You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- PDF Processed With Cutepdf Evaluation EditionDocument3 pagesPDF Processed With Cutepdf Evaluation EditionShyam SunderNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Standalone Financial Results For September 30, 2016 (Result)Document3 pagesStandalone Financial Results For September 30, 2016 (Result)Shyam SunderNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Standalone Financial Results For March 31, 2016 (Result)Document11 pagesStandalone Financial Results For March 31, 2016 (Result)Shyam SunderNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Standalone Financial Results, Limited Review Report For June 30, 2016 (Result)Document3 pagesStandalone Financial Results, Limited Review Report For June 30, 2016 (Result)Shyam SunderNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Standalone Financial Results, Limited Review Report For September 30, 2016 (Result)Document4 pagesStandalone Financial Results, Limited Review Report For September 30, 2016 (Result)Shyam SunderNo ratings yet

- Transcript of The Investors / Analysts Con Call (Company Update)Document15 pagesTranscript of The Investors / Analysts Con Call (Company Update)Shyam SunderNo ratings yet

- Investor Presentation For December 31, 2016 (Company Update)Document27 pagesInvestor Presentation For December 31, 2016 (Company Update)Shyam SunderNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document4 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Law On Charity and Sponsorship LithuaniaDocument4 pagesLaw On Charity and Sponsorship LithuaniaRosa Martin HuelvesNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Peshawar Electric Supply Company: Say No To CorruptionDocument2 pagesPeshawar Electric Supply Company: Say No To CorruptionRiaz Ul HaqNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- H. R. LL: A BillDocument5 pagesH. R. LL: A Billakctan19946No ratings yet

- Price ListDocument28 pagesPrice ListBrandon BarndtNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- De 231 EpDocument5 pagesDe 231 Epvijaybhaskar damireddyNo ratings yet

- Income Taxation On Corporations Exercise ProblemsDocument2 pagesIncome Taxation On Corporations Exercise ProblemsRico, Jalaica B.No ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Concepts in Federal Taxation 2017 24th Edition Murphy Solutions Manual 1Document73 pagesConcepts in Federal Taxation 2017 24th Edition Murphy Solutions Manual 1hiedi100% (35)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Tata Steel FP - SPC - TSPDL Bara-Tspdl HR-HR Slit-Hr Coil-22.06.2022 - 97713 - 2.00Document14 pagesTata Steel FP - SPC - TSPDL Bara-Tspdl HR-HR Slit-Hr Coil-22.06.2022 - 97713 - 2.00tata steeljsrNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- 60 Sales Ideas That Really WorkDocument19 pages60 Sales Ideas That Really WorkAlfredo K Díaz de LeónNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

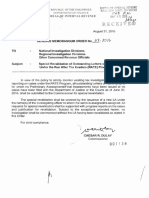

- RMO No. 57-2016 PDFDocument1 pageRMO No. 57-2016 PDFGabriel EdizaNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

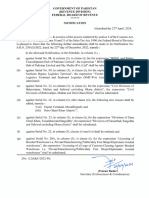

- 20244231544240339sro 614 (I) 2024Document1 page20244231544240339sro 614 (I) 2024BILWANI CONo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Format For Goods 1Document1 pageFormat For Goods 1Sanket PatelNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Industry of Hunger: Market Opportunity Within The U.S. Emergency Food Relief NetworkDocument22 pagesThe Industry of Hunger: Market Opportunity Within The U.S. Emergency Food Relief NetworkMattNo ratings yet

- Duplicate Receipt Dear Aditya Kumar PandeyDocument1 pageDuplicate Receipt Dear Aditya Kumar PandeyAdityaNo ratings yet

- Everytown Gun Safety Action Fund - 990 Tax FormDocument118 pagesEverytown Gun Safety Action Fund - 990 Tax FormCNBC.comNo ratings yet

- Computation of Income of A FirmDocument6 pagesComputation of Income of A FirmKhushbu GuptaNo ratings yet

- Deutsche Bank Ag Manila Branch vs. CirDocument2 pagesDeutsche Bank Ag Manila Branch vs. CirSalma Gurar100% (3)

- Indonesia 2nd Edition The Transfer Pricing Law ReviewDocument22 pagesIndonesia 2nd Edition The Transfer Pricing Law ReviewArianty Damaiance SilabanNo ratings yet

- Unit 2: Master Budget: An Overall Plan The Fundamentals of BudgetingDocument11 pagesUnit 2: Master Budget: An Overall Plan The Fundamentals of BudgetingbojaNo ratings yet

- PUBLIC PROCUREMENT. BPLM II, BPSAF II, BAC III - 2019 by Tubeti MwitaDocument539 pagesPUBLIC PROCUREMENT. BPLM II, BPSAF II, BAC III - 2019 by Tubeti MwitaFesto OtuomaNo ratings yet

- BBUS 470 Netptute Gourment Seafood CaseDocument10 pagesBBUS 470 Netptute Gourment Seafood CaseJohny FaulkNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- GlobalizationDocument24 pagesGlobalizationKate NguyenNo ratings yet

- Research On Taxation of Urban and Agricultural LandDocument2 pagesResearch On Taxation of Urban and Agricultural LandAnushka SharmaNo ratings yet

- Module2 AE26 ITDocument7 pagesModule2 AE26 ITJemalyn PiliNo ratings yet

- Tax Planning Tips For Property Investors Financial Year EndDocument1 pageTax Planning Tips For Property Investors Financial Year EndAdrianNo ratings yet

- Challenges of MNCsDocument15 pagesChallenges of MNCsdhaval_power123No ratings yet

- Accounting Exercises (Management Accounting)Document2 pagesAccounting Exercises (Management Accounting)arvin sibayan100% (1)

- LBR JWB Sesi 2 - BANDUNG COMPUTER - 2022Document12 pagesLBR JWB Sesi 2 - BANDUNG COMPUTER - 2022riyadiNo ratings yet

- Standard Means Test FormDocument2 pagesStandard Means Test FormNicole HernandezNo ratings yet

- AP Micro Syllabus - 20222023Document11 pagesAP Micro Syllabus - 20222023Sarah SeeharNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)