You might also like

- A Level Accounting 22 Nov2014Document16 pagesA Level Accounting 22 Nov2014Bin SaadunNo ratings yet

- 9706 s16 QP 22 PDFDocument16 pages9706 s16 QP 22 PDFFarrukhsgNo ratings yet

- 9706 s15 QP 21Document16 pages9706 s15 QP 21Mia0% (1)

- 9706 Y16 SP 2Document18 pages9706 Y16 SP 2Wi Mae RiNo ratings yet

- Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced LevelDocument18 pagesCambridge International Examinations Cambridge International Advanced Subsidiary and Advanced LevelsagarnitishpirtheeNo ratings yet

- 0452 s15 QP 21Document20 pages0452 s15 QP 21zuzoyopiNo ratings yet

- 9706 s12 QP 22Document16 pages9706 s12 QP 22Faisal RaoNo ratings yet

- 0452 s14 QP 11Document20 pages0452 s14 QP 11ATEFNo ratings yet

- A Level Accounting 23 Nov2014Document16 pagesA Level Accounting 23 Nov2014Bin SaadunNo ratings yet

- 0452 s13 QP 11Document20 pages0452 s13 QP 11Naðooshii AbdallahNo ratings yet

- 9706 s16 QP 32 PDFDocument12 pages9706 s16 QP 32 PDFFarrukhsgNo ratings yet

- 9706 s12 QP 42Document8 pages9706 s12 QP 42Adrian JosephianNo ratings yet

- 0452 s12 QP 22Document20 pages0452 s12 QP 22Faisal RaoNo ratings yet

- 0452 s15 QP 11Document24 pages0452 s15 QP 11zuzoyopiNo ratings yet

- Due Date: Tuesday September 30 (By 1:50 PM) : Intermediate Financial Accounting I - ADMN 3221H Accounting Assignment #2Document7 pagesDue Date: Tuesday September 30 (By 1:50 PM) : Intermediate Financial Accounting I - ADMN 3221H Accounting Assignment #2kaomsheartNo ratings yet

- 0452 s10 QP 11Document16 pages0452 s10 QP 11ATEF0% (1)

- 0452 w13 QP 11Document20 pages0452 w13 QP 11Naðooshii AbdallahNo ratings yet

- 0452 s13 QP 21Document20 pages0452 s13 QP 21Naðooshii AbdallahNo ratings yet

- Lcci 3012Document21 pagesLcci 3012alee200No ratings yet

- 7110 s09 QP 2Document20 pages7110 s09 QP 2mstudy123456100% (1)

- 0452 s14 QP 22Document20 pages0452 s14 QP 22simplesaiedNo ratings yet

- 0452 s15 QP 22Document20 pages0452 s15 QP 22zuzoyopiNo ratings yet

- 0452 s11 QP 13Document16 pages0452 s11 QP 13Athul TomyNo ratings yet

- 0452 s15 QP 12Document20 pages0452 s15 QP 12zuzoyopi0% (1)

- Cama PDFDocument15 pagesCama PDFChandrikaprasdNo ratings yet

- 7110 June 2006Document12 pages7110 June 2006Kristen NallanNo ratings yet

- 9706 s12 QP 43Document8 pages9706 s12 QP 43Adrian JosephianNo ratings yet

- 0452 s06 QP 2 PDFDocument12 pages0452 s06 QP 2 PDFAbirHudaNo ratings yet

- FM202 - Exam Q - 2011-2 - Financial Accounting 202 V3 - AM NV DRdocDocument6 pagesFM202 - Exam Q - 2011-2 - Financial Accounting 202 V3 - AM NV DRdocMaxine IgnatiukNo ratings yet

- Mock Test Paper 2Document7 pagesMock Test Paper 2FarrukhsgNo ratings yet

- Pathfinder NOV 2015 Skills LevelDocument210 pagesPathfinder NOV 2015 Skills LevelAnonymous nqukBeNo ratings yet

- 0452 w11 QP 13Document16 pages0452 w11 QP 13Faisal RaoNo ratings yet

- Exercise AC 518 2nd Sem 2016Document2 pagesExercise AC 518 2nd Sem 2016RALLISONNo ratings yet

- Chapter 15 16 Problems and AnswersDocument22 pagesChapter 15 16 Problems and AnswersPatch AureNo ratings yet

- Secimen: Advanced Gce AccountingDocument8 pagesSecimen: Advanced Gce Accountingaumit0099No ratings yet

- University of Cambridge International Examinations General Certificate of Education Advanced Subsidiary Level and Advanced LevelDocument8 pagesUniversity of Cambridge International Examinations General Certificate of Education Advanced Subsidiary Level and Advanced LevelSherjeel AhmedNo ratings yet

- 9706 w09 QP 42Document8 pages9706 w09 QP 42Shanavaz AsokachalilNo ratings yet

- 2016 Accountancy IDocument4 pages2016 Accountancy IDanish RazaNo ratings yet

- University of Cambridge International Examinations General Certificate of Education Advanced Subsidiary Level and Advanced LevelDocument16 pagesUniversity of Cambridge International Examinations General Certificate of Education Advanced Subsidiary Level and Advanced LevelTinyiko BandaNo ratings yet

- Chapter 15&16 Problems and AnswersDocument22 pagesChapter 15&16 Problems and AnswersMa-an Maroma100% (10)

- Financial Results For March 31, 2015 (Audited) (Result)Document12 pagesFinancial Results For March 31, 2015 (Audited) (Result)Shyam SunderNo ratings yet

- Financial Results, Limited Review Report For December 31, 2015 (Result)Document4 pagesFinancial Results, Limited Review Report For December 31, 2015 (Result)Shyam SunderNo ratings yet

- 0452 s12 QP 23Document20 pages0452 s12 QP 23Faisal RaoNo ratings yet

- As Practice Paper 1Document10 pagesAs Practice Paper 1Farrukhsg100% (1)

- 7110 s08 QP 2Document16 pages7110 s08 QP 2Tayyab AbdullahNo ratings yet

- Iandfct2exam201504 0Document8 pagesIandfct2exam201504 0Patrick MugoNo ratings yet

- Advanced Financial Accounting - Paper 8 CPA PDFDocument10 pagesAdvanced Financial Accounting - Paper 8 CPA PDFAhmed Suleyman100% (1)

- Standalone & Consolidated Financial Results, Limited Review Report For December 31, 2016 (Result)Document9 pagesStandalone & Consolidated Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Suggested Answer - Syl12 - Jun2014 - Paper - 19 Final Examination: Suggested Answers To QuestionsDocument15 pagesSuggested Answer - Syl12 - Jun2014 - Paper - 19 Final Examination: Suggested Answers To QuestionsMdAnjum1991No ratings yet

- Section A (20 Marks)Document11 pagesSection A (20 Marks)Taha NasirNo ratings yet

- AC1025 ZA d1Document12 pagesAC1025 ZA d1Amna AnwarNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2016 EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2016 EditionNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2018 EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2018 EditionNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Oil Well, Refinery Machinery & Equipment Wholesale Revenues World Summary: Market Values & Financials by CountryFrom EverandOil Well, Refinery Machinery & Equipment Wholesale Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Computerised Accounting Practice Set Using Xero Online Accounting: Australian EditionFrom EverandComputerised Accounting Practice Set Using Xero Online Accounting: Australian EditionNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Tangazo La Ajira Za Kazi Za Mkataba Tanganyika DCDocument6 pagesTangazo La Ajira Za Kazi Za Mkataba Tanganyika DCBin SaadunNo ratings yet

- Informator Studia W SGH Po AngielskuDocument40 pagesInformator Studia W SGH Po AngielskuBin SaadunNo ratings yet

- Advert Driver 2023Document3 pagesAdvert Driver 2023Bin SaadunNo ratings yet

- Program Assistant Job Description 1Document2 pagesProgram Assistant Job Description 1Bin SaadunNo ratings yet

- Apc VacanciesDocument7 pagesApc VacanciesBin SaadunNo ratings yet

- Aecf Vacancy MarchDocument5 pagesAecf Vacancy MarchBin SaadunNo ratings yet

- SNR Internal Auditor 1712298427Document2 pagesSNR Internal Auditor 1712298427Bin SaadunNo ratings yet

- Final WAJIBUs Annual Report 2020 - OPDocument90 pagesFinal WAJIBUs Annual Report 2020 - OPBin SaadunNo ratings yet

- SNV New VacanciesDocument5 pagesSNV New VacanciesBin SaadunNo ratings yet

- Foundations of Leaving CareDocument8 pagesFoundations of Leaving CareBin SaadunNo ratings yet

- ICAP JD - Senior Finance ManagerDocument4 pagesICAP JD - Senior Finance ManagerBin SaadunNo ratings yet

- TZ Staff Benefits Summary RecruitmentDocument5 pagesTZ Staff Benefits Summary RecruitmentBin SaadunNo ratings yet

- Program Assistant - Job DescriptionDocument2 pagesProgram Assistant - Job DescriptionBin SaadunNo ratings yet

- The Way You Do Anything Is The Way You Do EverythingDocument1 pageThe Way You Do Anything Is The Way You Do EverythingBin SaadunNo ratings yet

- CIA Exam Preparation Part 1 Essentials of Internal AuditingDocument4 pagesCIA Exam Preparation Part 1 Essentials of Internal AuditingBin Saadun100% (1)

- Land Cruiser 78: Grade SFXDocument2 pagesLand Cruiser 78: Grade SFXBin SaadunNo ratings yet

- CIA TOCs 3part PDFDocument6 pagesCIA TOCs 3part PDFBin SaadunNo ratings yet

- (NBAA) The National Board of Accountants and Auditors TanzaniaDocument2 pages(NBAA) The National Board of Accountants and Auditors TanzaniaBin SaadunNo ratings yet

- Audit and Assurance (Int) - SQBDocument190 pagesAudit and Assurance (Int) - SQBBin SaadunNo ratings yet

- Honda Click 110 Service Manual EngDocument104 pagesHonda Click 110 Service Manual EngBin SaadunNo ratings yet

- AHMIGOM 2nded 2013 PDFDocument142 pagesAHMIGOM 2nded 2013 PDFBin SaadunNo ratings yet

- How To Prepare Economy? Exam Microeconomics Macroecono Mics Indian EconomyDocument8 pagesHow To Prepare Economy? Exam Microeconomics Macroecono Mics Indian EconomyAchuth GangadharanNo ratings yet

- Project Costing PDFDocument30 pagesProject Costing PDFJohn StephensNo ratings yet

- List of Books by Author Steven M. BraggDocument5 pagesList of Books by Author Steven M. BraggAriyanto100% (1)

- Par CorDocument11 pagesPar CorIts meh Sushi100% (1)

- Komal Jeevan (Table No. 159)Document15 pagesKomal Jeevan (Table No. 159)Kshitiz RastogiNo ratings yet

- Synergy of High Net-Worth Individuals (Hnis) With Their Distribution ChannelDocument69 pagesSynergy of High Net-Worth Individuals (Hnis) With Their Distribution Channelkaushal_sharmaNo ratings yet

- Chatham Lodging TrustDocument5 pagesChatham Lodging Trustpresentation111No ratings yet

- Investing in MusicDocument32 pagesInvesting in MusicBMX Entertainment CorporationNo ratings yet

- Underwriting Placements and The Art of Investor Relations Presentation by Sherilyn Foong Alliance Investment Bank Berhad MalaysiaDocument25 pagesUnderwriting Placements and The Art of Investor Relations Presentation by Sherilyn Foong Alliance Investment Bank Berhad MalaysiaPramod GosaviNo ratings yet

- Retirements: A Guide To The Younger GenerationsDocument50 pagesRetirements: A Guide To The Younger GenerationsnanaappiahNo ratings yet

- Financial Statements Analysis Case StudyDocument17 pagesFinancial Statements Analysis Case StudychrisNo ratings yet

- International Capital Burgeting AssignmentDocument22 pagesInternational Capital Burgeting AssignmentHitesh Kumar100% (1)

- Capital Budgeting Example ExcelDocument1 pageCapital Budgeting Example ExcelNgoc Hong DuongNo ratings yet

- Foreclosures-Don Quixote Law SchoolDocument74 pagesForeclosures-Don Quixote Law SchoolTommy Jefferson100% (3)

- Pilipinas Shell Petroleum CorporationDocument4 pagesPilipinas Shell Petroleum Corporation레미렘100% (1)

- Comparative Analysia of MF Reported by ARCHANA.KDocument78 pagesComparative Analysia of MF Reported by ARCHANA.KMartha PraveenNo ratings yet

- Jump Start: Log in or Join PMI To Gain AccessDocument6 pagesJump Start: Log in or Join PMI To Gain AccessJ. ZhouNo ratings yet

- GBM 1 31 07Document11 pagesGBM 1 31 07cmu_ufaNo ratings yet

- Project ReportDocument11 pagesProject Reportzahid mehmoodNo ratings yet

- The Role of Managerial Finance: All Rights ReservedDocument45 pagesThe Role of Managerial Finance: All Rights ReservedmoonaafreenNo ratings yet

- Rothschild Owned Blackst... Ts Say - IntellihubDocument8 pagesRothschild Owned Blackst... Ts Say - IntellihubSimon Jones100% (1)

- Gamboa v. Teves DigestDocument3 pagesGamboa v. Teves DigestLaurice Claire C. Peñamante100% (2)

- International Corporate Business Development in Malmo Sweden Resume Jesper FrantzichDocument3 pagesInternational Corporate Business Development in Malmo Sweden Resume Jesper FrantzichJesperFrantzichNo ratings yet

- Final Exam in Taxation AccountingDocument5 pagesFinal Exam in Taxation AccountingMarvin CeledioNo ratings yet

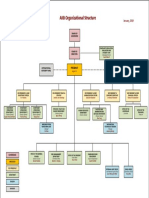

- AIIB Organizational StructureDocument1 pageAIIB Organizational StructureAbi S. BCanNo ratings yet

- Euromoney Institutional Investor PLC The Journal of Private EquityDocument11 pagesEuromoney Institutional Investor PLC The Journal of Private EquityJean Pierre BetancourthNo ratings yet

- RBS Internship ReportDocument61 pagesRBS Internship ReportWaqas javed100% (3)

- Order in Respect of Mangalam Agro Products LimitedDocument15 pagesOrder in Respect of Mangalam Agro Products LimitedShyam SunderNo ratings yet

- Venture Capital Q2 2016Document1 pageVenture Capital Q2 2016BayAreaNewsGroup100% (2)

- RIA ComplianceDocument3 pagesRIA ComplianceriacomplianceNo ratings yet