You might also like

- 2018 TaxReturn PDFDocument139 pages2018 TaxReturn PDFGregory GoodNo ratings yet

- Emirates SWOT Analysis Reveals Strong Government Support and Effective BrandingDocument4 pagesEmirates SWOT Analysis Reveals Strong Government Support and Effective BrandingWan SajaNo ratings yet

- Emirates SWOT Analysis Reveals Strong Government Support and Effective BrandingDocument4 pagesEmirates SWOT Analysis Reveals Strong Government Support and Effective BrandingWan SajaNo ratings yet

- Announces Q2 Results, Results Press Release & Auditors Report For September 30, 2015 (Result)Document15 pagesAnnounces Q2 Results, Results Press Release & Auditors Report For September 30, 2015 (Result)Shyam SunderNo ratings yet

- Moderator: Mr. L.J. Muthivhi (CA), SADocument11 pagesModerator: Mr. L.J. Muthivhi (CA), SANhlanhla MsizaNo ratings yet

- MSME (Micro, Small and Medium Enterprises)Document6 pagesMSME (Micro, Small and Medium Enterprises)ISU MITTALNo ratings yet

- EO 156 - Restructuring of The Motor Vehicle Development ProgDocument13 pagesEO 156 - Restructuring of The Motor Vehicle Development ProgPrince PersiaNo ratings yet

- Procedure For Prod - CertificateDocument166 pagesProcedure For Prod - CertificatePonduru TirmualaNo ratings yet

- CENVAT Credit: Understanding the Recent AmendmentsDocument8 pagesCENVAT Credit: Understanding the Recent Amendmentsraju7971No ratings yet

- Taxation (Pakistan) : Monday 2 June 2008Document13 pagesTaxation (Pakistan) : Monday 2 June 2008Uma Shankar JaiswalNo ratings yet

- PR3 2011 Investment Holding CompanyDocument27 pagesPR3 2011 Investment Holding CompanypsteohNo ratings yet

- 7 AnnexureDocument31 pages7 AnnexurePitamber ShakyaNo ratings yet

- Notes - Capital AllowanceDocument8 pagesNotes - Capital AllowanceDIVA RTHININo ratings yet

- WB Incentive Scheme As On 22 May 2015Document44 pagesWB Incentive Scheme As On 22 May 2015Sanjay SethiaNo ratings yet

- Inland Revenue Board Malaysia: Public Ruling No. 3/2011Document27 pagesInland Revenue Board Malaysia: Public Ruling No. 3/2011Lawrence Lau U HaoNo ratings yet

- General MSME Frequently Asked Questions: Manufacturing SectorDocument33 pagesGeneral MSME Frequently Asked Questions: Manufacturing SectorRamyaMeenakshiNo ratings yet

- Public Ruling No. 11 - 2018 - Withholding Tax On Special Classses of IncomeDocument25 pagesPublic Ruling No. 11 - 2018 - Withholding Tax On Special Classses of IncomeNorsalzarinaNo ratings yet

- EoDB Intiatives 11december2015Document5 pagesEoDB Intiatives 11december2015Shabir TrambooNo ratings yet

- Tutorial 3 (1) Q1,2,4,5Document9 pagesTutorial 3 (1) Q1,2,4,5Shan JeefNo ratings yet

- General Guidelines for PETRONAS Licensing and RegistrationDocument36 pagesGeneral Guidelines for PETRONAS Licensing and RegistrationHabib Mukmin100% (1)

- Executive Order No.877-A - Comprehensive Motor Vehicle Development Program - 03.06.2003 - 0Document17 pagesExecutive Order No.877-A - Comprehensive Motor Vehicle Development Program - 03.06.2003 - 0SamJadeGadianeNo ratings yet

- 7 Annexure A 6.indDocument46 pages7 Annexure A 6.indtonyvgeorgeNo ratings yet

- Bharat Telecom LTD Condensed Audited Financial Statements For The Year Ended 31 March 2015Document1 pageBharat Telecom LTD Condensed Audited Financial Statements For The Year Ended 31 March 2015L'express MauriceNo ratings yet

- Automobile Industry - Some Economic PoliciesDocument4 pagesAutomobile Industry - Some Economic PoliciesRenu PratapNo ratings yet

- Taxation Answers and Marking Scheme6,719,75018,000,000180,0001,126,913Document12 pagesTaxation Answers and Marking Scheme6,719,75018,000,000180,0001,126,913abby bendarasNo ratings yet

- Guide On Motor Vehicle Services or Repair CentreDocument10 pagesGuide On Motor Vehicle Services or Repair CentreggNo ratings yet

- ICV Supplier Certification Guidelines OCT 2023Document30 pagesICV Supplier Certification Guidelines OCT 2023Noori Zahoor KhanNo ratings yet

- 2012 Malaysian Budget Tax HighlightsDocument14 pages2012 Malaysian Budget Tax HighlightsCathy WongNo ratings yet

- MSME Registration and BenefitsDocument41 pagesMSME Registration and BenefitsRajeevChandNo ratings yet

- Advanced Taxation (Malaysia) : Professional Pilot Paper - Options ModuleDocument20 pagesAdvanced Taxation (Malaysia) : Professional Pilot Paper - Options ModuleTang Swee ChanNo ratings yet

- CENVAT Credit PDFDocument177 pagesCENVAT Credit PDFkgsanghaviNo ratings yet

- Executive Order 156 Provides Comprehensive Industrial Policy for Motor Vehicle DevelopmentDocument17 pagesExecutive Order 156 Provides Comprehensive Industrial Policy for Motor Vehicle DevelopmentWally Ann YumulNo ratings yet

- Inland Revenue Board of Malaysia: Public Ruling No. 10/2015Document26 pagesInland Revenue Board of Malaysia: Public Ruling No. 10/2015Ken ChiaNo ratings yet

- Advanced Financial Accounting - Paper 8 CPA PDFDocument10 pagesAdvanced Financial Accounting - Paper 8 CPA PDFAhmed Suleyman100% (1)

- Irr Eo 156Document13 pagesIrr Eo 156Jennifer AndoNo ratings yet

- WPPF and WWF (As Per Labour Law and Rules Amended Upto Sept 2015) Accountants PerspectiveDocument29 pagesWPPF and WWF (As Per Labour Law and Rules Amended Upto Sept 2015) Accountants PerspectiveFahim Khan0% (1)

- Sidco Functions and SchemesDocument11 pagesSidco Functions and SchemesKarthikacauraNo ratings yet

- Talgo 1H2015 Results PresentationDocument18 pagesTalgo 1H2015 Results PresentationTail RiskNo ratings yet

- Heavy InduDocument6 pagesHeavy Indumvnreddy.111No ratings yet

- Executive Summary: in Thousands of PesosDocument6 pagesExecutive Summary: in Thousands of PesosDAS MAGNo ratings yet

- Accounts Manual - Part 1Document28 pagesAccounts Manual - Part 1Kiran KothariNo ratings yet

- Amendments in CA Final Direct Tax For May 2015Document127 pagesAmendments in CA Final Direct Tax For May 2015sourabh singlaNo ratings yet

- Royal Malaysian Customs: Guide Approved Trader SchemeDocument16 pagesRoyal Malaysian Customs: Guide Approved Trader SchemetenglumlowNo ratings yet

- Suggested Answer - Syl12 - Jun2014 - Paper - 19 Final Examination: Suggested Answers To QuestionsDocument15 pagesSuggested Answer - Syl12 - Jun2014 - Paper - 19 Final Examination: Suggested Answers To QuestionsMdAnjum1991No ratings yet

- Arl Internship ReportDocument19 pagesArl Internship ReportChaudhry RashidNo ratings yet

- GuidelinesDocument12 pagesGuidelinesSANJAY AGARWALNo ratings yet

- Government of India Central Capital Investment Subsidy Scheme DetailsDocument72 pagesGovernment of India Central Capital Investment Subsidy Scheme DetailsMohiuddin AnsariNo ratings yet

- F6 Pilot PaperDocument19 pagesF6 Pilot PaperSoon SiongNo ratings yet

- CAF7-Financial Accounting and Reporting II - QuestionbankDocument250 pagesCAF7-Financial Accounting and Reporting II - QuestionbankEvan Jones100% (7)

- Other Tax and Investment DevelopmentsDocument21 pagesOther Tax and Investment DevelopmentsShandru MurthyNo ratings yet

- ICAI CAT Course DetailsDocument2 pagesICAI CAT Course DetailsVishu VishwaroopNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- 2.6 or 5.1 - Subsidies - SN - July 2016Document17 pages2.6 or 5.1 - Subsidies - SN - July 2016Starlet PearlNo ratings yet

- FDBDNZFGMJFH MdsfsdfsDocument187 pagesFDBDNZFGMJFH Mdsfsdfsshri100% (1)

- Manual ON Foreign Direct Investment IN IndiaDocument103 pagesManual ON Foreign Direct Investment IN Indiacoolnik007No ratings yet

- External Guidelines SAG MADANI 24Oct2023Document9 pagesExternal Guidelines SAG MADANI 24Oct2023Kambing ButaNo ratings yet

- SUMMARYDocument5 pagesSUMMARYADARSH PATTARNo ratings yet

- SMEDA Business Guide Series: Procedure For Claiming Duty DrawbacksDocument27 pagesSMEDA Business Guide Series: Procedure For Claiming Duty DrawbacksAnas AnsariNo ratings yet

- Cost Records and Cost Audit Applicability - Companies Act - IndiaFilingsDocument6 pagesCost Records and Cost Audit Applicability - Companies Act - IndiaFilingsShaik MastanvaliNo ratings yet

- Sup May 2016Document170 pagesSup May 2016Rocky RkNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- International Public Sector Accounting Standards Implementation Road Map for UzbekistanFrom EverandInternational Public Sector Accounting Standards Implementation Road Map for UzbekistanNo ratings yet

- Policies to Support the Development of Indonesia’s Manufacturing Sector during 2020–2024: A Joint ADB–BAPPENAS ReportFrom EverandPolicies to Support the Development of Indonesia’s Manufacturing Sector during 2020–2024: A Joint ADB–BAPPENAS ReportNo ratings yet

- Emirate SDDocument11 pagesEmirate SDWan SajaNo ratings yet

- Emiratesppt 130619105244 Phpapp01Document22 pagesEmiratesppt 130619105244 Phpapp01msy1991No ratings yet

- Emirates Airlines: The Finest in the SkyDocument22 pagesEmirates Airlines: The Finest in the SkyNiraj DesaiNo ratings yet

- Swot of Emirates AirlinesDocument2 pagesSwot of Emirates Airlinesdilip504No ratings yet

- IRS Form 1040es 2016Document12 pagesIRS Form 1040es 2016Freeman Lawyer100% (1)

- AccountingDocument5 pagesAccountingAAAAANo ratings yet

- Salary Slip Format in PDF All PDFDocument3 pagesSalary Slip Format in PDF All PDFRajeev GunasekaranNo ratings yet

- India: What Is The TDS and Income Tax System in India?Document5 pagesIndia: What Is The TDS and Income Tax System in India?Ketan JajuNo ratings yet

- Taxation Comprehensive Exam TosDocument2 pagesTaxation Comprehensive Exam Tosaccounting probNo ratings yet

- Introduction To Income Tax Integ REVISED 2022 1Document14 pagesIntroduction To Income Tax Integ REVISED 2022 1brr brrNo ratings yet

- Batch 6 CompleteDocument98 pagesBatch 6 CompleteAlexis Von TeNo ratings yet

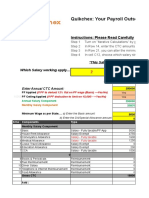

- Quikchex CTC Calculator AprilDocument8 pagesQuikchex CTC Calculator Aprilravipati46No ratings yet

- SEction 110 of The NIRC of 1977Document2 pagesSEction 110 of The NIRC of 1977Tyrone HernandezNo ratings yet

- Develop Understanding of TaxationDocument89 pagesDevelop Understanding of TaxationEyob kefle100% (1)

- Parent Involvement and Community Partnership: Doris J. Yu School Head, TnhsDocument63 pagesParent Involvement and Community Partnership: Doris J. Yu School Head, TnhsTupsan Nhs Mambajao CamiguinNo ratings yet

- Payslip Sep-2022 NareshDocument3 pagesPayslip Sep-2022 NareshDharshan RajNo ratings yet

- Tax 2022Document6 pagesTax 2022kateNo ratings yet

- Train LawDocument41 pagesTrain LawJoana Lyn GalisimNo ratings yet

- G.R. No. 148187 April 16, 2008 Philex Mining Corporation, Petitioner, Commissioner of Internal Revenue, Respondent. Decision Ynares-Santiago, J.Document6 pagesG.R. No. 148187 April 16, 2008 Philex Mining Corporation, Petitioner, Commissioner of Internal Revenue, Respondent. Decision Ynares-Santiago, J.Jhoi MateoNo ratings yet

- Tax ReviewerDocument180 pagesTax Reviewertdh1023No ratings yet

- NEU Taxation Law Pre-Week Notes PDFDocument35 pagesNEU Taxation Law Pre-Week Notes PDFKin Pearly FloresNo ratings yet

- Tax Evasion Vs Tax AvoidanceDocument2 pagesTax Evasion Vs Tax AvoidanceNurse NotesNo ratings yet

- 1702-EX Jan 2018 ENCS Final v3 PDFDocument3 pages1702-EX Jan 2018 ENCS Final v3 PDFLuz SudarioNo ratings yet

- Individual Income Tax Return for Tax Year 2019Document48 pagesIndividual Income Tax Return for Tax Year 2019Mirza Naseer AbbasNo ratings yet

- Basic Terminologies Basic Terminologies: Estate Tax Estate TaxDocument52 pagesBasic Terminologies Basic Terminologies: Estate Tax Estate TaxFrances Marella CristobalNo ratings yet

- Vsa Taxation Incometaxation Part4.1 MCQ 1Document18 pagesVsa Taxation Incometaxation Part4.1 MCQ 1lopa.palis.uiNo ratings yet

- Estate Tax ComputationDocument11 pagesEstate Tax ComputationNorfaidah Didato GogoNo ratings yet

- Assessment of Individual's Income Tax in India: January 2018Document4 pagesAssessment of Individual's Income Tax in India: January 2018Jai VermaNo ratings yet

- Nolo Complete Books-in-Print 2010-2011Document52 pagesNolo Complete Books-in-Print 2010-2011Nolo100% (2)

- Church of Pentecost South Africa Financial StatementsDocument5 pagesChurch of Pentecost South Africa Financial StatementsEnoch AbasseyNo ratings yet

- Principles of Taxation For Business and Investment Planning 16th Edition Jones Test Bank 1Document36 pagesPrinciples of Taxation For Business and Investment Planning 16th Edition Jones Test Bank 1shannonwaltersqwdifntckm100% (27)

- 1 - Payslip - July 2020Document2 pages1 - Payslip - July 2020B.GOUTHAM SABARIESNo ratings yet

- M/s Skarpsinne Infotech Private Limited, A Company Registered Under TheDocument5 pagesM/s Skarpsinne Infotech Private Limited, A Company Registered Under ThePrejith SajeevNo ratings yet