You might also like

- Principles of Exterior Drainage PDFDocument48 pagesPrinciples of Exterior Drainage PDFsushmak75% (4)

- Literature IntroDocument46 pagesLiterature IntrosushmakNo ratings yet

- 3 DB Ahm JRP CMV Intelligent Building 7-2-2014 LibreDocument16 pages3 DB Ahm JRP CMV Intelligent Building 7-2-2014 LibreVaishali MishraNo ratings yet

- Public Libraries, History and DevelopmentDocument50 pagesPublic Libraries, History and DevelopmentGeorgy Plekhanov100% (1)

- Impacts of Urbanization On Land Use Cover Changes and Itsprobable Implications On Local Climate and Groundwater LevelDocument3 pagesImpacts of Urbanization On Land Use Cover Changes and Itsprobable Implications On Local Climate and Groundwater LevelsushmakNo ratings yet

- Literature IntroDocument46 pagesLiterature IntrosushmakNo ratings yet

- Market Survey: E. Mohitha P. Mounika K. Sushma S. Bhagya Sri B. Naga DeepthiDocument16 pagesMarket Survey: E. Mohitha P. Mounika K. Sushma S. Bhagya Sri B. Naga DeepthisushmakNo ratings yet

- Chap 6Document29 pagesChap 6mayarayNo ratings yet

- Stormwater RunoffDocument15 pagesStormwater RunoffsushmakNo ratings yet

- Specification Items in The Last Column of Table 3Document2 pagesSpecification Items in The Last Column of Table 3sushmakNo ratings yet

- Stormwater Runoff PDFDocument29 pagesStormwater Runoff PDFmasoodaeNo ratings yet

- Us Fsi Breakthrough For Sustainability in Real Estate 051414 PDFDocument16 pagesUs Fsi Breakthrough For Sustainability in Real Estate 051414 PDFsushmakNo ratings yet

- Stormwater RunoffDocument15 pagesStormwater RunoffsushmakNo ratings yet

- Analyzing The SunDocument50 pagesAnalyzing The SunravikanthtumuluruNo ratings yet

- Building Construction: Working DrawingsDocument1 pageBuilding Construction: Working DrawingssushmakNo ratings yet

- Design of Green Building: A Case Study For Composite ClimateDocument6 pagesDesign of Green Building: A Case Study For Composite ClimatesushmakNo ratings yet

- Climate Responsive ArchDocument16 pagesClimate Responsive ArchsushmakNo ratings yet

- Neuman Hayner Architects Designs Conservatory in Israel Inspired by The Lines in Sheet MusicDocument3 pagesNeuman Hayner Architects Designs Conservatory in Israel Inspired by The Lines in Sheet MusicsushmakNo ratings yet

- PR ReportDocument1 pagePR ReportsushmakNo ratings yet

- FRM Dance Movmnt To Arch FormDocument110 pagesFRM Dance Movmnt To Arch FormsushmakNo ratings yet

- Architecture For Dance An Analysis of TR PDFDocument5 pagesArchitecture For Dance An Analysis of TR PDFsushmakNo ratings yet

- HoA SRDocument383 pagesHoA SRsushmakNo ratings yet

- Area statement-AD New PDFDocument36 pagesArea statement-AD New PDFsushmakNo ratings yet

- Climate Responsive ArchDocument100 pagesClimate Responsive ArcharchaikhNo ratings yet

- Building Construction: Working DrawingsDocument1 pageBuilding Construction: Working DrawingssushmakNo ratings yet

- Building Economics 2Document20 pagesBuilding Economics 2sushmakNo ratings yet

- Energy Efficient Materials ListDocument5 pagesEnergy Efficient Materials ListsushmakNo ratings yet

- Architecture For Dance An Analysis of TR PDFDocument5 pagesArchitecture For Dance An Analysis of TR PDFsushmakNo ratings yet

- VizinagaramDocument1 pageVizinagaramsushmakNo ratings yet

- QuestionnaireDocument2 pagesQuestionnairesushmakNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- In Re: Paul J. Mraz, James E. Mraz Heidi Pfisterer Mraz, His Wife v. Pauline M. Bright Sommers Enterprises, Incorporated Gordon Schmidt Coldwell Banker Residential Affiliates, Incorporated Aaron Chicovsky William Ross Pederson, and John Doe, Counter-Offerer, 46 F.3d 1125, 4th Cir. (1995)Document5 pagesIn Re: Paul J. Mraz, James E. Mraz Heidi Pfisterer Mraz, His Wife v. Pauline M. Bright Sommers Enterprises, Incorporated Gordon Schmidt Coldwell Banker Residential Affiliates, Incorporated Aaron Chicovsky William Ross Pederson, and John Doe, Counter-Offerer, 46 F.3d 1125, 4th Cir. (1995)Scribd Government DocsNo ratings yet

- Gujarat Technological University: Comprehensive Project ReportDocument32 pagesGujarat Technological University: Comprehensive Project ReportDharmesh PatelNo ratings yet

- Menu EngineeringDocument9 pagesMenu Engineeringfirstman31No ratings yet

- Management Theory and Practice - Chapter 1 - Session 1 PPT Dwtv9Ymol5Document35 pagesManagement Theory and Practice - Chapter 1 - Session 1 PPT Dwtv9Ymol5DHAVAL ABDAGIRI83% (6)

- Pharmaceutical Specialty Account Manager in Springfield MA Resume Richard PielaDocument2 pagesPharmaceutical Specialty Account Manager in Springfield MA Resume Richard PielaRichardPielaNo ratings yet

- Performance Analysis of Chinas Fast Fashion ClothDocument10 pagesPerformance Analysis of Chinas Fast Fashion ClothQuỳnh LêNo ratings yet

- Enhancing Analytical & Creative Thinking Skills PDFDocument2 pagesEnhancing Analytical & Creative Thinking Skills PDFsonypall3339No ratings yet

- Income Tax Banggawan2019 Ch9Document13 pagesIncome Tax Banggawan2019 Ch9Noreen Ledda83% (6)

- Canada Post Amended Statement of Claim Against Geolytica and Geocoder - CaDocument12 pagesCanada Post Amended Statement of Claim Against Geolytica and Geocoder - CaWilliam Wolfe-WylieNo ratings yet

- American Ambulette SchedulesDocument321 pagesAmerican Ambulette SchedulesMNCOOhioNo ratings yet

- G12 ABM Marketing Lesson 1 (Part 1)Document10 pagesG12 ABM Marketing Lesson 1 (Part 1)Leo SuingNo ratings yet

- SAP InvoiceDocument86 pagesSAP InvoicefatherNo ratings yet

- Deal or No Deal Tax 2 Quiz BeeDocument13 pagesDeal or No Deal Tax 2 Quiz BeeRebecca SisonNo ratings yet

- Sparsh Gupta AprDocument4 pagesSparsh Gupta Aprshivamtyagihpr001No ratings yet

- Design & Build Toyo Batangas WH Evaluation SUMMARYDocument1 pageDesign & Build Toyo Batangas WH Evaluation SUMMARYvina clarisse OsiasNo ratings yet

- Grievance Redrassal ManagementDocument71 pagesGrievance Redrassal ManagementAzaruddin Shaik B Positive0% (1)

- Executive Summary:: Advanced & Applied Business Research Pillsbury Cookie Challenge Due Date: 4 March 2013Document6 pagesExecutive Summary:: Advanced & Applied Business Research Pillsbury Cookie Challenge Due Date: 4 March 2013chacha_420100% (1)

- Chandelier Exit 26 Jun 2016Document4 pagesChandelier Exit 26 Jun 2016Rajan ChaudhariNo ratings yet

- Planning & Managing Inventory in Supply Chain: Cycle Inventory, Safety Inventory, ABC Inventory & Product AvailabilityDocument24 pagesPlanning & Managing Inventory in Supply Chain: Cycle Inventory, Safety Inventory, ABC Inventory & Product AvailabilityAsma ShoaibNo ratings yet

- Fundamentals of Accounting II AssignmentDocument2 pagesFundamentals of Accounting II Assignmentbirukandualem946No ratings yet

- Black White and Teal Minimal Abstract Patterns Finance Report Finance PresentationDocument15 pagesBlack White and Teal Minimal Abstract Patterns Finance Report Finance PresentationamirulNo ratings yet

- Final QARSHI REPORTDocument31 pagesFinal QARSHI REPORTUzma Khan100% (2)

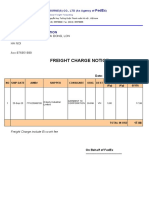

- Freight Charge Notice: To: Garment 10 CorporationDocument4 pagesFreight Charge Notice: To: Garment 10 CorporationThuy HoangNo ratings yet

- Mohamed Nada - Learn Pivot Tables in One Hour EbookDocument37 pagesMohamed Nada - Learn Pivot Tables in One Hour EbookEjlm OtoNo ratings yet

- Progress Test 4 KeyDocument2 pagesProgress Test 4 Keyalesenan100% (1)

- Modern OfficeDocument10 pagesModern OfficesonuNo ratings yet

- A Guide About Bank AccountsDocument6 pagesA Guide About Bank AccountsHelloprojectNo ratings yet

- 73 220 Lecture07Document10 pages73 220 Lecture07api-26315128No ratings yet

- Ccs (Conduct) RulesDocument3 pagesCcs (Conduct) RulesKawaljeetNo ratings yet

- Atestat Pagau Maria XII-E CNPCB CorectatDocument5 pagesAtestat Pagau Maria XII-E CNPCB CorectatMaria ItuNo ratings yet