ODPBiswa1989No ratings yet

- JAZZ Sellside MA PitchbookDocument47 pagesJAZZ Sellside MA PitchbookBernardo FusatoNo ratings yet

- Blackstone Group Annual Report No. 1Document80 pagesBlackstone Group Annual Report No. 1Giovanni GrazianoNo ratings yet

- KKR Private Equity Investors, L.P. Annual Report 2008Document131 pagesKKR Private Equity Investors, L.P. Annual Report 2008AsiaBuyoutsNo ratings yet

- Global Farmland Fund - EGB TeaserDocument6 pagesGlobal Farmland Fund - EGB TeaseragrachinaNo ratings yet

- A91 Partners JDDocument2 pagesA91 Partners JDJohn DoeNo ratings yet

- Pariksha - Investment MemoDocument4 pagesPariksha - Investment MemoRashi KohliNo ratings yet

- Loi Sha009 GicDocument2 pagesLoi Sha009 GicgreenindiacargoplNo ratings yet

- 3cfff0f2 1cfe 4a1e 91ed 7c5ce06f11d6 Preqin Investor Outlook Alternative Assets H2 2021Document29 pages3cfff0f2 1cfe 4a1e 91ed 7c5ce06f11d6 Preqin Investor Outlook Alternative Assets H2 2021UDITA MEHTANo ratings yet

- List of Investors - Short TermDocument12 pagesList of Investors - Short Termrshah11508No ratings yet

- Venture CapitalDocument71 pagesVenture CapitalSmruti VasavadaNo ratings yet

- Investment Banks: Main Activities and UnitsDocument8 pagesInvestment Banks: Main Activities and UnitsatifqadriNo ratings yet

- Avendus India Opportunities Fund IIIDocument12 pagesAvendus India Opportunities Fund IIIhiteshaNo ratings yet

- Landmark Capital - Fund BrochureDocument37 pagesLandmark Capital - Fund BrochureSandeep BorseNo ratings yet

- Private Placement Subscription AgreementDocument11 pagesPrivate Placement Subscription Agreementalvah100% (3)

- Standard Chartered Wealth Management PackDocument35 pagesStandard Chartered Wealth Management PackAnura BirdNo ratings yet

- Incred AIFDocument20 pagesIncred AIFvarunNo ratings yet

- FAB Analyst and Investor Day BiosDocument17 pagesFAB Analyst and Investor Day BioskhuramrajpootNo ratings yet

- Global Family Office Report 2023Document66 pagesGlobal Family Office Report 2023NeoNo ratings yet

- Beijing Capital Growth Fund - PPMDocument111 pagesBeijing Capital Growth Fund - PPMRangaraja IyengarNo ratings yet

- Characteristics: 1. Debt Financing: A. Bank LoansDocument6 pagesCharacteristics: 1. Debt Financing: A. Bank LoansIDEAL DRAGONSNo ratings yet

- Bain Report India Real EstateDocument40 pagesBain Report India Real Estatesudhansu_777No ratings yet

- Developing The 21st Century LeaderDocument32 pagesDeveloping The 21st Century LeaderMaRa MaRoulita100% (1)

- Final PPT of Unilever PDFDocument55 pagesFinal PPT of Unilever PDFFany KartikaNo ratings yet

- Polytechnic University of The PhilippinesDocument12 pagesPolytechnic University of The PhilippinesKyla Dane P. Prado0% (1)

- V Některých Případech Je Potřeba Vyměnit Čip Z Originálního DiskuDocument2 pagesV Některých Případech Je Potřeba Vyměnit Čip Z Originálního DiskuovertopNo ratings yet

- ENR Top 500 2020Document64 pagesENR Top 500 2020ApaxATONo ratings yet

- Chapter Two Small Business ManagementDocument28 pagesChapter Two Small Business ManagementBekeleNo ratings yet

- Praktek Value Chain Analysis Di PT. Aneka TambangDocument9 pagesPraktek Value Chain Analysis Di PT. Aneka TambangEndah RiwayatunNo ratings yet

- Wheel of RetailingDocument6 pagesWheel of RetailingjaijohnkNo ratings yet

- Nigerian Banks: Resilience Built inDocument52 pagesNigerian Banks: Resilience Built inapanisile14142No ratings yet

- Metis Coal Report Brochure Full May 1Document8 pagesMetis Coal Report Brochure Full May 1arorakgarima100% (1)

- A Study of Merger and Acquisition in Indian Banking SectorDocument81 pagesA Study of Merger and Acquisition in Indian Banking SectorChinmay VangeNo ratings yet

- Corporate DiversificationDocument24 pagesCorporate DiversificationPatrick Joshua BreisNo ratings yet

- Ge S Two Decade Transformation Jack Welch S LeadershipDocument27 pagesGe S Two Decade Transformation Jack Welch S LeadershipMohsinRaza100% (2)

- Sika Media Release - MBCC - EN - 11nov21Document4 pagesSika Media Release - MBCC - EN - 11nov21Gabriel LimNo ratings yet

- EOS - Disney Pixar - Group 7Document9 pagesEOS - Disney Pixar - Group 7Amod VelingkarNo ratings yet

- Final ExaminationDocument3 pagesFinal ExaminationZia SmithNo ratings yet

- 2013 Restaurant Industry ReportDocument28 pages2013 Restaurant Industry Report10TAMBKANo ratings yet

- EVENTMANAGEMENTDocument5 pagesEVENTMANAGEMENTmichelleahmedantiqueeleganceNo ratings yet

- Betty Crocker ReportDocument6 pagesBetty Crocker Reportapi-260096278No ratings yet

- Service Marketing of Icici BankDocument41 pagesService Marketing of Icici BankIshan VyasNo ratings yet

- Economic Characteristics of The Air Transportation and Included OrganizationsDocument4 pagesEconomic Characteristics of The Air Transportation and Included OrganizationsVence Dela Tonga PortesNo ratings yet

- China Hotel IndustryDocument10 pagesChina Hotel IndustryProf PaulaNo ratings yet

- FICODocument114 pagesFICOgnanshettyNo ratings yet

- SEC v. National SecuritiesDocument2 pagesSEC v. National Securitiesruth_pedro_2No ratings yet

- G.R. No. 167519 January 14, 2015 THE Wellex Group, INC., Petitioner, U-LAND AIRLINES, CO., LTD., RespondentDocument44 pagesG.R. No. 167519 January 14, 2015 THE Wellex Group, INC., Petitioner, U-LAND AIRLINES, CO., LTD., RespondentAnonymous EWc8jygsNo ratings yet

- Strategic MNGT IMT-56Document71 pagesStrategic MNGT IMT-56Deepak MahajanNo ratings yet

- Pitfall of Parenting Mature CompanyDocument12 pagesPitfall of Parenting Mature Companyrohitboy123No ratings yet

- AcctTheory - Chap06 Structure of Accounting Theory (Belkaoui)Document29 pagesAcctTheory - Chap06 Structure of Accounting Theory (Belkaoui)Aurora AzzahraNo ratings yet

- Merger & Acquisitions On Tata Steel Ltd. & CorusDocument28 pagesMerger & Acquisitions On Tata Steel Ltd. & CorusFarhan100% (2)

- Cracking The Growth Code in ChemicalsDocument7 pagesCracking The Growth Code in ChemicalsLuca EgidiNo ratings yet