Professional Documents

Culture Documents

New Accounting Standards - Kotak - Jun 2016

Uploaded by

vishmittCopyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

New Accounting Standards - Kotak - Jun 2016

Uploaded by

vishmittCopyright:

Available Formats

INDIA

Strategy

India

JUNE 29, 2016

NEW RELEASE

BSE-30: 26,740

New (accounting standards) and old (valuations). It is hard to get excited by

accounting in general and we would advise investors the same as Indian companies

transition to the new accounting standard (Indian Accounting StandardsInd-AS) from

April 1, 2016. Reported numbers for revenues, EBITDA and EPS may look different in

several cases versus those prepared under the old accounting standard or versus Street

estimates. However, cash flows and valuations will not change materially.

Adoption of Ind-AS from 1QFY17

Indian companies will have to gradually adopt the revised Indian Accounting Standards (Ind-AS)

from April 1, 2016. Companies (listed or unlisted) with a net worth of `5 bn or more will move

to Ind-AS from April 1, 2016, all listed companies from April 1, 2017 and unlisted companies

with a net worth of `2.5 bn or more from April 1, 2017. Banks and NBFCs will adopt the new

accounting standards from April 1, 2018.

Revenues, EBITDA and EPS will be different in several cases; cash flows will not change

We discuss differences between Ind-AS and the previous accounting standard (Indian GAAP)

across several broad areas in Exhibit 1 for companies under our coverage. Revenues, EBITDA

and EPS may look different in several cases under Ind-AS compared to IGAAP. Companies

adopting Ind-AS from April 1, 2016 will have to mandatorily provide comparative financial

statements prepared under Ind-AS for the previous year (FY2016) and balance sheet (opening

Ind-AS balance sheet) for FY2015 also.

Revenues (excise duty), EBITDA (JV accounting), interest costs and EPS (treasury shares) different

QUICK NUMBERS

Companies with net

worth of `5 bn or

more to apply

Ind-AS from

April 1, 2016

Smaller companies

and banks & NBFCs

will apply Ind-AS

from April 1, 2017

and April 1, 2018

respectively

We highlight a few broad areas of changes between the new and old standards and discuss the

more arcane stuff in the analysis of individual companies in the exhibit. (1) Revenues will be

reported gross of excise duty and net of discounts and incentives, which will result in optically

higher revenues and lower EBITDA margin. (2) JV accounting (subject to the issue of control)

will move to equity accounting rather than consolidation, which would depress EBITDA; net

profits will be unchanged. (3) Interest rate on certain types of instruments will be charged as

effective interest rate and will include coupon rate, redemption premium and issue expenses.

(4) Treasury shares will need to be eliminated, which would increase the reported EPS of certain

companies; net profits will be unchanged.

Valuation methodologies already largely capture the likely changes to earnings

We would highlight that the Street is already capturing some of the changes under Ind-AS in

valuations. For example, in the case of companies with treasury shares (BPCL, IOCL, RIL, UNSP

to name a few), the Street already excludes treasury shares (as is required under Ind-AS) to

compute the fair valuation of companies on `/share basis or adds back the value of the treasury

shares in the SoTP valuation. Similarly, we add back over burden removal (OBR, a portion of

which will not be required to be provided under Ind-AS and will optically boost Coal Indias EPS)

to the reported EBITDA of Coal India while computing its fair value. We would note that cash

flows and valuations of the companies should not change simply because of reported numbers

being different versus those under IGAAP or versus Street estimates based on IGAAP.

Sanjeev Prasad

sanjeev.prasad@kotak.com

Mumbai: +91-22-4336-0830

Akhilesh Tilotia

akhilesh.tilotia@kotak.com

Mumbai: +91-22-4336-0897

Sunita Baldawa

sunita.baldawa@kotak.com

Mumbai: +91-22-4336-0896

Kotak Institutional Equities Research

kotak.research@kotak.com

Mumbai: +91-22-4336-0000

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

India

Strategy

Additional disclosures may be useful

In our view, additional disclosures from companies or reconciliation between the two

accounting standards would be useful to appreciate the changes better. We note that

companies will have to provide comparative interim financial statements (not required under

Ind-AS but as per listing agreements), which should help understand the financials of the

two periods (current and year ago) if both are prepared under the same standard (Ind-AS).

If an entity follows Ind-AS for preparing interim financial reports, interim reports would

include (1) balance sheet at the end of the current interim period and a comparative balance

sheet as of the end of the immediately preceding financial year, (2) statements of profit and

loss for the current interim period and cumulatively for the financial year to date with

comparative statements of profit and loss of the comparable interim periods (both current

and year-to-date) of the immediately preceding financial year (1QFY16 when companies

report under Ind-AS in 1QFY17) and (3) statement of cash flows cumulatively for the current

financial year to date with a comparative statement for the comparable year-to-date period

of the immediately preceding financial year (1QFY16).

Reporting of revenues (Ind-AS 18)

On reporting of revenues, it would be helpful if companies were to report excise duty

(amount) separately. Excise duty is considered as part of revenues under Ind-AS 18 based on

our discussions with and inputs from companies and tax firms. Excise duty would thus be

included in both revenues and cost of materials consumed. However, this would not have

any impact on EBITDA or PAT. It may distort reported EBITDA margin though, as historically

the Street has computed EBITDA margin on net revenues/sales (excluding excise duty).

If companies were to report excise duty sales separately, it would not really matter as it

would be simple enough to compute net revenues/sales (net of excise duty) so that revenues

are comparable with historical revenues/sales. Under Ind-AS 18, other taxes such as sales tax

or service tax would not be included in revenues as was the case historically as companies

act as agents on behalf of the government in the case of sales or service tax; historical

sales/revenues excluded other taxes (taxes other than excise duty).

We reproduce the relevant sections from Ind-AS 18, which covers revenue and Ind-115,

which covers revenue from contract with customers. We note that the government has not

yet notified Ind-AS 115. We assume that all taxes would be excluded from revenues as and

when GST is implemented in the country.

Ind-AS 18

Definitions

7 The following terms are used in this standard with the meanings specified:

Revenue is the gross inflow of economic benefits during the period arising in the course of

the ordinary activities of an entity when those inflows result in increases in equity, other

than increases relating to contributions from equity participants.

Fair value is the amount for which an asset could be exchanged, or a liability settled,

between knowledgeable, willing parties in an arms length transaction.

8 Revenue includes only the gross inflows of economic benefits received and receivable by

the entity on its own account. Amounts collected on behalf of third parties such as

sales taxes, goods and services taxes and value-added taxes are not economic

benefits which flow to the entity and do not result in increases in equity. Therefore,

they are excluded from revenue. Similarly, in an agency relationship, the gross inflows of

economic benefits include amounts collected on behalf of the principal and which do not

result in increases in equity for the entity. The amounts collected on behalf of the principal

are not revenue. Instead, revenue is the amount of commission.

KOTAK INSTITUTIONAL EQUITIES RESEARCH

Strategy

India

Ind-AS 115

109AA An entity shall present separately the amount of excise duty included in the revenue

recognized in the statement of profit and loss.

Treatment of outsourcing, contract manufacturing and take-or-pay contracts

as leases (Ind-AS 17)

We note that several Indian companies, particularly in the consumer staples and durables

business, procure their finished goods from suppliers, many of whom are exclusive to the

companies. It is possible that such arrangements between the purchaser (consumer staple or

durable company) and the seller (manufacturing entity or bottler) may be treated as leases

under Ind-AS 17, which would complicate the reporting of costs for the companies (lease

payments versus cost of goods purchased).

There are two principles for determining whether an arrangement qualifies as a lease (and

we reproduce the same verbatim from the standard)(1) fulfillment of the arrangement is

dependent on the use of a specific asset or assets (the asset); and (2) the arrangement

conveys a right to use the asset.

The first principle would suggest elements of a lease since the supplier has no other use for

the specific asset/(s) other than to provide goods as part of the arrangement to the

purchaser. We reproduce the relevant paragraphs from the standard below.

(a) Although a specific asset may be explicitly identified in an arrangement, it is not the

subject of a lease if fulfillment of the arrangement is not dependent on the use of the

specified asset. For example, if the supplier is obliged to deliver a specified quantity of

goods or services and has the right and ability to provide those goods or services using

other assets not specified in the arrangement, then fulfillment of the arrangement is not

dependent on the specified asset and the arrangement does not contain a lease.

A warranty obligation that permits or requires the substitution of the same or similar

assets when the specified asset is not operating properly does not preclude lease

treatment. In addition, a contractual provision (contingent or otherwise) permitting or

requiring the supplier to substitute other assets for any reason on or after a specified

date does not preclude lease treatment before the date of substitution.

(b) An asset has been implicitly specified if, for example, the supplier owns or leases only

one asset with which to fulfill the obligation and it is not economically feasible or

practicable for the supplier to perform its obligation through the use of alternative assets.

The second one regarding whether an arrangement conveys the right to use the asset or in

other words will depend on whether the arrangement conveys to the purchaser (lessee), the

right to control the use of the underlying asset/(s). The right to control the use of the

underlying asset is conveyed if any one of the following conditions is met (reproduced

from the standard below):

(a) The purchaser has the ability or right to operate the asset or direct others to operate the

asset in a manner it determines while obtaining or controlling more than an insignificant

amount of the output or other utility of the asset.

(b) The purchaser has the ability or right to control physical access to the underlying asset

while obtaining or controlling more than an insignificant amount of the output or other

utility of the asset.

(c) Facts and circumstances indicate that it is remote that one or more parties other

than the purchaser will take more than an insignificant amount of the output or

other utility that will be produced or generated by the asset during the term of the

arrangement, and the price that the purchaser will pay for the output is neither

contractually fixed per unit of output nor equal to the current market price per

unit of output as of the time of delivery of the output.

KOTAK INSTITUTIONAL EQUITIES RESEARCH

India

Strategy

Exhibit 1: 1QFY17 results may see some positive and negative surprises on reported numbers

Impact of Ind-AS on top companies in our universe

Company

Ticker

Implications

Automobiles

Amara Raja Batteries

AMRJ IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

Ashok Leyland

AL IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

Bajaj Auto

BJAUT IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Returns from investment in fixed maturity plans (current investment of Rs60-70 bn) would be accounted on accrual basis as

compared to cash basis currently. Mark-to-market forex gains on unrealized hedges will flow through directly to balance sheet

instead of to P&L currently. This would reduce volatility in other income; in particular, other income would increase in FY2017

due to significant investment in three-year FMPs.

Bharat Forge

BHFC IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) FX fluctuation impact on loans (taken post FY2016) and other long-term monetary assets/liabilities to be charged to the P&L

(versus being allowed to be capitalized under amended AS11 of IGAAP); this could lead to higher volatility in earnings.

Eicher Motors

EIM IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Returns from investment in fixed maturity plans would be accounted on accrual basis as compared to cash basis currently.

This would reduce volatility in other income; in particular, other income would increase in FY2017 due to significant investment

in three-year FMPs.

(3) ESOP accounting: Fair valuation of ESOP cost and P&L charge is mandatory under Ind-AS; FY2016 PBT would have been

marginally lower if ESOP charges were taken through the P&L.

Exide Industries

EXID IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

Hero Motocorp

HMCL IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Returns from investment in fixed maturity plans would be accounted on accrual basis as compared to cash basis currently.

This would reduce volatility in other income; in particular, other income would increase in FY2017 due to significant investment

in 3-year FMPs.

Mahindra & Mahindra

MM IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Returns from investment in fixed maturity plans would be accounted on accrual basis as compared to cash basis currently.

This would reduce volatility in other income; in particular, other income would increase in FY2017 due to significant investment

in three-year FMPs.

(3) Treasury shares: They are not treated as financials assets under Ind-AS and would need to be adjusted (eliminated) from

equity. Will lead to reduction in net worth and increased RoE (our EPS estimates are already adjusted for this). M&M had 51.8

mn treasury shares at end-FY2016 (8% of equity base).

(4) FX fluctuation impact on loans (taken post FY2016) and other long-term monetary assets/liabilities to be charged to the

P&L (versus being allowed to be capitalized under amended AS11 of IGAAP); this could lead to higher volatility in earnings.

Maruti Suzuki

MSIL IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Returns from investment in fixed maturity plans would be accounted on accrual basis as compared to cash basis currently.

This would reduce volatility in other income; in particular, other income would increase in FY2017 due to significant investment

in three-year FMPs.

Motherson Sumi Systems

MSS IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) FX fluctuation impact on long-term monetary assets/liabilities to be charged to the P&L (versus being allowed to be

capitalized under amended AS11 of IGAAP); this could lead to higher volatility in earnings.

Tata Motors

TTMT IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) FX fluctuation impact on foreign currency loans (taken post FY2016) and other long-term monetary assets/liabilities to be

charged to the P&L (versus being allowed to be capitalized under amended AS11 of IGAAP); this could lead to higher volatility

in earnings.

(3) Factoring of receivables and acceptances from creditors will need to be accounted as debt in the balance sheet. This could

lead to marginal increase in overall borrowings of the company.

TVS Motor

TVSL IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

WABCO India

WIL IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

Source: Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH

Strategy

India

1QFY17 results may see some positive and negative surprises on reported numbers (cont.)

Impact of Ind-AS on top companies in our universe

Company

Ticker

Implications

Cement

ACC

ACC IN Equity

Income statement: (1) Revenues will be reported gross of excise duty and net of discounts/incentives, (2) EBITDA may increase

marginally due to lower charge for long-term provisions (present value accounting), and (3) depreciation may increase if assets

are revalued.

Balance sheet: (1) Net worth may change due to revaluation of PPE, recognition of investments at fair value, (3) fixed assets

may increase due to fair value exercise and classification of capital advances as C-WIP rather than loans and advances, and (3)

current liabilities will change due to lower long-term provisions (present value impact).

Ambuja Cements

ACEM IN Equity

Income statement: (1) Revenues will be reported gross of excise duty and net of discounts/incentives, (2) EBITDA may increase

marginally due to lower charge for long-term provisions (present value accounting), and (3) depreciation may increase if assets

are revalued.

Balance sheet: (1) Net worth may change due to revaluation of PPE, recognition of investments at fair value, (3) fixed assets

may increase due to fair value exercise and classification of capital advances as C-WIP rather than loans and advances, and (3)

current liabilities will change due to lower long-term provisions (present value impact).

Dalmia Bharat

DBEL IN Equity

Income statement: (1) Revenues will be reported gross of excise duty and net of discounts/incentives, (2) EBITDA may increase

marginally due to lower charge for long-term provisions (present value accounting), and (3) depreciation may increase if assets

are revalued.

Balance sheet: (1) Net worth may change due to revaluation of PPE, recognition of investments at fair value, (3) fixed assets

may increase due to fair value exercise and classification of capital advances as C-WIP rather than loans and advances, (3)

current liabilities will change due to lower long-term provisions (present value impact), and (4) increase in debt owing to reclassification of current liabilities into debt.

Grasim Industries

GRASIM IN Equity

Income statement: (1) Revenues will be reported gross of excise duty and net of discounts/incentives, (2) EBITDA may increase

marginally due to lower charge for long-term provisions (present value accounting), (3) depreciation may increase if assets are

revalued, and (4) exclusion of earnings from pulp JVs will impact revenue and EBITDA (revenues of Rs21 bn and EBITDA of Rs2

bn in FY2016), although net income will remain unaffected.

Balance sheet: (1) Net worth may change due to revaluation of PPE, recognition of investments at fair value, (2) fixed assets

may increase due to fair value exercise and classification of capital advances as C-WIP rather than loans and advances, (3)

current liabilities will change due to lower long-term provisions (present value impact), and (4) higher value of investments in

group companies such as Hindalco and Aditya Birla Nuvo.

Shree Cement

SRCM IN Equity

Income statement: (1) Revenues will be gross of revenues and reported net of discounts/incentives, (2) EBITDA may increase

marginally due to lower charge for long-term provisions (present value accounting), and (3) depreciation may increase if assets

are revalued.

Balance sheet: (1) Net worth may change due to revaluation of PPE, recognition of investments at fair value, (3) fixed assets

may increase due to fair value exercise and classification of capital advances as C-WIP rather than loans and advances, and (3)

current liabilities will change due to lower long-term provisions (present value impact).

UltraTech Cement

Income statement: (1) Revenues will be reported gross of excise duty and net of discounts/incentives, (2) EBITDA may increase

UTCEM IN Equity marginally due to lower charge for long-term provisions (present value accounting), and (3) depreciation may increase if assets

are revalued.

Balance sheet: (1) Net worth may change due to revaluation of PPE, recognition of investments at fair value, (2) fixed assets

may increase due to fair value exercise and classification of capital advances as C-WIP rather than loans and advances, and (3)

current liabilities will change due to lower long-term provisions (present value impact).

Consumer products

Asian Paints

APNT IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Fair valuation of marketable investments: APNT invests a good portion (85% at end-FY2015 cash) of its cash in mutual

funds. With fair value (as opposed to the current 'book gain/loss on maturity') accounting, volatility in earnings will come

down.

(3) JV consolidation: Equity accounting instead of proportionate consolidation. Will impact reported revenues and EBITDA with

no impact on EPS.

Britannia Industries

BRIT IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Fair valuation of marketable investments: BRIT invests a good portion (65% at end-FY2015) of its cash in mutual funds.

With fair value (as opposed to the current 'book gain/loss on maturity') accounting, volatility in earnings will come down.

(3) ESOP accounting: Fair valuation of ESOP cost and P&L charge mandatory under Ind-AS; FY2015 PBT would have been

marginally lower if ESOP charges were taken on the P&L.

(4) 'Take-or-pay' contracts or contract manufacturing to be treated as deemed lease under Ind-AS (versus treatment as

purchase transactions under IGAAP). This will mean higher assets on books and lower return ratios. BRIT has a higher share of

outsourced manufacturing than peers.

Colgate-Palmolive (India)

CLGT IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

Dabur India

DABUR IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

GlaxoSmithKline Consumer

SKB IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Actuarial gains/losses to be charged to reserves versus being charged to the P&L currently. Will reduce earnings volatility on

this count.

Source: Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH

India

Strategy

1QFY17 results may see some positive and negative surprises on reported numbers (cont.)

Impact of Ind-AS on top companies in our universe

Company

Ticker

Godrej Consumer Products

GCPL IN Equity

Implications

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) ESOP accounting: Fair valuation of ESOP cost and P&L charge mandatory under Ind-AS; FY2015 PBT would have been 1%

lower if ESOP charges were taken on the P&L.

(3) FX fluctuation impact on long-term monetary assets/liabilities to be charged to the P&L (versus being allowed to be

capitalized under amended AS11 of IGAAP); negative impact on earnings.

Hindustan Unilever

HUVR IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Few non-material reclassification of cost-line items.

(3) Fair valuation of marketable investments; volatility in earnings will come down.

ITC

ITC IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) ESOP accounting: Fair valuation of ESOP cost and P&L charge mandatory under Ind-AS; FY2015 PBT would have been 4%

lower if ESOP charges were taken on the P&L.

Marico

MRCO IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Fair valuation of marketable investments: MRCO invests a good portion (50% at end-FY2015) of its cash in mutual funds.

With fair value (as opposed to the current 'book gain/loss on maturity') accounting, volatility in earnings will come down.

Nestle India

NEST IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Actuarial gains/losses to be charged to reserves versus being charged to the P&L currently. Will reduce earnings volatility on

this count.

(3) 'Take-or-pay' contracts or contract manufacturing could be treated as deemed lease under Ind-AS 17 (versus treatment as

purchase transactions under IGAAP). This will mean higher assets on books and lower return ratios. NEST has a higher share of

outsourced manufacturing than peers.

Page Industries

PAG IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

Pidilite Industries

PIDI IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Fair valuation of marketable investments: PIDI invests a good portion (75% at end-FY2015) of its cash in mutual funds. With

fair value (as opposed to the current 'book gain/loss on maturity') accounting, volatility in earnings will come down.

(3) FX fluctuation impact on long-term monetary assets/liabilities to be charged to the P&L (versus being allowed to be

capitalized under amended AS11 of IGAAP); negative impact on earnings.

Titan Company

TTAN IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Actuarial gains/losses to be charged to reserves versus being charged to the P&L currently. Will reduce earnings volatility on

this count.

United Breweries

UBBL IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Actuarial gains/losses to be charged to reserves versus being charged to the P&L currently. Will reduce earnings volatility on

this count.

(3) 'Take-or-pay' contracts or contract manufacturing could be treated as deemed lease under Ind-AS 17 (versus treatment as

purchase transactions under IGAAP). This will mean higher assets on books and lower return ratios. UBBL has a higher share of

outsourced manufacturing than peers.

United Spirits

UNSP IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Actuarial gains/losses to be charged to reserves versus being charged to the P&L currently. Will reduce earnings volatility on

this count.

(3) 'Take-or-pay' contracts or contract manufacturing could be treated as deemed lease under Ind-AS 17 (versus treatment as

purchase transactions under IGAAP). This will mean higher assets on books and lower return ratios. UNSP has a higher share

of outsourced manufacturing than peers.

(4) Treasury shares: Not treated as financials assets under Ind-AS and would need to be adjusted (eliminated) from equity. Will

lead to reduction in net worth and increase in EPS and RoE. UNSP had 3.46 mn treasury shares at end-FY2015 (2.38% of equity

base).

Source: Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH

Strategy

India

1QFY17 results may see some positive and negative surprises on reported numbers (cont.)

Impact of Ind-AS on top companies in our universe

Company

Ticker

Implications

Energy

BPCL

BPCL IN Equity

(1) BORL JV's financials will be added on the basis of equity method, instead of proportionate consolidation.

(2) Equity investments will have to be shown at fair value on the balance sheet and gains or losses will be accounted in other

comprehensive income.

(3) Treasury shares (67 mn shares or 9.3% of outstanding shares) will be eliminated from equity.

Cairn India

CAIR IN Equity

(1) Returns from FMPs will have to be accounted on accrual basis, instead of being accounted on maturity.

(2) ESOPs have to be accounted at fair valuation; no material impact given sharp correction in stock price.

Castrol India

CSTRL IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

GAIL (India)

GAIL IN Equity

(1) Equity investments will have to be shown at fair value on the balance sheet and gains or losses will be accounted in other

comprehensive income.

HPCL

HPCL IN Equity

(1) HMEL JV's financials will be added on the basis of equity method, instead of proportionate consolidation.

(2) Equity investments will have to be shown at fair value on the balance sheet and gains or losses will be accounted in other

comprehensive income.

IOCL

IOCL IN Equity

(1) Equity investments will have to be shown at fair value on the balance sheet and gains or losses will be accounted in other

comprehensive income.

(2) Treasury shares (31 mn shares or 1.3% of outstanding shares) will be eliminated from equity.

Oil India

OINL IN Equity

(1) Equity investments will have to be shown at fair value on the balance sheet and gains or losses will be accounted in other

comprehensive income.

ONGC

ONGC IN Equity

(1) Equity investments will have to be shown at fair value on the balance sheet and gains or losses will be accounted in other

comprehensive income.

Petronet LNG

PLNG IN Equity

No major change expected.

Reliance Industries

RIL IN Equity

(1) Forex fluctuation on long-term debt (post FY2016) has to be accounted in the P&L, instead of being capitalized in the

balance sheet.

(2) Creditors for capital expenditure may be required to be accounted as debt in the balance sheet.

(3) Treasury shares (292 mn shares or 9% of equity) will be eliminated from equity , which will boost reported EPS.

Industrials

ABB

ABB IN Equity

No major change expected.

BHEL

BHEL IN Equity

(1) There is less clarity on whether deferred debt (around 50% of total receivables) would have to be accounted for using the

time value of money concept or not.

Cummins India

KKC IN Equity

No major change expected.

Havells India

HAVL IN Equity

No major change expected.

L&T

LT IN Equity

(1) JV accounting: Financials that are booked on line-by-line basis now (company's share) will be shown only as proportionate

PAT (equity method of accounting). Revenues, EBITDA, interest and depreciation to be lower. However, there is no impact on

PAT.

(2) ESOP accounting: Fair valuation of ESOP cost and P&L charge mandatory under Ind-AS; no major impact in P&L based on

details shared in FY2015 annual report.

(3) Profit on stake sales in L&T Finance, if any, may be passed through reserve rather than P&L (adjustment between majority

and minority).

Siemens

SIEM IN Equity

No major change expected.

Thermax

TMX IN Equity

No major change expected.

Voltas

VOLT IN Equity

(1) JV accounting: Financials that are booked on line-by-line basis now (company's share) will be shown only as proportionate

PAT (equity method of accounting).

(2) Equity investments, which are neither associates nor subsidiaries, have to be shown as fair value on the balance sheet and

gains or losses to be carried to the P&L; Voltas has investments in Lakshmi Machine Works.

Infrastructure

Adani Port and SEZ

ADSEZ IN Equity

(1) Under Ind-AS, exchange rate differences on long-term foreign currency instruments used for acquisition of long-term assets

are to be recognized in P&L in the period they arise. At present, company adjusts exchange differences arising on

translation/settlement of long-term foreign currency monetary items pertaining to the acquisition of a depreciable asset to the

cost of the asset and depreciates the same over the remaining useful life of the asset.

(2) Under Ind-AS, premium or discount of forward exchange contracts are recognized in the reporting period in which exchange

rates change. At present, the premium or discount arising at the inception of forward exchange contracts is amortized as an

expense/income over the life of the contract.

Container Corporation

CCRI IN Equity

No major change expected.

IRB

IRB IN Equity

(1) Depreciation method would remain revenue-based, though this will also take into account for toll revenues earned in the

construction phase; excess depreciation on this account for past projects to be accounted for in the balance sheet.

(2) Liability against deferred premium payment would be shown as the discounted value and thus, depreciation related to the

corresponding asset would also reduce; excess depreciation on this account for past projects to be accounted for in the

balance sheet.

Sadbhav Engineering

SADE IN Equity

(1) Calculation of effective interest rate for ICD = cash coupon rate + premium redemption + upfront fee.

(2) Construction profit so earned by the road SPV would get shown in the P&L and would increase tax expense. Construction

profit would equal estimated toll revenues less operating expenses less project cost. Grant to also be accounted in the P&L.

(3) Subordinate debt (typically zero debt) would be discounted to present value and rest of the investment would be termed

other equity. As interest income gets earned, the tax expense would increase.

Source: Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH

India

Strategy

1QFY17 results may see some positive and negative surprises on reported numbers (cont.)

Impact of Ind-AS on top companies in our universe

Company

Internet

Ticker

Info Edge

INFOE IN Equity

Implications

(1) Marginal deferment of revenue in case of products where revenue was earlier recognized upfront, but post Ind-AS would

need to be accounted over the life of the contract.

(2) ESOP accounting using fair value method under Ind-AS (intrinsic method earlier). FY2016 net profit would have been lower

by Rs178 mn (~12% impact). Future employee costs on account of ESOP costs would vary on a quarterly basis depending on

stock price movement.

(3) There is now a case for Zomato not being consolidated: INFOEs stake in Zomato is less than 50% (if convertible shares

are included), and INFOE does not control Zomato (there are other investors as well). The company may have to report on

equity accounting method under Ind-AS.

Just Dial

JUST IN Equity

(1) JD Omni is currently sold for an upfront fee and a monthly recurring fee. Just Dial may need to account for the upfront fee

over the life of the customer, and revenue recognition from Omni may hence get deferred. Company is trying out various

pricing options for Omni, with reduced upfront fee, and hence impact to P&L may not be much. Omni contributes ~7% to our

FY2017E revenues.

(2) ESOP accounting: Company may cancel and re-issue ESOPs granted in the past, which may lead to some write-backs due to

fair value accounting (as stock price has declined considerably).

Media

DishTV

DITV IN Equity

(1) Revenue recognition. Dish TV recognizes entire activation income upfront. Under Ind-AS, the company may have to

recognize it over useful life of the set-top box. This change could impact revenues and EBITDA by about Rs1.75-2 bn in

FY2017E (about 15% EBITDA impact) assuming useful life of STB of 5 years. We note that, the impact will moderate over the

medium term as unamortized activation will get recognized in future years. (2) STBs are depreciated over 5 years period. Any

change in useful life under Ind-AS could impact depreciation. (3) Forex impact. Forex impact associated with foreign currency

debt will be routed through P&L under Ind-AS as against BS at present. Dish TV has forex debt of about US$135 mn of which

about 55-60% is hedged.

Zee Entertainment Enterprises

Z IN Equity

(1) Preference capital to be classified as financial liability and (2) investments would be marked to market on a quarterly basis

and routed through the P&L.

COAL IN Equity

Income statement: Increase in EBITDA as accounting for overburden provision will be discontinued (Rs28 bn in FY2016) and

accounting for actuarial changes for employee-related expenses will be adjusted through other comprehensive income.

However, DD&A will increase due to amortization of stripping activity assets under units of production method. Also, OCF may

decline as company will have to pay tax on higher reported incomelower overburden will not be offset by higher DD&A.

Under earlier accounting, company got a tax break on overburden provision.

Metals & Mining

Coal India

Balance sheet: Write-back of past overburden provision (Rs470 bn up to March 2016) that will likely be routed through the

other comprehensive income will increase the net worth. Cash balances may reduce owing to a potential tax outgo on writeback of past overburden removal.

Hindalco Industries

HNDL IN Equity

Income statement: (1) EBITDA may increase due to (a) inclusion of 'take-or-pay' contracts, (b) discounting of long-term

provisions to the present value, (c) part of the production stripping cost being recognized as asset from open cast mining

operations etc., (2) depreciation charge may increase due to revaluation of assets, 'take-or-pay' contracts, and (3) interest

expense may increase due to 'take-or-pay' contracts. Also, FX fluctuation on loans for capital assets will be recognized in

income statement rather being capitalized, which may increase earnings volatility.

Balance sheet: (1) Net worth may change due to revaluation of PPE, recognition of investments at fair value, (2) borrowings can

change due to (a) inclusion of 'take-or-pay' contracts in debt, (b) recognition of various bill factoring with bank as debt, (3)

fixed assets may increase due to fair value exercise, 'take-or-pay' contract inclusion in the balance sheet and classification of

capital advances as C-WIP rather than loans and advances, (4) current assets will change due to increase in debtors (of those

discounted from banks), possibly lower inventories (elimination of interest on deferred settlement terms), and (5) current

liabilities will change due to lower long-term provisions (present value impact).

Hindustan Zinc

HZ IN Equity

Income statement: (1) EBITDA may change (a) as part of the production stripping cost is recognized as asset from open cast

mining operations and (b) from inclusion of 'take-or-pay' contracts, (2) depreciation may increase if assets are revalued, and

(3) company may start reporting certain interest costs after accounting for long-term provision in present value terms.

Balance sheet: (1) Net worth may increase due to revaluation of PPE, (2) fixed assets may increase due to fair value exercise,

'take-or-pay' contract inclusion in balance sheet and classification of capital advances as C-WIP rather than loans and

advances, (3) current assets will change due to increase in debtors (of those discounted from banks), possibly lower

inventories (elimination of interest on deferred settlement terms), and (4) current liabilities will change due to lower long-term

provisions (present value impact).

JSW Steel

JSTL IN Equity

Income statement: (1) EBITDA may increase due to (a) inclusion of 'take-or-pay' contracts, (b) de-recognition of interest

expense from cost of RM purchases and inventories based on difference in deferred settlement terms and normal credit period,

(c) discounting of long-term provisions to the present value, etc., (2) depreciation charge may increase due to revaluation of

assets, 'take-or-pay' contracts and (3) interest expense may increase to account for interest on RM purchases on deferred credit

terms, 'take-or-pay' contracts, re-classification of redeemable preference shares as debt. Also, FX fluctuation on loans for

capital assets will be recognized in income statement rather being capitalized, which may increase earnings volatility.

Balance sheet: (1) Net worth may increase due to revaluation of PPE, recognition of investments at fair value, (2) borrowings

can increase due to (a) re-classification of redeemable preference shares as debt, (b) inclusion of debt for 'take-or-pay'

contracts, (c) recognition of debtors discounted (bill factoring) as debt, (3) fixed assets may increase due to fair value exercise,

'take-or-pay' contract balance-sheet inclusion and classification of capital advances as C-WIP rather than loans and advances,

(4) current assets will change due to increase in debtors (of those discounted from banks), possibly lower inventories

(elimination of interest on deferred settlement terms), and (5) current liabilities will change due to lower long-term provisions

(present value impact).

Source: Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH

Strategy

India

1QFY17 results may see some positive and negative surprises on reported numbers (cont.)

Impact of Ind-AS on top companies in our universe

Company

National Aluminium Co.

Ticker

NACL IN Equity

Implications

Income statement: (1) EBITDA may increase as (a) part of the production stripping cost is recognized as asset from open cast

mining operations and (b) inclusion of 'take-or-pay' contracts, (2) depreciation may increase if assets are revalued, and (3)

company may start reporting certain interest costs after accounting for long-term provision in present value terms.

Balance sheet: (1) Net worth may increase due to revaluation of PPE, (2) fixed assets may increase due to fair value exercise,

'take-or-pay' contract balance-sheet inclusion and classification of capital advances as C-WIP rather than loans and advances,

and (3) current liabilities will change due to lower long-term provisions (present value impact).

NMDC

NMDC IN Equity

Income statement: (1) EBITDA may increase (a) as part of the production stripping cost is recognized as asset from open cast

mining operations and (b) from inclusion of 'take-or-pay' contracts, (2) depreciation may increase if assets are revalued, and (3)

company may start reporting certain interest costs after accounting for long-term provision in present value terms.

Balance sheet: (1) Net worth may increase due to revaluation of PPE, and (2) fixed assets may increase due to fair value

exercise, 'take-or-pay' contract inclusion in balance sheet and classification of capital advances as C-WIP rather than loans and

advances.

Tata Steel

TATA IN Equity

Income statement: (1) EBITDA may increase due to (a) inclusion of 'take-or-pay' contracts, (b ) discounting of long-term

provisions to the present value, etc., (2) depreciation charge may increase due to revaluation of assets, 'take-or-pay' contracts,

and (3) interest expense may increase due to 'take-or-pay' contracts. Also, FX fluctuation on loans for capital assets will be

recognized in income statement rather being capitalized, which may increase earnings volatility.

Balance sheet: (1) Net worth may change due to revaluation of PPE, recognition of investments at fair value, (2) borrowings can

change due to (a) inclusion 'take-or-pay' contracts in debt, (b) recognition of various bill factoring with bank as debt, (3) fixed

assets may increase due to fair value exercise, 'take-or-pay' contract balance-sheet inclusion and classification of capital

advances as C-WIP rather than loans and advances, (4) current assets will change due to increase in debtors (of those

discounted from banks), possibly lower inventories (elimination of interest on deferred settlement terms), and (5) current

liabilities will change due to lower long-term provisions (present value impact).

Consolidation and JVs: The investment in JVs will be recognized at full value of assets, liabilities and share of income rather

than proportionate consolidation (per earlier practice) for those JVs where company has effective control. Also, consolidation

will be based on effective control over entities and this may lead to consolidation of some entities in which Tata Steel does not

have more than 50% ownership. In case of other JVs, equity method will be used, which will reduce the asset, liabilities given

proportional consolidation earlier.

Vedanta

VEDL IN Equity

Income statement: (1) Amortization of goodwill will be nil as it will now be tested for impairment rather than being amortized,

(2) other income may increase sharply. This is due to MTM accounting (fair value) of FMPs in subsidiaries including HZ. We

note that Vedanta was accounting for these FMP's on maturity basis while HZ accounted on MTM basis. The backlog (being

lower amount accounted by Vedanta) was Rs44 bn as of March 2016. Also, FX fluctuation on loans for capital assets will be

recognized in income statement rather being capitalized, which may increase earnings volatility.

Balance sheet: (1) Net worth may increase due to revaluation of PPE, recognition of investments at fair value, (2) borrowings

can change due to recognition of various bill factoring done with bank as debt, (3) fixed assets may increase due to fair value

exercise, 'take-or-pay' contract inclusion in balance sheet and classification of capital advances as C-WIP rather than loans and

advances, (4) current assets will change due to increase in debtors (of those discounted from banks), possibly lower

inventories (elimination of interest on deferred settlement terms), and (5) current liabilities will change due to lower long-term

provisions (present value impact).

Others

InterGlobe Aviation

INDIGO IN Equity

(1) Revenues to be reported net of commission paid to dealers/aggregators. Net impact: lower revenues, same EBITDA, higher

EBITDA margin.

(2) Impact of forex fluctuation on book value of aircraft financed through borrowings in foreign currency will be routed through

P&L. Impact: increased volatility in the reported income.

(3) Other income from investments in long-term debt instruments (significant in case of IndiGo) to be booked on proportionate

basis. Impact: reduced volatility in other income.

PI Industries

PI IN Equity

(1) Revenues to be reported gross of excise duty; PI already reports revenues net of discounts. Net impact: higher revenues,

same EBITDA, lower EBITDA margin.

(2) Finance income component of revenues generated through sale on credit (significant in case of domestic ag-chem business)

to be separately booked in other income. Impact: lower revenues, EBITDA and margins, higher other income, unchanged PAT.

(3) Impact of forex fluctuation on carrying value of assets financed through borrowings in foreign currency will be routed

through P&L. Impact: increased volatility in the reported income.

Tata Chemicals

TTCH IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Impact of forex fluctuation on carrying value of assets financed through borrowings in foreign currency will be routed

through P&L. Impact: increased volatility in the reported income.

UPL

UPLL IN Equity

(1) Revenues to be reported gross of excise duty and net of discounts/incentives. Net impact: higher revenues, same EBITDA,

lower EBITDA margin.

(2) Finance income component of revenues generated through sale on credit (significant in case of UPL) to be separately

booked in other income. Impact: lower revenues, EBITDA and margins, higher other income, unchanged PAT.

(3) One-time adjustment of impairment of intangible assets through reserves is allowed. UPL carries significant amount of

goodwill on its books (Rs14.6 bn), which may see a significant write down, thus improving return ratios of the firm.

(4) UPL will need to consolidate accounts of Advanta, despite it being an associate company at present, on account of its

significant control over company's operations.

Whirlpool

WHIRL IN Equity

(1) Revenues to be reported gross of excise duty. The company already reports revenues net of discounts/incentives. Net

impact: higher revenues, same EBITDA and lower EBITDA margin.

Source: Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH

India

Strategy

1QFY17 results may see some positive and negative surprises on reported numbers (cont.)

Impact of Ind-AS on top companies in our universe

Company

Ticker

Implications

Pharmaceuticals

Biocon

BIOS IN Equity

Impact of ESOP accounting change to fair value method (Rs50 mn) and recognition to foreign currency movement on long-term

monetary assets in the P&L (Rs39 mn) is marginal.

Cipla

CIPLA IN Equity

Impact of ESOP accounting change to fair value method is marginal (Rs40 mn). ~80 bps impact on EBITDA margins due to

change in excise recognition in COGS as opposed to net revenues, though no impact on absolute EBITDA. All investments to

now be recognized at fair value, with MTM gains recognized in P&L. Bulk of Invagen acquisition value likely to be recognized in

goodwill, and hence, impact on account of intangibles recognition likely to be limited.

Dr Lal Pathlabs

DLPL IN Equity

Net worth is less than Rs5 bn, so no immediate impact.

Dr Reddy's Laboratories

DRRD IN Equity

DRRD uses IFRS, so, we do not expect any material change to numbers.

Lupin

LPC IN Equity

Impact of ESOP accounting change to fair value method is marginal (~Rs500 mn). ~67 bps impact on EBITDA margins due to

change in excise recognition in COGS as opposed to net revenues, though no impact on absolute EBITDA. All investments to

now be recognized at fair value, with MTM gains recognized in P&L, which will help smoothen earnings. A significant portion

of Gavis fair value has been allocated to intangibles, which will result in annual amortization charge increasing by Rs4.5-5.0 bn.

Sun Pharmaceuticals

SUNP IN Equity

~90 bps impact on EBITDA margin due to change in excise recognition in COGS as opposed to net revenues, though no impact

on absolute EBITDA. All investments to now be recognized at fair value, with MTM gains recognized in P&L.

Torrent Pharmaceuticals

TRP IN Equity

Torrent can potentially recognize Elder intangibles as having indefinite useful life, which can have ~10% EPS impact with Rs970

mn amortized currently.

DLF

DLFU IN Equity

Major changes in subsidiary, JV and JDA accounting - largely reflect in changes in display of income statement.

Oberoi Realty

OBER IN Equity

Major changes in subsidiary, JV and JDA accounting - largely reflect in changes in display of income statement.

Infosys

INFO IN Equity

Infosys reports as per IFRS. There will be no meaningful impact on move to Ind-AS.

Mindtree

MTCL IN Equity

Mindtree reports as per Indian GAAP as well as IFRS. Ind-AS reporting will not be meaningfully different from IFRS. Key changes

under Ind-AS (versus Indian GAAP) would be (1) increase in amortization on intangibles, which will impact EBIT margin by 100

bps, and (2) mark to market of investments on quarterly basis will impact other income.

Mphasis

MPHL IN Equity

TCS

TCS IN Equity

Tech Mahindra

(1) ESOP accounting will be based on fair value versus intrinsic value earlier. It will result in increase in ESOP costs by US$8 mn

in FY2017, (2) treasury shares will not show up on P&L and BS. Shares count (excl. treasury shares) would be used for EPS

calculation (investors have always valued the stock on EPS ex-treasury shares). Investment in treasury shares will be adjusted

TECHM IN Equity against reserves on BS, (3) no meaningful forex impact as Tech M has adopted hedge accounting as per AS 32, (4) M&A

accounting will be as per purchase method. It will result in significant impairment of goodwill for acquisitions done in FY2016

and later (Pininfarina and Target group), and (5) Tech M has limited investments in FMP; shift to Ind-AS will not impact other

income meaningfully.

Wipro

WPRO IN Equity

Wipro reports as per IFRS. There will be no meaningful impact on move to Ind-AS.

BHARTI IN Equity

(1) Activation fee/installation charges or similar nature of other charges is recognized over the expected life of the customer

and is not permitted to be recognized upfront; adoption of Ind-AS will affect (reduce) the revenue recognition of the relevant

year in which the mobile connection is given due to its spread over the expected life of the customer. This will be a case of

deferment of revenue.

Real estate

Technology

TCS reports as per IFRS. There will be no meaningful impact on move to Ind-AS.

Telecom

Bharti Airtel

(2) Assets retirement obligations (ARO) are measured at present value of the expected cost to settle the obligation; ARO

liability is discounted and measured at amortized cost with subsequent charging of the amortization amount as finance cost.

This will have impact on the profit for the year.

Bharti Infratel

BHIN IN Equity

(1) Revenue and rent equalization reporting will cease and the company will start booking revenue/rent on cash basis; this

would result in a one-time charge on equity (in FY2017) in order to reverse the impact of revenue/rent equalization recognized

from FY2008 onwards. We believe that the one-time impact would be close to Rs14 bn.

(2) Equity method would be used to account for the consolidation of Indus' operations as opposed to proportionate

consolidation currently; this would impact all line items except net profit.

(3) Fair valuation of marketable investments: BHIN invests a good portion (87% at end-FY2015) of its cash in mutual funds.

With fair value (as opposed to the current 'book gain/loss on maturity') accounting, volatility in earnings will come down.

IDEA

Reliance Communications

IDEA IN Equity

(1) Activation fee/installation charges or similar nature of other charges is recognized over the expected life of the customer

and is not permitted to be recognized upfront; adoption of Ind-AS will affect (reduce) the revenue recognition of the relevant

year in which the mobile connection is given due to its spread over the expected life of the customer. This will be a case of

deferment of revenue.

RCOM IN Equity

(1) As per Ind-AS, the amount of foreign exchange difference arising on the liabilities for acquisition of fixed assets would have

to be charged to P&L account. If a company has opted to capitalize the exchange differences as per existing accounting

standard, adoption of Ind-AS will affect the amount of fixed assets as well as depreciation charged for the year and also for the

subsequent years because of non capitalization of exchange differences. RCOM added Rs 6.55 bn of exchange differences on

long-term borrowing relating to acquisition of depreciable capital assets to the cost of capitalized assets in FY2015.

(2) Activation fee/installation charges or similar nature of other charges is recognized over the expected life of the customer

and is not permitted to be recognized upfront; adoption of Ind-AS will affect (reduce) the revenue recognition of the relevant

year in which the mobile connection is given due to its spread over the expected life of the customer. This will be a case of

deferment of revenue.

(3) In case of composite assets (like BTS), all items of fixed assets are to be broken to significant parts for component-wise

accounting; if the rate of depreciation(which based on the useful life) of various components of fixed asset is different from

those used for the whole asset at present, there will be a change in amount of depreciation charged and consequently the

written down value of the components of fixed asset and profit for the year.

Source: Kotak Institutional Equities estimates

10

KOTAK INSTITUTIONAL EQUITIES RESEARCH

Strategy

India

1QFY17 results may see some positive and negative surprises on reported numbers (cont.)

Impact of Ind-AS on top companies in our universe

Company

Ticker

Implications

Utilities

Adani Power

ADANI IN Equity

Adani Power may have to discontinue accruing revenues on under-recovery of fuel cost, though that will depend on the timeline

by which adoption of Ind-AS for revenue recognition becomes effective. Foreign exchange-related losses on debt will have to

be routed through the income statement, instead of being capitalized.

JSW Energy

JSW IN Equity

Power companies will not be able to recognize under-recovery of tariffs that leads to creation of regulated assets as was the

practice under Indian GAAP, though the impact of the same will depend on the timeline by which adoption of Ind-AS for

revenue recognition becomes effective.

NHPC

NHPC IN Equity

Power companies will not be able to recognize under-recovery of tariffs that leads to creation of regulated assets as was the

practice under Indian GAAP, though the impact of the same will depend on the timeline by which adoption of Ind-AS for

revenue recognition becomes effective. Foreign exchange-related losses on debt will have to be routed through the income

statement, instead of being capitalized.

NTPC

NTPC IN Equity

Power companies will not be able to recognize under-recovery of tariffs that leads to creation of regulated assets as was the

practice under Indian GAAP, though the impact of the same will depend on the timeline by which adoption of Ind-AS for

revenue recognition becomes effective. Foreign exchange-related losses on debt will have to be routed through the income

statement, instead of being capitalized.

Power Grid

PWGR IN Equity

Power companies will not be able to recognize under-recovery of tariffs that leads to creation of regulated assets as was the

practice under Indian GAAP, though the impact of the same will depend on the timeline by which adoption of Ind-AS for

revenue recognition becomes effective. Foreign exchange-related losses on debt will have to be routed through the income

statement, instead of being capitalized.

Reliance Power

RPWR IN Equity

Power companies will not be able to recognize under-recovery of tariffs that leads to creation of regulated assets as was the

practice under Indian GAAP, though the impact of the same will depend on the timeline by which adoption of Ind-AS for

revenue recognition becomes effective. Foreign exchange-related losses on debt will have to be routed through the income

statement, instead of being capitalized.

TPWR IN Equity

Tata Power will have to discontinue proportionate consolidation of earnings from the coal business (revenues of Rs81 bn and

EBITDA of Rs13.6 bn in FY2015), leading to lower revenues and EBITDA, though impact would be neutral at the net income

level. Power companies will not be able to recognize under-recovery of tariffs that leads to creation of regulated assets (Rs17

bn in Mumbai and Rs47 bn in Delhi as of March 2016) as was the practice under Indian GAAP, though the impact of the same

will depend on the timeline by which adoption of Ind-AS for revenue recognition becomes effective. Foreign exchange-related

losses on debt will have to be routed through the income statement, instead of being capitalized. Investments in telecom

subsidiaries of the group will have to be reported on fair value leading to increase in net worth as well.

Tata Power

Banking companies

Applicable for scheduled commercial banks and insurance companies from April 1, 2018.

Source: Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH

11

Disclosures

"I, Sanjeev Prasad, hereby certify that all of the views expressed in this report accurately reflect my personal views about the

subject company or companies and its or their securities. I also certify that no part of my compensation was, is or will be,

directly or indirectly, related to the specific recommendations or views expressed in this report."

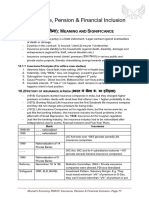

Kotak Institutional Equities Research coverage universe

Distribution of ratings/investment banking relationships

Percentage of companies covered by Kotak Institutional

Equities, within the specified category.

70%

60%

50%

40%

34.4%

30.6%

30%

19.4%

20%

10%

15.6%

3.3%

5.0%

1.1%

0.6%

REDUCE

SELL

0%

BUY

ADD

Percentage of companies within each category for

which Kotak Institutional Equities and or its affiliates has

provided investment banking services within the

previous 12 months.

* The above categories are defined as follows: Buy = We

expect this stock to deliver more than 15% returns over

the next 12 months; Add = We expect this stock to

deliver 5-15% returns over the next 12 months; Reduce

= We expect this stock to deliver -5-+5% returns over

the next 12 months; Sell = We expect this stock to deliver

less than -5% returns over the next 12 months. O ur

target prices are also on a 12-month horizon basis.

These ratings are used illustratively to comply with

applicable regulations. As of 31/03/2016 Kotak

Institutional Equities Investment Research had

investment ratings on 180 equity securities.

Source: Kotak Institutional Equities

As of March 31, 2016

Ratings and other definitions/identifiers

Definitions of rating

BUY. We expect this stock to deliver more than 15% returns over the next 12 months.

ADD. We expect this stock to deliver 5-15% returns over the next 12 months.

REDUCE. We expect this stock to deliver -5-+5% returns over the next 12 months.

SELL. We expect this stock to deliver <-5% returns over the next 12 months.

Our target prices are also on a 12-month horizon basis.

Other definitions

Coverage view. The coverage view represents each analysts overall fundamental outlook on the Sector. The coverage view will consist of one of the following

designations: Attractive, Neutral, Cautious.

Other ratings/identifiers

NR = Not Rated. The investment rating and target price, if any, have been suspended temporarily. Such suspension is in compliance with applicable regulation(s)

and/or Kotak Securities policies in circumstances when Kotak Securities or its affiliates is acting in an advisory capacity in a merger or strategic transaction

involving this company and in certain other circumstances.

CS = Coverage Suspended. Kotak Securities has suspended coverage of this company.

NC = Not Covered. Kotak Securities does not cover this company.

RS = Rating Suspended. Kotak Securities Research has suspended the investment rating and price target, if any, for this stock, because there is not a sufficient

fundamental basis for determining an investment rating or target. The previous investment rating and price target, if any, are no longer in effect for this stock

and should not be relied upon.

NA = Not Available or Not Applicable. The information is not available for display or is not applicable.

NM = Not Meaningful. The information is not meaningful and is therefore excluded.

12

KOTAK INSTITUTIONAL EQUITIES RESEARCH

Corporate Office

Overseas Affiliates

Kotak Securities Ltd.

Kotak Mahindra (UK) Ltd

Kotak Mahindra Inc

27 BKC, Plot No. C-27, G Block

8th Floor, Portsoken House

369 Lexington Avenue

Bandra Kurla Complex, Bandra (E)

155-157 Minories

28th Floor, New York

Mumbai 400 051, India

London EC3N 1LS

NY 10017, USA

Tel: +91-22-43360000

Tel: +44-20-7977-6900

Tel:+1 212 600 8856

Copyright 2016 Kotak Institutional Equities (Kotak Securities Limited). All rights reserved.

1. Note that the research analysts contributing to this report may not be registered/qualified as research analysts with FINRA; and

2. Such research analysts may not be associated persons of Kotak Mahindra Inc and therefore, may not be subject to NASD Rule 2711 restrictions on

communications with a subject company, public appearances and trading securities held by a research analyst account.

3. Any U.S. recipients of the research who wish to effect transactions in any security covered by the report should do so with or through Kotak

Mahindra Inc and (ii) any transactions in the securities covered by the research by U.S. recipients must be effected only through Kotak Mahindra Inc

at nilesh.jain@kotak.com.

This report is distributed in Singapore by Kotak Mahindra (UK) Limited (Singapore Branch) to institutional investors, accredited investors or expert investors only as

defined under the Securities and Futures Act. Recipients of this analysis / report are to contact Kotak Mahindra (UK) Limited (Singapore Branch) (16 Raffles Quay,

#35-02/03, Hong Leong Building, Singapore 048581) in respect of any matters arising from, or in connection with, this analysis / report. Kotak Mahindra (UK)

Limited (Singapore Branch) is regulated by the Monetary Authority of Singapore.

Kotak Securities Limited and its affiliates are a full-service, integrated investment banking, investment management, brokerage and financing group. We along with

our affiliates are leading underwriter of securities and participants in virtually all securities trading markets in India. We and our affiliates have investment banking

and other business relationships with a significant percentage of the companies covered by our Investment Research Department. Our research professionals

provide important input into our investment banking and other business selection processes. Investors should assume that Kotak Securities Limited and/or its

affiliates are seeking or will seek investment banking or other business from the company or companies that are the subject of this material and that the research

professionals who were involved in preparing this material may participate in the solicitation of such business. Our research professionals are paid in part based on

the profitability of Kotak Securities Limited, which include earnings from investment banking and other business. Kotak Securities Limited generally prohibits its

analysts, persons reporting to analysts, and members of their households from maintaining a financial interest in the securities or derivatives of any companies that

the analysts cover. Additionally, Kotak Securities Limited generally prohibits its analysts and persons reporting to analysts from serving as an officer, director, or

advisory board member of any companies that the analysts cover. Our salespeople, traders, and other professionals may provide oral or written market

commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein, and our proprietary trading and investing

businesses may make investment decisions that are inconsistent with the recommendations expressed herein. In reviewing these materials, you should be aware

that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest. Additionally, other important information regarding our

relationships with the company or companies that are the subject of this material is provided herein.

This material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation

would be illegal. We are not soliciting any action based on this material. It is for the general information of clients of Kotak Securities Limited. It does not constitute

a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any advice

or recommendation in this material, clients should consider whether it is suitable for their particular circumstances and, if necessary, seek professional advice. The

price and value of the investments referred to in this material and the income from them may go down as well as up, and investors may realize losses on any

investments. Past performance is not a guide for future performance, future returns are not guaranteed and a loss of original capital may occur. Kotak Securities

Limited does not provide tax advise to its clients, and all investors are strongly advised to consult with their tax advisers regarding any potential investment.

Certain transactions -including those involving futures, options, and other derivatives as well as non-investment-grade securities - give rise to substantial risk and

are not suitable for all investors. The material is based on information that we consider reliable, but we do not represent that it is accurate or complete, and it

should not be relied on as such. Opinions expressed are our current opinions as of the date appearing on this material only. We endeavor to update on a

reasonable basis the information discussed in this material, but regulatory, compliance, or other reasons may prevent us from doing so. We and our affiliates,

officers, directors, and employees, including persons involved in the preparation or issuance of this material, may from time to time have long or short

positions in, act as principal in, and buy or sell the securities or derivatives thereof of companies mentioned herein. Kotak Securities Limited and its non US affiliates

may, to the extent permissible under applicable laws, have acted on or used this research to the extent that it relates to non US issuers, prior to or immediately

following its publication. Foreign currency denominated securities are subject to fluctuations in exchange rates that could have an adverse effect on the value or

price of or income derived from the investment. In addition, investors in securities such as ADRs, the value of which are influenced by foreign currencies affectively

assume currency risk. In addition options involve risks and are not suitable for all investors. Please ensure that you have read and understood the current derivatives

risk disclosure document before entering into any derivative transactions.

Kotak Securities Limited established in 1994, is a subsidiary of Kotak Mahindra Bank Limited. Kotak Securities is one of Indias largest brokerage and distribution

house.

Kotak Securities Limited is a corporate trading and clearing member of BSE Limited (BSE), National Stock Exchange of India Limited (NSE), MSEI and United Stock

Exchange of India Limited (USEIL). Our businesses include stock broking, services rendered in connection with distribution of primary market issues and financial

products like mutual funds and fixed deposits, depository services and Portfolio Management.

Kotak Securities Limited is also a depository participant with National Securities Depository Limited (NSDL) and Central Depository Services (India) Limited (CDSL).

Kotak Securities Limited is also registered with Insurance Regulatory and Development Authority as Corporate Agent for Kotak Mahindra Old Mutual Life Insurance

Limited and is also a Mutual Fund Advisor registered with Association of Mutual Funds in India (AMFI). Kotak Securities Limited is registered as a Research Analyst

under SEBI (Research Analyst) Regulations, 2014.

We hereby declare that our activities were neither suspended nor we have defaulted with any stock exchange authority with whom we are registered in last five

years. However SEBI, Exchanges and Depositories have conducted the routine inspection and based on their observations have issued advise letters or levied minor

penalty on KSL for certain operational deviations. We have not been debarred from doing business by any Stock Exchange / SEBI or any other authorities; nor has

our certificate of registration been cancelled by SEBI at any point of time.

We offer our research services to primarily institutional investors and their employees, directors, fund managers, advisors who are registered with us

Details of Associates are available on our website i.e. www.kotak.com

Research Analyst has not served as an officer, director or employee of Subject Company. We or our associates have received compensation from the subject

company in the past 12 months. We or our associates have managed or co-managed public offering of securities for the subject company in the past 12 months.

We or our associates have received compensation for investment banking or merchant banking or brokerage services from the subject company in the past 12