You might also like

- Plastic Products LahoreDocument32 pagesPlastic Products LahoreAbdul SattarNo ratings yet

- The Co-Operative Societies Rules, 1927Document33 pagesThe Co-Operative Societies Rules, 1927Muzaffar IqbalNo ratings yet

- Gazette Inter Part-II Annual 2014 PDFDocument1,158 pagesGazette Inter Part-II Annual 2014 PDFAbdul SattarNo ratings yet

- Skincare CosmeticsDocument86 pagesSkincare CosmeticsAbdul SattarNo ratings yet

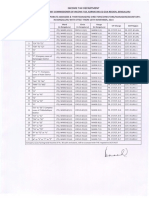

- Financial Powers Distt Governments 8 TH EdDocument293 pagesFinancial Powers Distt Governments 8 TH EdchalakasifNo ratings yet

- Hair GelDocument1 pageHair GelerksevNo ratings yet

- FR and SR Rules PunjabDocument515 pagesFR and SR Rules PunjabGolden SparrowNo ratings yet

- Formulation and Characterization of Sunscreen Creams With Synergistic Efficacy On SPF by Combination of UV FiltersDocument5 pagesFormulation and Characterization of Sunscreen Creams With Synergistic Efficacy On SPF by Combination of UV FiltersAbdul SattarNo ratings yet

- Croda Capital Markets Day: 7 November 2012Document138 pagesCroda Capital Markets Day: 7 November 2012Abdul SattarNo ratings yet

- The Co-Operative Societies Rules, 1927Document33 pagesThe Co-Operative Societies Rules, 1927Muzaffar IqbalNo ratings yet

- Carnuba Wax EmulsionDocument0 pagesCarnuba Wax EmulsionAbdul SattarNo ratings yet

- The Co-Operative Societies Rules, 1927Document33 pagesThe Co-Operative Societies Rules, 1927Muzaffar IqbalNo ratings yet

- The Co-Operative Societies Rules, 1927Document33 pagesThe Co-Operative Societies Rules, 1927Muzaffar IqbalNo ratings yet

- Deputation PolicyDocument4 pagesDeputation Policymamjad381No ratings yet

- Us 4121904Document7 pagesUs 4121904Abdul SattarNo ratings yet

- Standard Bidding Document - Drugs & Medicines For DHQ THQDocument86 pagesStandard Bidding Document - Drugs & Medicines For DHQ THQAbdul SattarNo ratings yet

- Depilatory HerbalDocument10 pagesDepilatory HerbalAbdul SattarNo ratings yet

- 56-Compact Cream FoundationDocument1 page56-Compact Cream FoundationAbdul SattarNo ratings yet

- The Co-Operative Societies Rules, 1927Document33 pagesThe Co-Operative Societies Rules, 1927Muzaffar IqbalNo ratings yet

- DRADocument28 pagesDRAAbdul SattarNo ratings yet

- 56-Compact Cream FoundationDocument1 page56-Compact Cream FoundationAbdul SattarNo ratings yet

- 96-Pressed Mineral PowderDocument1 page96-Pressed Mineral PowderAbdul SattarNo ratings yet

- Shampoo ThicknersDocument8 pagesShampoo ThicknersAbdul SattarNo ratings yet

- DRADocument28 pagesDRAAbdul SattarNo ratings yet

- Skin CareDocument20 pagesSkin CareAbdul Sattar100% (1)

- SMEDA Copyrights Registration ProcedureDocument17 pagesSMEDA Copyrights Registration ProcedureAbdul SattarNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Tax Checklist For NursesDocument1 pageTax Checklist For NursesSasperilla SummerNo ratings yet

- Car Rental Voucher - Booking - Com Car HireDocument4 pagesCar Rental Voucher - Booking - Com Car HireMarcelo CubilloNo ratings yet

- Countrywise Withholding Tax Rates Chart As Per DTAADocument8 pagesCountrywise Withholding Tax Rates Chart As Per DTAAajithaNo ratings yet

- E Bay ISAPIDocument2 pagesE Bay ISAPIShivam AroraNo ratings yet

- I AnnexureDocument4 pagesI AnnexureRiSHI KeSH GawaINo ratings yet

- Project Report GSTDocument57 pagesProject Report GSTVidhi RamchandaniNo ratings yet

- Annexure Viii Neon Cable - 26!04!2021Document12 pagesAnnexure Viii Neon Cable - 26!04!2021group3 cgstauditNo ratings yet

- LLB IV Sem GST Unit I Levy and Collection Tax by DR Nisha SharmaDocument7 pagesLLB IV Sem GST Unit I Levy and Collection Tax by DR Nisha Sharmad. CNo ratings yet

- Tax Cases April 28Document52 pagesTax Cases April 28Treborian TreborNo ratings yet

- 2017 TXN - TXT 2 - PDF - BitcoinDocument4 pages2017 TXN - TXT 2 - PDF - BitcoinDaniel NaeNo ratings yet

- Form16 Instructions 2015-16 FinalDocument8 pagesForm16 Instructions 2015-16 FinalVenugopal Athiur RamachandranNo ratings yet

- 9YWwhh55h5384810244629010109102 PDFDocument2 pages9YWwhh55h5384810244629010109102 PDFDave Yerznkyan100% (1)

- Form 16 by Tcs PDFDocument5 pagesForm 16 by Tcs PDFAnonymous utPqL6jA3i25% (4)

- Jurisdiction Details PDFDocument57 pagesJurisdiction Details PDFjigneshNo ratings yet

- Chapter 3Document4 pagesChapter 3Frances Garrovillas100% (2)

- South Dakota Property Tax 101Document3 pagesSouth Dakota Property Tax 101inforumdocsNo ratings yet

- Gen Principles of TaxationDocument437 pagesGen Principles of TaxationJurilBrokaPatiñoNo ratings yet

- July Pay2Document1 pageJuly Pay2CresteynTeyngNo ratings yet

- OpTransactionHistory23 07 2022Document12 pagesOpTransactionHistory23 07 2022Rakesh KumarNo ratings yet

- Sandpiper Rental AgreementDocument12 pagesSandpiper Rental AgreementkyfullertonNo ratings yet

- BasesxaqDocument92 pagesBasesxaqanibalNo ratings yet

- Cash & Cash EquivalentsDocument4 pagesCash & Cash Equivalentsralphalonzo100% (5)

- DeductionsDocument4 pagesDeductionsDianna RabadonNo ratings yet

- 30, Vinayaka Layout, Shanthipura: House Rent ReceiptDocument5 pages30, Vinayaka Layout, Shanthipura: House Rent ReceiptmorasriNo ratings yet

- BIR Ruling (DA-335) 815-09Document5 pagesBIR Ruling (DA-335) 815-09Ren Mar CruzNo ratings yet

- Ajioluxe Plat TC New23Document3 pagesAjioluxe Plat TC New23templarNo ratings yet

- Monese StatementDocument2 pagesMonese StatementNyamweya Webster JuniorNo ratings yet

- Possible VAT Implications of Transfer PricingDocument12 pagesPossible VAT Implications of Transfer PricingPablo De La MotaNo ratings yet

- Sales Invoice - Ra EnterpiseDocument1 pageSales Invoice - Ra EnterpiseRohtas SharmaNo ratings yet

- Online Banking TCsDocument52 pagesOnline Banking TCsmaverick_1901No ratings yet