You might also like

- NPS - Income Tax Deduction Under Section 80CCC and 80CCDDocument5 pagesNPS - Income Tax Deduction Under Section 80CCC and 80CCDManoj KakkarNo ratings yet

- NPS - Sec 80CCD - Additional Deduction For National Pension System ContributionDocument2 pagesNPS - Sec 80CCD - Additional Deduction For National Pension System ContributionManoj KakkarNo ratings yet

- 16 Deductions Under Chapter ViaDocument89 pages16 Deductions Under Chapter ViabinoygnairNo ratings yet

- Salary. 192.: B.-Deduction at SourceDocument3 pagesSalary. 192.: B.-Deduction at SourceJeremy RemlalfakaNo ratings yet

- Deduction in Respect of Contribution To Certain Pension FundsDocument1 pageDeduction in Respect of Contribution To Certain Pension FundsalisagasaNo ratings yet

- Sec 201 - Failure To Deduct or Pay TDS - Amendment On 1 July 2010 - Circular No. 1 2010Document1 pageSec 201 - Failure To Deduct or Pay TDS - Amendment On 1 July 2010 - Circular No. 1 2010Mohan ReddyNo ratings yet

- Section - 33ABADocument2 pagesSection - 33ABAwaqtkeebaatein12No ratings yet

- 80 CCGDocument1 page80 CCGDTPS SwitchyardNo ratings yet

- Budget 2015 Proposes Additional Deduction of Up To Rs. 50000/-Under Section 80CCD For National Pension System ContributionDocument1 pageBudget 2015 Proposes Additional Deduction of Up To Rs. 50000/-Under Section 80CCD For National Pension System ContributionalisagasaNo ratings yet

- Section - 36Document5 pagesSection - 36adipawar2824No ratings yet

- It - Rebates and ReliefsDocument5 pagesIt - Rebates and ReliefsJitendra VernekarNo ratings yet

- EPF SchemeDocument4 pagesEPF SchemeSnigdha MazumdarNo ratings yet

- Rules For NonATPDocument4 pagesRules For NonATPsmyns.bwNo ratings yet

- Salary Tax AssessmentDocument9 pagesSalary Tax Assessmentshuvo134No ratings yet

- Section 80cca Deduction in Respect of Deposits Under National Savings Scheme or Payment To A Deferred Annuity PlanDocument3 pagesSection 80cca Deduction in Respect of Deposits Under National Savings Scheme or Payment To A Deferred Annuity PlanParul NayakNo ratings yet

- DeductionsDocument42 pagesDeductionsNithya RajNo ratings yet

- Withholding On Wages SEC. 78. Definitions. - As Used in This ChapterDocument5 pagesWithholding On Wages SEC. 78. Definitions. - As Used in This ChaptershakiraNo ratings yet

- Deduction for medical insurance and treatment under Section 80D and 80DDBDocument3 pagesDeduction for medical insurance and treatment under Section 80D and 80DDBVijayaraj KvrNo ratings yet

- Expenses Regarding Service Tax Return Submited by Babai in The Month of June - 09Document13 pagesExpenses Regarding Service Tax Return Submited by Babai in The Month of June - 09mdbalajeeNo ratings yet

- Deductions Under Chapter VI ADocument6 pagesDeductions Under Chapter VI AbabatoofaniNo ratings yet

- TDS Not DeductDocument6 pagesTDS Not DeductAnil WayanadNo ratings yet

- As May Be PrescribedDocument2 pagesAs May Be PrescribedHARSHANo ratings yet

- Section 139Document9 pagesSection 139Mkv Downloader2No ratings yet

- ST THDocument3 pagesST THDhananjaya MnNo ratings yet

- Section - 35ACDocument2 pagesSection - 35ACwaqtkeebaatein12No ratings yet

- Employees Deposit Linked Insurance Scheme, EDLIS Scheme, 1976Document6 pagesEmployees Deposit Linked Insurance Scheme, EDLIS Scheme, 1976paragranjitNo ratings yet

- 81.tax Treatment On Compulsory Acquisition of LandDocument6 pages81.tax Treatment On Compulsory Acquisition of Landchandra sekhara reddy AlluNo ratings yet

- Question:-Q Write Note On Deduction U/s 80 C To 80 UDocument15 pagesQuestion:-Q Write Note On Deduction U/s 80 C To 80 UnikhilNo ratings yet

- SchedulefileDocument6 pagesSchedulefile27-Deekshitha Preeth JayaramNo ratings yet

- 12 Chapter 5Document99 pages12 Chapter 5Pavan SAMEER KUMARNo ratings yet

- 5.3 Exemptions From Income From SalariesDocument3 pages5.3 Exemptions From Income From SalariesYash DedhiaNo ratings yet

- 31188sm DTL Finalnew-May-Nov14 Cp28Document66 pages31188sm DTL Finalnew-May-Nov14 Cp28gvcNo ratings yet

- Deduction of Tax at Source - BComDocument8 pagesDeduction of Tax at Source - BComAniket AgrawalNo ratings yet

- Income Tax Act AmendmentsDocument8 pagesIncome Tax Act AmendmentsShrikanth SKNo ratings yet

- The Companies (Profits) Surtax Act, 1964Document16 pagesThe Companies (Profits) Surtax Act, 1964Mrigendra MishraNo ratings yet

- Chapter 2Document9 pagesChapter 2Paym entNo ratings yet

- Income Tax Cia 2 Differences in Financial Bill of 2009 and 2011Document7 pagesIncome Tax Cia 2 Differences in Financial Bill of 2009 and 2011karandutt69No ratings yet

- It Computation As Per Sec 115bacDocument2 pagesIt Computation As Per Sec 115bacDivyaNo ratings yet

- 80TTB - Provides Deduction Benefit On Interest Income For Senior CitizensDocument1 page80TTB - Provides Deduction Benefit On Interest Income For Senior CitizensArjun VermaNo ratings yet

- Section 247. General Provisions. - : Sections 247-252, Tax CodeDocument2 pagesSection 247. General Provisions. - : Sections 247-252, Tax CodeEdward Kenneth KungNo ratings yet

- 44ad 2019Document2 pages44ad 2019dipak300pawarNo ratings yet

- 67.calculation of Relief Under Sections 89 89ADocument5 pages67.calculation of Relief Under Sections 89 89ARaghu SNNo ratings yet

- Income Tax Provision For Charitable Trust-1Document106 pagesIncome Tax Provision For Charitable Trust-1Gargi BasuNo ratings yet

- 3676 - NON Resident ReliefDocument7 pages3676 - NON Resident ReliefSankarson BhattacharyaNo ratings yet

- Advance Payment of TaxDocument35 pagesAdvance Payment of TaxTrapti Garg Goyal0% (1)

- Income Tax Amendments for Individuals, HUF, Companies and Charitable TrustsDocument13 pagesIncome Tax Amendments for Individuals, HUF, Companies and Charitable TrustsRashi ViRdiNo ratings yet

- Asifamin - 3179 - 18893 - 6 - Taxation Pakistan - Session-08 PDFDocument18 pagesAsifamin - 3179 - 18893 - 6 - Taxation Pakistan - Session-08 PDFaemanNo ratings yet

- Analysis of Changes Introduced in The Lok Sabha-Approved Finance Bill 2023Document20 pagesAnalysis of Changes Introduced in The Lok Sabha-Approved Finance Bill 2023BuntyNo ratings yet

- Major Changes of Finance ActDocument5 pagesMajor Changes of Finance ActJulia RobertNo ratings yet

- Explanation.-For The Purposes of This Sub-Section, The Term "Unit" Shall Have The Same Meaning As Assigned To It in Clause (ZC) ofDocument1 pageExplanation.-For The Purposes of This Sub-Section, The Term "Unit" Shall Have The Same Meaning As Assigned To It in Clause (ZC) ofashim1No ratings yet

- Section 194Q - TDS On Certain PurchasesDocument1 pageSection 194Q - TDS On Certain PurchasesNishanth JoseNo ratings yet

- GST 31.03.17 Itc Rules PDFDocument9 pagesGST 31.03.17 Itc Rules PDFParthibanNo ratings yet

- EDLI New Rule 2021Document2 pagesEDLI New Rule 2021M NageshNo ratings yet

- Q. What Is The Tax Implication On Surrender of Pension Plans?Document1 pageQ. What Is The Tax Implication On Surrender of Pension Plans?Harik CNo ratings yet

- 34564rtp Nov14 Ipcc-4Document59 pages34564rtp Nov14 Ipcc-4Deepal DhamejaNo ratings yet

- A Book: Integrated Professional Competency Course (IPCC) Paper - 1: AccountingDocument12 pagesA Book: Integrated Professional Competency Course (IPCC) Paper - 1: AccountingSipoy SatishNo ratings yet

- Section 40Document4 pagesSection 40Anil MathewNo ratings yet

- Agenda Item 2 (2) - ITC RulesDocument9 pagesAgenda Item 2 (2) - ITC Rulesfintech ConsultancyNo ratings yet

- Payment of Bonus Act, 1965Document33 pagesPayment of Bonus Act, 1965Adya GoswamiNo ratings yet

- RTI Mumbai PoliceDocument90 pagesRTI Mumbai Policenahar_sv1366No ratings yet

- Juvenile Justice Bill 2014Document69 pagesJuvenile Justice Bill 2014nahar_sv1366No ratings yet

- Case Laws On Well Used Term - It Is Well Settled ThatDocument240 pagesCase Laws On Well Used Term - It Is Well Settled Thatnahar_sv1366No ratings yet

- AIR 1989 SC 1239 - Jurisdiction - Where Contract Made or Breached - Can Be Conferred by Contract To Any One of The Courts Where Cause of Action ArisesDocument8 pagesAIR 1989 SC 1239 - Jurisdiction - Where Contract Made or Breached - Can Be Conferred by Contract To Any One of The Courts Where Cause of Action Arisesnahar_sv1366No ratings yet

- Bail OrderDocument39 pagesBail Ordernahar_sv1366No ratings yet

- Hya Vishwachi KodiDocument1 pageHya Vishwachi Kodinahar_sv1366No ratings yet

- ADSI 2014-Accidental Deaths & Suicides in IndiaDocument322 pagesADSI 2014-Accidental Deaths & Suicides in Indianahar_sv1366No ratings yet

- HC Order 9 Sept 2015Document30 pagesHC Order 9 Sept 2015Moneylife Foundation100% (1)

- Maharashtra Right To Public Services Act, 2015Document11 pagesMaharashtra Right To Public Services Act, 2015nahar_sv1366No ratings yet

- Supreme Court Judgement On SaharaDocument28 pagesSupreme Court Judgement On Saharanahar_sv1366No ratings yet

- RBI NotificationDocument2 pagesRBI Notificationnahar_sv1366No ratings yet

- Sitting Judge of SC Opposes Plan To Name Home Secretary's Wife As J&K Judge - ETDocument2 pagesSitting Judge of SC Opposes Plan To Name Home Secretary's Wife As J&K Judge - ETnahar_sv1366No ratings yet

- 201404021712156212Document2 pages201404021712156212Nayana NayakNo ratings yet

- Offences and Prosecution Under Income Tax ActDocument8 pagesOffences and Prosecution Under Income Tax Actnahar_sv1366No ratings yet

- Code of Civil Procedure by Justice B S ChauhanDocument142 pagesCode of Civil Procedure by Justice B S Chauhannahar_sv1366100% (1)

- Marathi Numbers-1 To 100Document2 pagesMarathi Numbers-1 To 100nahar_sv136658% (97)

- TransNum Sep 14 104127Document1 pageTransNum Sep 14 1041273sha CEBREUSNo ratings yet

- Si04253409 4 PDFDocument1 pageSi04253409 4 PDFclintNo ratings yet

- Income Tax Appeal FormDocument2 pagesIncome Tax Appeal Formitat hyderabadNo ratings yet

- Korea tax rates and calculations for individuals and companiesDocument4 pagesKorea tax rates and calculations for individuals and companiesQuynh NguyenNo ratings yet

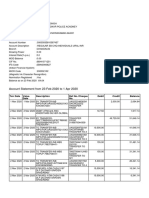

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument19 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balanceblinkfinance7No ratings yet

- CHAPTER 13 A - Regular Allowable Itemized DeductionsDocument4 pagesCHAPTER 13 A - Regular Allowable Itemized DeductionsDeviane CalabriaNo ratings yet

- Booktopia ChargingDocument1 pageBooktopia CharginguzairNo ratings yet

- Alnissiy Yemen - 04052018 Quo-33397 Batry + Spares YemenDocument2 pagesAlnissiy Yemen - 04052018 Quo-33397 Batry + Spares YemenSamir AjiNo ratings yet

- Vodafone bill details for Rs 638.76 chargesDocument2 pagesVodafone bill details for Rs 638.76 chargesRajneesh JhoradNo ratings yet

- 1 MondayDocument6 pages1 MondayCeline Marie Libatique AntonioNo ratings yet

- Mr. Shyam Singh's bank account statement and detailsDocument3 pagesMr. Shyam Singh's bank account statement and detailsShyamNo ratings yet

- Unicredit vs. IngDocument3 pagesUnicredit vs. IngAlina AndrioaeNo ratings yet

- Individual Tax Filing Guide for 2017Document8 pagesIndividual Tax Filing Guide for 2017deejay217No ratings yet

- Substantive Test: of TransactionsDocument56 pagesSubstantive Test: of Transactionsjoza100% (1)

- Online Tuition Fee Payment System for Philippine Christian UniversityDocument4 pagesOnline Tuition Fee Payment System for Philippine Christian UniversitydugongandmeNo ratings yet

- Local Charges / Service Fees Chile - Local Charges / Service FeesDocument3 pagesLocal Charges / Service Fees Chile - Local Charges / Service FeesFabiola FuentesNo ratings yet

- YatraDocument1 pageYatraANANTHAKRISHNANRRNo ratings yet

- Non - SDS ChecklistDocument2 pagesNon - SDS ChecklistAnkit GuptaNo ratings yet

- Accounting For Labor Part 2Document11 pagesAccounting For Labor Part 2Ghillian Mae GuiangNo ratings yet

- Calculate simple interest rates and amountsDocument9 pagesCalculate simple interest rates and amountsImtiaz AhmedNo ratings yet

- Composition Scheme Under GST 1.0Document28 pagesComposition Scheme Under GST 1.0Saqib AnsariNo ratings yet

- GSTR-1 07AUYPS5769G2ZJ March 2018-19Document41 pagesGSTR-1 07AUYPS5769G2ZJ March 2018-19Sachin SharmaNo ratings yet

- Exchange Rates for Mark to Market RevaluationDocument1 pageExchange Rates for Mark to Market RevaluationWendy WangNo ratings yet

- Problem 1 Current Liability Entries and Adjustments: InstructionsDocument6 pagesProblem 1 Current Liability Entries and Adjustments: Instructionsbeeeeee100% (1)

- Calculate Completing A 1040Document2 pagesCalculate Completing A 1040api-4921774500% (1)

- Tax Invoice for Sony HeadphonesDocument1 pageTax Invoice for Sony HeadphonesShyam SundarNo ratings yet

- Introduction to Plastic MoneyDocument70 pagesIntroduction to Plastic MoneyParm Sidhu100% (12)

- 返金規定 英語版 Refund policyDocument2 pages返金規定 英語版 Refund policyDai1 AcademyNo ratings yet

- Tax Exemptions and Deductions QuizDocument25 pagesTax Exemptions and Deductions QuizDanica VetuzNo ratings yet

- 02-2004 Vat Philippine Port Authority PpaDocument3 pages02-2004 Vat Philippine Port Authority Ppaapi-247793055No ratings yet