You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Mod 1 - Framework For Analysis & ValuationDocument33 pagesMod 1 - Framework For Analysis & ValuationbobdoleNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Financial Analysis Cheat Sheet: by ViaDocument2 pagesFinancial Analysis Cheat Sheet: by Viaheehan6No ratings yet

- Chapter 3 An Introduction To Consolidated Financial Statements - STDDocument54 pagesChapter 3 An Introduction To Consolidated Financial Statements - STDdhfbbbbbbbbbbbbbbbbbh100% (1)

- Resume Book: Columbia Healthcare and Pharmaceutical Management ProgramDocument44 pagesResume Book: Columbia Healthcare and Pharmaceutical Management ProgramJohn Mathias100% (2)

- Allapacan Company Bought 20Document18 pagesAllapacan Company Bought 20Carl Yry BitzNo ratings yet

- Milk Powder ProductionDocument28 pagesMilk Powder Productionabel_kayel100% (2)

- 72 Inventory Management and Financial PeDocument22 pages72 Inventory Management and Financial PeKiersteen AnasNo ratings yet

- Original PDF Financial Statement Analysis and Security Valuation 5th Edition PDFDocument41 pagesOriginal PDF Financial Statement Analysis and Security Valuation 5th Edition PDFgordon.hatley642100% (31)

- Accounting Statements and Cash FlowDocument33 pagesAccounting Statements and Cash Flowfathir alhakimNo ratings yet

- 10 Things You Must Do Before Buying An IPO, But Nobody Tells You About ThemDocument11 pages10 Things You Must Do Before Buying An IPO, But Nobody Tells You About ThemRanjit SahooNo ratings yet

- Associate Bearings Company LimitedDocument18 pagesAssociate Bearings Company LimitedKnt Nallasamy GounderNo ratings yet

- Audit of CFS Mind MapDocument1 pageAudit of CFS Mind Mapgovarthan1976No ratings yet

- Test Bank For Fundamentals of Financial Management 11th Edition Eugene F Brigham DR Joel F HoustonDocument38 pagesTest Bank For Fundamentals of Financial Management 11th Edition Eugene F Brigham DR Joel F HoustonThomas Peterson100% (14)

- Sustainability 13 01933 v2Document15 pagesSustainability 13 01933 v2ronNo ratings yet

- GL HOTELS LIMITED ("GL Hotels"/ "Target Company")Document1 pageGL HOTELS LIMITED ("GL Hotels"/ "Target Company")vridhiNo ratings yet

- Wag Kang Aayaw Co's cash and cash equivalents balanceDocument1 pageWag Kang Aayaw Co's cash and cash equivalents balanceMark Domingo MendozaNo ratings yet

- Option PricingDocument30 pagesOption Pricingkfir goldburdNo ratings yet

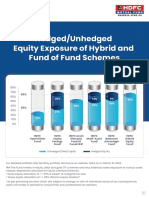

- Leaflet - Hedged and Unhedged Exposure of Hybrid FundsDocument2 pagesLeaflet - Hedged and Unhedged Exposure of Hybrid FundsDeepakNo ratings yet

- Edison RevengeDocument51 pagesEdison RevengeescanquemaNo ratings yet

- Market Index: Dow Jones - 100 Year HistoryDocument31 pagesMarket Index: Dow Jones - 100 Year Historyyoni hathahanNo ratings yet

- Far - First Preboard QuestionnaireDocument14 pagesFar - First Preboard QuestionnairewithyouidkNo ratings yet

- List of Stock Exchanges in The World PDFDocument6 pagesList of Stock Exchanges in The World PDFBinod Kumar PadhiNo ratings yet

- Eliminating EntriesDocument81 pagesEliminating EntriesRose CastilloNo ratings yet

- Project Viability FinalDocument79 pagesProject Viability FinalkapilNo ratings yet

- Management ProjectDocument7 pagesManagement ProjectAanchal NarulaNo ratings yet

- Mechanics of Futures Markets ExplainedDocument23 pagesMechanics of Futures Markets ExplainedaliNo ratings yet

- Dividends For RetirementDocument2 pagesDividends For RetirementThad MalleyNo ratings yet

- A Study On Factors Influencing of Women Policyholder's Investment Decision Towards Life Insurance Corporation of India Policies in ChennaiDocument6 pagesA Study On Factors Influencing of Women Policyholder's Investment Decision Towards Life Insurance Corporation of India Policies in ChennaiarcherselevatorsNo ratings yet

- Financial Management Roles and PurposesDocument10 pagesFinancial Management Roles and Purposesifras1343No ratings yet

- Cfa Level III Errata PDFDocument7 pagesCfa Level III Errata PDFTran HongNo ratings yet