You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- English For Financial Literacy Volume 1Document313 pagesEnglish For Financial Literacy Volume 1Azure Pear HaNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Principles of Islamic JurisprudenceDocument338 pagesPrinciples of Islamic JurisprudenceWanie_Ckieyn__1255100% (9)

- Brokers Accreditation AgreementDocument7 pagesBrokers Accreditation AgreementCharmaine CuynoNo ratings yet

- 200 SAP SD Interview Questions and AnswersDocument16 pages200 SAP SD Interview Questions and Answersestivali10No ratings yet

- Business Blue PrintDocument65 pagesBusiness Blue PrintImtiaz KhanNo ratings yet

- BBA.5 (Unit.1 Introduction To Direct Tax, Residential Status and Income Under The Head of SalariesDocument66 pagesBBA.5 (Unit.1 Introduction To Direct Tax, Residential Status and Income Under The Head of SalariesMihir AsnaniNo ratings yet

- Senarai Syarikat Yang Mendaftar Semula 1 PDFDocument3,140 pagesSenarai Syarikat Yang Mendaftar Semula 1 PDFfura5salNo ratings yet

- Practical Accounting 1-MockboardzDocument9 pagesPractical Accounting 1-MockboardzMoira C. Vilog100% (1)

- Usm Alumni Association Membership Form: Personal DetailsDocument1 pageUsm Alumni Association Membership Form: Personal DetailsShahrir RayNo ratings yet

- SK Seri Tasik, Bandar Sri Permaisuri, Kuala Lumpur Organisasi Kokurikulum 2018Document1 pageSK Seri Tasik, Bandar Sri Permaisuri, Kuala Lumpur Organisasi Kokurikulum 2018Shahrir RayNo ratings yet

- Project 100Document2 pagesProject 100Shahrir RayNo ratings yet

- SK Seri Tasik, Bandar Sri Permaisuri, Kuala Lumpur Organisasi Kokurikulum 2018Document1 pageSK Seri Tasik, Bandar Sri Permaisuri, Kuala Lumpur Organisasi Kokurikulum 2018Shahrir RayNo ratings yet

- Takaful SureCover - ZT0033.1.P.L.B.M (Final)Document14 pagesTakaful SureCover - ZT0033.1.P.L.B.M (Final)Shahrir RayNo ratings yet

- Nota Takafulink New Plan (Nota) SoftDocument7 pagesNota Takafulink New Plan (Nota) SoftShahrir RayNo ratings yet

- Nota Takafulink New Plan (Nota) SoftDocument7 pagesNota Takafulink New Plan (Nota) SoftShahrir RayNo ratings yet

- Skema Jawapan PJK t4Document1 pageSkema Jawapan PJK t4sklupakNo ratings yet

- Nota Takafulink New Plan (Nota) SoftDocument7 pagesNota Takafulink New Plan (Nota) SoftShahrir RayNo ratings yet

- Nota Takafulink New Plan (Nota) SoftDocument7 pagesNota Takafulink New Plan (Nota) SoftShahrir RayNo ratings yet

- Crisis in The Muslim Mind-AbuSulaymanDocument82 pagesCrisis in The Muslim Mind-AbuSulaymanTowardsLightNo ratings yet

- Withholding Tax Payables OptionsDocument7 pagesWithholding Tax Payables OptionsVijay Kumar TNo ratings yet

- TaxSavings For Salaried EmployeesDocument18 pagesTaxSavings For Salaried Employeesravi100% (1)

- College Hostel Mess Fees - Clarification Regarding Taxability and Rate of GSTDocument6 pagesCollege Hostel Mess Fees - Clarification Regarding Taxability and Rate of GSTRohan KulkarniNo ratings yet

- LilliputDocument17 pagesLilliputSharn GillNo ratings yet

- Tds GuidelineDocument23 pagesTds GuidelineYash BhayaniNo ratings yet

- Management Information 3 (ICAI)Document88 pagesManagement Information 3 (ICAI)Rajib HossainNo ratings yet

- Ingram Micro Malaysia SDN BHD (175932-M)Document10 pagesIngram Micro Malaysia SDN BHD (175932-M)akoolaNo ratings yet

- Nomura Coke BottlingDocument32 pagesNomura Coke BottlingSXC948No ratings yet

- Government Intervention - Taxes and SubsidiesDocument10 pagesGovernment Intervention - Taxes and SubsidiesfantasybookwyrmNo ratings yet

- G.R. No. 96016 October 17, 1991 Commissioner of Internal Revenue, Petitioner, vs. The Court of Appeals and Efren P. Castaneda, RespondentsDocument1 pageG.R. No. 96016 October 17, 1991 Commissioner of Internal Revenue, Petitioner, vs. The Court of Appeals and Efren P. Castaneda, RespondentsCristy Yaun-CabagnotNo ratings yet

- Me Important Question1,2,3,4,5Document58 pagesMe Important Question1,2,3,4,5Asis MahalikNo ratings yet

- Application For Registration As A Vendor: Next PageDocument4 pagesApplication For Registration As A Vendor: Next PageMark KNo ratings yet

- Invoice M112308296312009275Document1 pageInvoice M112308296312009275Bruh YooinkNo ratings yet

- The Maharashtra Stamp (Determination of True Market Value of Property) Rules, 1995 - Maharashtra Housing and Building LawsDocument20 pagesThe Maharashtra Stamp (Determination of True Market Value of Property) Rules, 1995 - Maharashtra Housing and Building LawsSudarshan GadalkarNo ratings yet

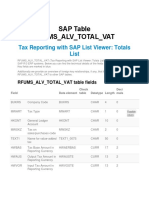

- RFUMSDocument2 pagesRFUMSSivakumar ThangarajanNo ratings yet

- Introduction To Consumption Taxes: Prepared By: Mrs. Nelia I. Tomas, CPA, LPTDocument56 pagesIntroduction To Consumption Taxes: Prepared By: Mrs. Nelia I. Tomas, CPA, LPTTokis SabaNo ratings yet

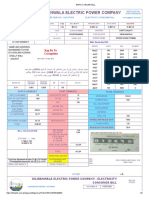

- Bill Gepco ForDocument2 pagesBill Gepco ForMohsan AliNo ratings yet

- This Paper Is Not To Be Removed From The Examination HallDocument4 pagesThis Paper Is Not To Be Removed From The Examination HallTaslimaNo ratings yet

- Request For Proposals: 2017 Lodging Tax FundDocument16 pagesRequest For Proposals: 2017 Lodging Tax FundPratitiNo ratings yet

- Circular No. 17 of 2020 (F. No.370133 - 22 - 2020-Tpl) Guidelines Under Section 194-O (4) and Section 206c (1h) of The Income-Tax Act, 1961Document3 pagesCircular No. 17 of 2020 (F. No.370133 - 22 - 2020-Tpl) Guidelines Under Section 194-O (4) and Section 206c (1h) of The Income-Tax Act, 1961Vivek AgarwalNo ratings yet

- Branch Teller: Use SCR 008765 Deposit Fee Collection State Bank CollectDocument1 pageBranch Teller: Use SCR 008765 Deposit Fee Collection State Bank CollectNishchay Kumar RaiNo ratings yet

- Applied Direct TaxationDocument548 pagesApplied Direct TaxationVarun SinghNo ratings yet

- State of Hawaii Basic Business Application: Form Bb-1 (Rev. 2022)Document6 pagesState of Hawaii Basic Business Application: Form Bb-1 (Rev. 2022)Tham DangNo ratings yet

- Nepal Budget Highlights - 79-80 - APM & AssociatesDocument89 pagesNepal Budget Highlights - 79-80 - APM & Associatesaasthapoddar155No ratings yet